Why CEMEX Shares Could Head Even Higher

Shares of CEMEX (NYS: CX) hit a 52-week high on Wednesday. Let's take a look at how it got there and see if clear skies are still in the forecast.

How it got here

After years of back-and-forth worrying as to whether CEMEX would be able to claw its way out from under billions in debt, it appears that the pieces of the puzzle are finally coming together for one of the world's largest cement producers.

CEMEX announced yesterday that after plenty of negotiating, many of its creditors are on board to help push $7.2 billion worth of debt back to later dates. In addition, the company announced that it would be raising cash by selling a stake in its Latin American operations on the Colombian stock market. All told, CEMEX's debt refinancing and cash raising efforts, compounded with renewed stability in the cement market, should easily allow the company to meet its $1 billion debt obligation due in March 2013.

Beyond refinancing its debt, CEMEX also noted other cost-cutting and growth drivers that caused its core operating profits to hit their highest levels in three years. On the cost-cutting front, CEMEX signed a deal to outsource 2,000 jobs to IBM (NYS: IBM) . The deal is expected to save $1 billion over the next 10 years. CEMEX is also seeing stabilization in the U.S. housing industry, as evidenced by the strength from America's largest homebuilder, D.R. Horton (NYS: DHI) , which recorded net sales order growth of 25% in its latest quarter.

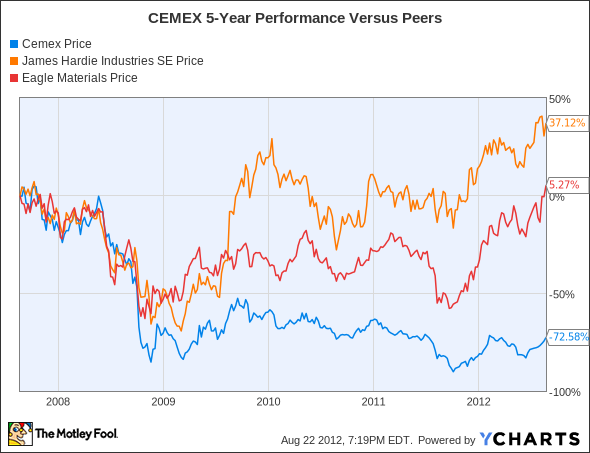

How it stacks up

Let's see how CEMEX shares compares to its peers.

As you can see, CEMEX's peers, James Hardie Industries (NYS: JHX) and Eagle Materials (NYS: EXP) , have significantly outperformed the debt-riddled cement maker over the past five years.

Company | Price/Book | Price/Cash Flow | Forward P/E | Debt/Equity |

|---|---|---|---|---|

CEMEX | 0.7 | 22.5 | NM | 143.7% |

James Hardie Industries | 139.1 | 9.1 | 47.7 | 0% |

Eagle Materials | 3.9 | 23.4 | 27.5 | 52.5% |

Source: Morningstar. NM = not meaningful; earnings are expected to be negative over the next 12 months.

For those of you who consider yourselves value investors, look away before you turn to stone! Cement producers aren't exactly sitting in the sweet spot in terms of growth, yet all three are seeing their share prices rise dramatically.

It's not hard to see why James Hardie is the best performer, given that it's the only one of the three here that has no debt. Still, James Hardie's pricey valuation is a concern, especially after it forecast lower-than-expected full-year revenue on the heels of a deteriorating Australian housing market and U.S. uncertainty.

Eagle Materials, at 23 times cash flow and nearly 28 times forward earnings, is the "value" company of this group, but it's also had a pleasant upside surprise. Cement revenue rose by 26% in its latest quarter as the company continued to wield a stranglehold on its expenses.

CEMEX has been crushed by unfavorable currency translations and crippling debt, but its recent refinancing efforts could quickly change that.

What's next

Now for the $64,000 question: What's next for CEMEX? The answer depends on CEMEX's ability to continue to reduce its debt burden, the overall health of the cement industry in the U.S. and Latin America, and the success of its peers in garnering market share.

Our very own CAPS community gives the company a four-star rating (out of five), with 96% of nearly 4,000 members expecting it to outperform. Although I've been decidedly negative on the U.S. housing sector, I'm among those optimists to have made a CAPScall of outperform on CEMEX. That call is up a whopping 69 points as of this writing.

The CEMEX story isn't without its challenges. Although CEMEX appears to have solved its near-term liquidity issues, it'll still need to cope with an uncertain U.S. market and crazy currency vacillations. However, my initial reasoning for getting into CEMEX is its premier position in the cement market in Latin and Southern America, where construction growth hasn't tapered off much. By focusing on these regions, CEMEX should be able to return to profitability and really begin making some serious dents in its large debt pile.

Even if you feel CEMEX isn't the right stock to retire with, our analysts at Stock Advisor are bound to have a company or two that'll tickle your fancy in our latest free report. Find out the identity of three companies that could lead you into a comfortable retirement by clicking here.

If you're still craving even more info on CEMEX, I would recommend adding the stock to your free and personalized watchlist so you can keep up on all of the latest news with the company.

The article Why CEMEX Shares Could Head Even Higher originally appeared on Fool.com.

Fool contributor Sean Williams has no material interest in any companies mentioned in this article. You can follow him on CAPS under the screen name TMFUltraLong, track every pick he makes under the screen name TrackUltraLong, and check him out on Twitter, where he goes by the handle @TMFUltraLong.The Motley Fool owns shares of IBM. Motley Fool newsletter services have recommended creating a synthetic long position in IBM. Try any of our Foolish newsletter services free for 30 days. We Fools don't all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.

Copyright © 1995 - 2012 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.