The Memo About Mortgage Insurance Stocks You Need to See

If you haven't already gotten the memo about mortgage insurance companies, then here it is: Avoid them like the plague.

It shouldn't be a surprise to anyone that private-label mortgage insurers have been, and continue to be, in serious trouble since the onset of the financial crisis. As my Foolish colleague Dan Caplinger noted: "it's hard to think of a business you'd want to be in less."

Walk through just about any single-family development project and you'll see why. While the financial crisis may seem like a distant memory, "for sale" signs remain ubiquitous, with many advertising properties as "short sales" or "bank owned." And if you look closely, it isn't uncommon to see newly issued foreclosure documents affixed to front doors.

A siren song for the uninitiated

Many of you are likely wondering why I bring this up now. Isn't it true these companies have struggled for over five years? Yes, of course. The reason I'm writing about it now, in turn, is because their recent and seemingly impressive stock performance could serve as a siren song to the uninitiated.

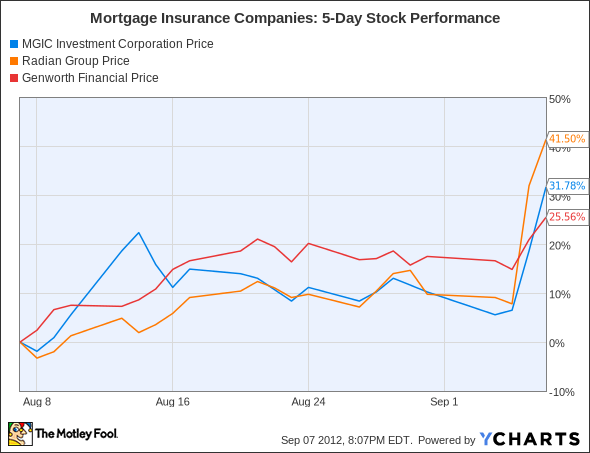

If you didn't know these companies were down between 75% and 95% over the last five years, the recent uptick could be deceivingly enticing. Take a look at the following chart, which plots the five-day stock performance of MGIC Investment (NYS: MTG) , Radian Group (NYS: RDN) , and Genworth Financial (NYS: GNW) , three of the biggest players in this space.

Why the excitement?

On a general level, there's a growing chorus of evidence that the housing market is recovering. As I wrote last week, single-family housing starts are up 22% year over year, the Case-Schiller home-price index has increased for five consecutive months, and the National Association of Home Builders' housing market index recently rose to its highest level since February of 2007.

On a more specific level, there's similar noise about the mortgage insurance industry. At the beginning of June, my colleague Amanda Alix wrote that mortgage insurers were on the rebound. Her rationale? These three companies had reported a collective increase in business in April, writing insurance policies worth $7.1 billion, up from $6.7 billion in March.

The industry was thus locked and loaded. The final trigger arrived last Thursday, when Radian Group published delinquency data further indicative of a rebound. For the month of August, its delinquent loans dropped more than 2%, falling to less than 95,000 loans from 97,000 the month before.

Don't let these gains fool you

Despite this success, and what otherwise may appear to be a bargain given their valuations, I implore you to think twice before adding any mortgage insurance stocks to your portfolio.

Even though it's been years since the financial crisis officially ended, the carnage remains strewn throughout the financial industry. Bank of America's (NYS: BAC) balance sheet provides a case in point, as more than 7.5% of its loans are designated as noncurrent -- a staggeringly high percentage in historical terms, and one of the three disturbing areas that every B of A shareholder should be aware of according to our in-depth report on the lending giant.

Finally, even their most important customer, Fannie Mae, has little faith in the continued viability of many private-label mortgage insurers. Here's how the quasi-governmental agency described the industry in its most recent quarterly report:

"As of August 8, 2012, of our largest mortgage insurers, one -- [PMI] -- has publicly disclosed that it is in receivership and two -- [Triad] and [Republic] -- have publicly disclosed that they are in run-off ... In addition, [Genworth] is currently operating pursuant to a waiver it received from its regulator of the state regulatory capital requirements applicable to its main insurance writing entity. [Radian] has disclosed that, in the absence of additional capital contributions to its main insurance writing entity, its capital might fall below state regulatory capital requirements in the future ... Additionally, [Mortgage Guaranty] has disclosed that it expects that its capital fell below state regulatory capital requirements as of June 30, 2012, and is currently operating pursuant to a waiver it received from the regulator of the state regulatory capital requirements applicable to its main insurance writing entity."

Not exactly what you'd call a sterling endorsement.

You've now gotten the memo

Look, I'm not different than any other investor reading this. Like you, I'm constantly looking for unappreciated and undervalued stocks primed to provide monster returns. Yet, while there's no doubt mortgage insurance company stocks are unappreciated, there's also effectively no evidence that they're undervalued. As a result, you'd be smart to avoid them altogether.

In their place, I would consider any of the companies identified in our free report about three Dow stocks every investor needs. All three of the underlying companies, including one that's a favorite of Warren Buffett, are solid investments and pay generous dividends. To learn the identity of these stocks before the rest of the market catches on, simply click here to download the free report instantly.

The article The Memo About Mortgage Insurance Stocks You Need to See originally appeared on Fool.com.

Fool contributor John Maxfield and The Motley Fool own shares of Bank of America. The Motley Fool has adisclosure policy. We Fools may not all hold the same opinions, but we all believe thatconsidering a diverse range of insightsmakes us better investors. Try any of our Foolish newsletter servicesfree for 30 days.

Copyright © 1995 - 2012 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.