Can Anything Stop This Discount Retailer?

Shares of Ross Stores (NAS: ROST) hit a 52-week high yesterday. Let's take a look at how it got there and see if clear skies are still in the forecast.

How it got here

Since I last looked at Ross Stores roughly four months ago, it appears that the only thing that's changed is the stock has rocketed even higher.

Ross, which offers brand-name and designer merchandise at a discount, continues to appeal to a bargain-hungry consumer eager for designer apparel. In its second-quarter results released last week, Ross highlighted a 27% increase in EPS from a 12% rise in total sales. A good mix of product compounded with stringent cost-cutting and inventory control has created a margin-packing powerhouse.

As always, there are plenty of factors waiting to derail Ross' efforts to head higher. For one, the competition among discount retailers is fierce. Kohl's (NYS: KSS) , Wal-Mart (NYS: WMT) , and TJX (NYS: TJX) are always waiting in the wings to take consumers from Ross if it falters. Secondly, Ross' pricing needs to be just right so that it doesn't kill its margins or send consumers running for better deals. J.C. Penney (NYS: JCP) shareholders can tell you all about the perils of changing a pricing strategy -- Penney's has seen same-store sales fall close to 20% in two straight quarters. Finally, Ross is battling weakening U.S. GDP growth, which threatens to strap disposable spending.

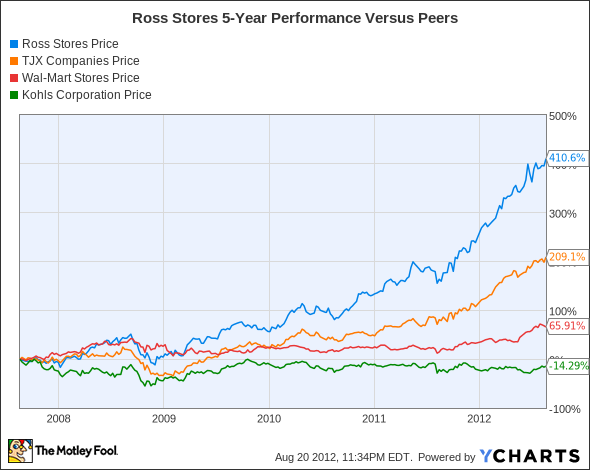

How it stacks up

Let's see how Ross Stores stacks up next to its peers.

ROST data by YCharts.

Ross and TJX have absolutely written the book on "how to sell" since the recession. Kohl's may want to pick up a copy!

Company | Price/Book | Price/Cash Flow | Forward P/E | Revenue Growth (3-year average) |

|---|---|---|---|---|

Ross Stores | 9.8 | 14.8 | 18.1 | 9.9% |

TJX | 10.2 | 14.2 | 16.8 | 6.9% |

Wal-Mart | 3.5 | 9.0 | 13.4 | 3.4% |

Kohl's | 2.0 | 6.2 | 8.7 | 4.7% |

Source: Morningstar.

Much as I discussed in April, there's a clear bifurcation between discount retailers that offer designer brands and are successful, versus the valuation of those that can't execute their plan. Both Ross and TJX are valued at premiums in terms of book and forward P/E largely because they've been able to keep traffic up in their stores and they understand how to control inventory and maintain margins.

Kohl's and Wal-Mart are two completely different stories. Wal-Mart has successfully turned its apparel division around after a three-year slump, but it relies predominantly on its grocery business for much of its revenue. It's not quite comparable on a margin basis, but Wal-Mart will never command the same premium that Ross or TJX are receiving right now. Kohl's, on the other hand, has been downright disappointing. Its total sales slumped 1% as same-store sales dropped 2.7% for the second quarter. After many disappointing quarters, it's no secret why the company appears cheap on paper.

What's next

Now for the $64,000 question: What's next for Ross Stores? The answer is going to depend largely on the health of the U.S. economy and consumer spending, as well as on Ross Stores' ability to control its inventory levels.

Our very own CAPS community gives the company a four-star rating (out of five), with a whopping 91.6% of members expecting it to outperform. Just as I was leaning toward making a CAPScall of outperform on Ross in April but wanted a pullback, I'm still in the exact same camp (only the stock has gone even higher).

Ross' execution has been practically unparalleled since the recession. It has done a perfect job of pricing its designer clothing within the budgets of middle-class America and has done an even better job controlling its inventory. Even if GDP contracts further and consumer spending dips, there's little reason to believe that Ross won't continue to outperform its peers. I would really like to see Ross boost its yield higher than the current 0.8%, but in retrospect, its quarterly payout has more than tripled to $0.14 from $0.04 in just five years. For now I'm going to wait on the sidelines until I get that aforementioned pullback.

The great thing about Ross Stores is it's an easy-to-understand business. That's one premise behind Peter Lynch's investment style and one of the main reasons our team of analysts at Motley Fool Stock Advisor have picked out three winners for us middle-class investors that aren't already sitting on Warren Buffett-type cash. Find out the identity of these three stocks for free by clicking here to get your copy of this latest special report.

Craving more input on Ross Stores? Start by adding it to your free and personalized Watchlist. It's a free service from The Motley Fool to keep you up to date on the stocks you care about most.

The article Can Anything Stop This Discount Retailer? originally appeared on Fool.com.

Fool contributor Sean Williams has no material interest in any companies mentioned in this article. You can follow him on CAPS under the screen name TMFUltraLong, track every pick he makes under the screen name TrackUltraLong, and check him out on Twitter, where he goes by the handle @TMFUltraLong.Try any of our Foolish newsletter services free for 30 days. We Fools don't all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.

Copyright © 1995 - 2012 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.