First Solar's Latest Pop Is Just the Beginning

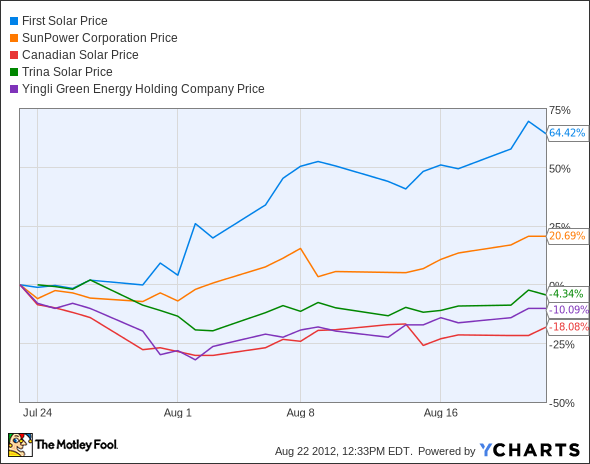

First Solar (NAS: FSLR) seems to have gone from market outcast to the hottest stock in energy in recent weeks. After the company's earnings report earlier this month, the market seems to have found some value in the company's strategy shift and its continued profitability.

The rally hasn't made its way to all solar stocks, though. SunPower (NAS: SPWR) is up nicely over the past month, but Chinese leaders Trina Solar (NYS: TSL) , Canadian Solar (NAS: CSIQ) , and Yingli Green Energy (NYS: YGE) are all down over the past month.

I believe this is because investors are starting to understand that the long-term success of companies in solar is more dependent on quality products, vertical integration, and strong balance sheets versus competing primarily on cost. So can First Solar's run continue?

Modules won't drive growth

If First Solar is going to stay in the module business it won't be as a dominant player. Despite increasing conversion efficiency to 12.6% in the last quarter, First Solar is still behind Chinese firms like Canadian Solar and is well below SunPower's industry-leading panels, which exceed 20% efficiency.

As the cost of these more efficient panels fall, the cost difference becomes less meaningful. For example, if an entire installation costs $4 per watt with First Solar panels and installers have the option to install panels that will generate 50% more electricity for $0.15 more, there's no question they would do it. This is why SunPower dominates the residential market and First Solar has a larger hold in the utility-scale market.

Systems are the future

Where First Solar has a clear advantage over competitors is in its systems business. The company has 2.9 GW of systems in its pipeline and a number of well-known partners buying its projects. This ability to build bankable projects is where First Solar's biggest opportunity lies.

It will be able to use its strong balance sheet as a selling point for systems as well. Even when the system is sold, there are warranty and servicing obligations, commitments buyers want to know will be lived up to. First Solar has the history and the balance sheet to meet these obligations.

Will the hot streak end?

We've seen solar stocks rise and fall quickly before, so there's no guarantee the streak won't end tomorrow. But the stock is only trading at 5.6 times the low end of management's 2012 earnings guidance and the company has $744 million of cash on the balance sheet as a cushion.

I think that sets the company up for long-term success for investors willing to buy now and not worry about volatility tomorrow. For more reasons to buy the stock as well as warning signs to watch for, check out our detailed report on the stock. It comes with a year of updates as the market conditions change, and can only be found here.

The article First Solar's Latest Pop Is Just the Beginning originally appeared on Fool.com.

Fool contributorTravis Hoiumowns shares of SunPower in both personal and managed accounts. You can follow Travis on Twitter at@FlushDrawFool, check out hispersonal stock holdingsor follow his CAPS picks atTMFFlushDraw.The Motley Fool has adisclosure policy. We Fools may not all hold the same opinions, but we all believe thatconsidering a diverse range of insightsmakes us better investors. Try any of our Foolish newsletter servicesfree for 30 days.

Copyright © 1995 - 2012 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.