Is It Time to Buy or Fly on Express Scripts?

Shares of pharmacy-benefit management (PBM) company Express Scripts (NAS: ESRX) hit a 52-week high on Wednesday. Let's take a look at how it got there and see if clear skies are still in the forecast.

How it got here

Who would have ever thought that a lengthy delay in the regulatory approval of Express Scripts' merger with Medco Health Solutions would have been a positive for the company. In Express Scripts' second-quarter results released yesterday, the company noted that the eight-month antitrust review process allowed it to get all of its ducks in a row, such that when the deal was finally approved, it was able to quickly integrate the two platforms and realize cost synergies to a greater degree than it had predicted.

For the second quarter, Express Scripts easily surpassed Wall Street's expectations by reporting revenue of $27.7 billion, which was more than double the $11.4 billion reported in the year-ago quarter, with $0.88 in EPS. Many investors were concerned that a recent spat between it and Walgreen (NYS: WAG) , whereby Walgreen stopped routing prescription orders through Express Scripts, would hurt both parties, but it appears Walgreen was the only one to suffer, losing pharmacy customers to CVS Caremark (NYS: CVS) and Rite-Aid (NYS: RAD) .

We should keep in mind, though, that Express Scripts won't have a cakewalk in the PBM field. It continues to face tough competition from CVS Caremark and Catamaran (NAS: CTRX) , in addition to dealing with probably another year or possibly more of Medco platform integration. Merging two large companies is never easy, and it rarely goes off as smoothly as Express Scripts is making it sound.

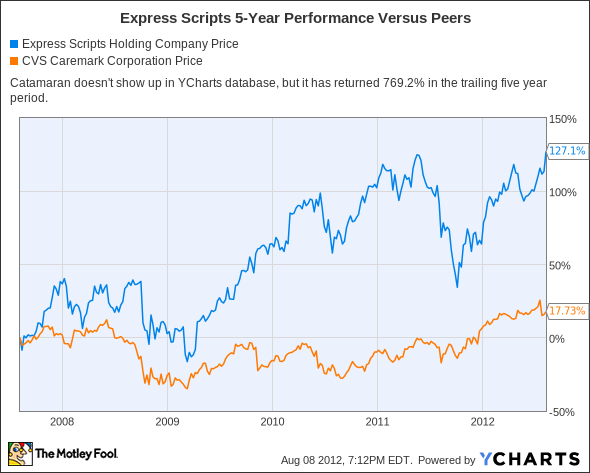

How it stacks up

Let's see how Express Scripts stacks up next to its peers.

The PBM sector has been a major source of growth over the past five years, with Catamaran returning nearly 770% and Express Scripts up a not-too-shabby 127%.

Company | Price / Book | Price / Cash Flow | Forward P/E | Debt / Equity |

|---|---|---|---|---|

Express Scripts | 2.3 | 12.9 | 14.1 | 415.7% |

CVS Caremark | 1.5 | 8.7 | 11.8 | 24.2% |

Catamaran | 7.4 | 32.0 | 29.4 | 7.9% |

Source: Morningstar, Yahoo! Finance.

We can see some clear differentiation between these companies based on their financial metrics. Express Scripts has made no secret that it's aggressively using its capital, including debt, to facilitate mergers. Combining with Medco leaves it considerably more in debt than its peers. That's one reason those aforementioned cost synergies are extremely important.

CVS Caremark is absolutely the best value on paper here with a reasonable amount of debt and the lowest book, cash flow, and forward P/E. Unfortunately, CVS Caremark also boasts a tepid growth rate relative to the other two companies here. That's not bad, however, as it also supplies the only dividend of these three stocks.

Catamaran is without a doubt the best-capitalized, but most expensive, stock of this group. At more than 30 times cash flow and roughly 30 times forward earnings, there isn't much room for error at current levels.

What's next

Now for the $64,000 question: What's next for Express Scripts? The answer to that question depends on how quickly it can complete its integration with Medco and recognize $1 billion or more in cost synergies, and if it can repay a good portion of its $11.5 billion in debt.

Our very own CAPS community gives the company a four-star rating (out of five), with a whopping 94.3% of members expecting it to outperform. Although I've yet to make a CAPScall in either direction, I'm definitely leaning more toward outperform.

Express Scripts has a lot of potential upside catalysts. Having mended with Walgreen, the company will again begin filling orders for the pharmacy giant in September. In addition, the passing of the Affordable Care Act should bring a new pool of insurable persons heading to pharmacies in 2014 and after, which has the potential to greatly increase Express Scripts' customer base. Finally, its Medco cost savings will be a boost to its bottom line earnings ... eventually. In the meantime, I'm not convinced the company won't have integration hiccups along the way. For now I'm going to sit on the sidelines and add Express Scripts to my Watchlist.

Peter Lynch has always inspired investors to buy what they know and businesses they could easily understand. Our analysts at Motley Fool Stock Advisor couldn't agree more and recently released a report highlighting three stocks that middle-class investors like you and I, who don't have Warren Buffett-type cash in our pockets can use to get rich. See what companies they've highlighted, for free, by clicking here.

The article Is It Time to Buy or Fly on Express Scripts? originally appeared on Fool.com.

Fool contributor Sean Williams has no material interest in any companies mentioned in this article. You can follow him on CAPS under the screen name TMFUltraLong, track every pick he makes under the screen name TrackUltraLong, and check him out on Twitter, where he goes by the handle @TMFUltraLong.The Motley Fool owns shares of Express Scripts and Catamaran. Motley Fool newsletter services have recommended buying shares of Express Scripts and Catamaran. Try any of our Foolish newsletter services free for 30 days. We Fools don't all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.

Copyright © 1995 - 2012 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.