3 Reasons to Buy VIVUS

Shares of biotech company VIVUS (NAS: VVUS) have been on a roller-coaster ride lately as a result of contrasting headlines in the news. The stock plummeted last month when patent concerns surfaced surrounding the company's new prescription weight-loss drug Qsymia. However, it was Qsymia's approval by the Food and Drug Administration in mid-July that had lifted the stock to a 52-week high. With so much movement in the stock it can be difficult knowing when to buy or sell shares. That's why I've outlined three reasons I think VIVUS is a buy today.

1: Approval of anti-obesity drug

VIVUS' newly approved treatment for obesity is important for a couple of reasons. First, it operates in an underserved market. According to Bloomberg, 42% of Americans will be obese by 2030. That's a frightening figure, but not for companies like VIVUS, as the climbing rate of obesity means strong demand and big bucks. That's not to say that VIVUS doesn't face competitors.

Quite the opposite, in fact, since VIVUS' drug will directly compete with Arena Pharmaceuticals' (NAS: ARNA) weight-loss pill Belviq. Arena's medication was approved ahead of VIVUS' Qsymia, although it now looks like Qsymia will be the first of the two treatments to hit the market. This is an impressive achievement for both companies considering it's the first time medications such as these have been cleared for sale in the United States in more than a decade.

Qsymia is expected to be commercially available before the end of fiscal 2012. Rodham & Renshaw say sales of the drug could reach $290 million by next year. Yet, even if VIVUS falls short of this specific mark, the company will certainly enjoy an earnings boon in 2013.

2: Medical advantages over the competition

Clinical trials of both Qsymia and Belviq showed VIVUS' Qsymia as being more effective in the treatment of obesity. For example, patients who took Qsymia lost on average about 10% of their body weight, while those on Belviq experienced only a 4% drop in body mass.

Additionally, patients being prescribed Qsymia are encouraged to take the medication for a minimum of six months. For VIVUS, this means three extra months of drug sales per patient compared to the recommended duration for the rival treatment from Arena Pharmaceuticals.

Potential competition from Orexigen Therapeutics (NAS: OREX) has also been wiped out -- at least until next year. The FDA forced the obesity drug maker to extend pre-approval trials on its Contrave product due to cardiovascular risks. Until Orexigen can prove that its drug is safe it looks like the only two real contenders in the space are VIVUS and Arena Pharmaceuticals.

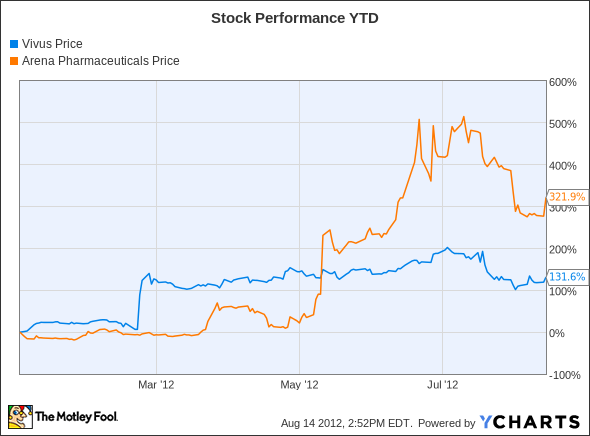

Now that we've done a side-by-side comparison of VIVUS and Arena's competing obesity remedies, let's see how the two frontrunners measure up in terms of stock performance.

As you can see, Arena takes the lead in this regard with shares up more than 287% year-to-date. Meanwhile, VIVUS has gained upward of 123% so far this year. That's not great for current VIVUS shareholders considering Orexigen's stock is up nearly 158% year-to-date, despite not yet receiving FDA approval for its key weight-loss drug, Contrave.

Fortunately, I think this creates a buying opportunity for investors who don't mind a bit of volatility. Shares of VIVUS are currently trading at $22 apiece, or 26% below the stock's 52-week high of $31.

3: Long-term growth

The market potential for obesity drugs is tremendous, and VIVUS has a front-row seat. Not only does Qsymia create opportunities for VIVUS in the U.S. but also overseas as well. The company is also poised for commercial success with its erectile dysfunction drug, Stendra. Unlike Arena Pharmaceuticals, this means VIVUS isn't completely reliant on the success of its anti-obesity drug for sustained growth.

Stendra, which received FDA approval in April, could give Pfizer's (NYS: PFE) Viagra a run for its money. According to Bloomberg, VIVUS' remedy works in less than half the time that it takes for Viagra to work. Last year, Pfizer pulled in $2 billion in sales of Viagra, proving that strong demand exists for the treatment of erectile dysfunction. Going forward, I expect VIVUS to gain traction in this market segment.

New medical solutions from companies such as VIVUS and Arena Pharmaceuticals often lead to meaningful gains in stockholder value. As these two biotech firms ready their drugs for the market, now is a good time to get on board.

For many investors, the biotech industry can be complicated and hard to navigate. Luckily, the Motley Fool just released a new premium report on Arena Pharmaceuticals and the industry at large. In the report you will get in-depth analysis on this biotech, as well as key opportunities and risks surrounding the stock. Click here to check it out now and you will also get a full year of timely updates on shares of Arena.

The article 3 Reasons to Buy VIVUS originally appeared on Fool.com.

Fool contributor Tamara Rutter owns shares of VIVUS and Arena Pharmaceuticals. Follow her onTwitter, where she uses the handle@TamaraRutter, for more Foolish insights and investing advice. The Motley Fool has a disclosure policy. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. Try any of our Foolish newsletter services free for 30 days.

Copyright © 1995 - 2012 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.