What the Heck Is Going on With Heckmann?

Shares of Heckmann (NYS: HEK) hit a 52-week low yesterday. Let's take a look at how it got here to find out whether there are still cloudy skies ahead.

How it got here

Heckmann's woes stem from its latest earnings report, which had an unexpected adjusted loss, and from the company's lack of forward guidance. This uncertainty was interpreted with extreme negativity, as the market sent shares down by over 20% yesterday.

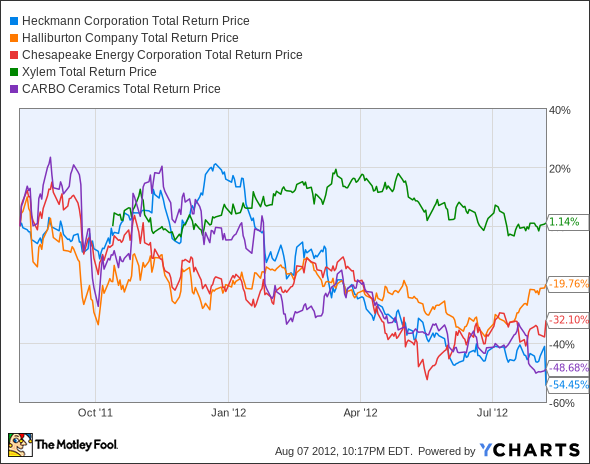

Stock negativity is hardly limited to Heckmann, especially when one considers other companies focused on nat-gas extraction. Large and small drilling services companies, from heavyweight Halliburton (NYS: HAL) to comparatively tiny CARBO Ceramics (NYS: CRR) , have all slid this year as the nat-gas industry flounders. Many services companies have closely tracked the performance of the energy producers they assist, as you can see from the relatively close clustering of Heckmann, CARBO, and Chesapeake Energy (NYS: CHK) :

HEK Total Return Price data by YCharts

Xylem (NYS: XYL) , a larger water-services company, has avoided Heckmann's fate so far thanks to greater diversity, which includes several manufacturing subsidiaries offering products for uses well beyond Heckmann's water provision and treatment focus.

What you need to know

Heckmann's done one thing much better than its peers. It's taken off running over the past three years, growing sales by a far greater rate than any other roughly comparable company:

Company | P/E Ratio | Gross Margin (TTM) | 3-Year Annualized Revenue Growth* | Debt to Equity |

|---|---|---|---|---|

Heckmann | NM | 16.6%^ | 89.5% | 0.6 |

Halliburton | 10.2 | 19.0% | 23.6% | 0.3 |

CARBO Ceramics | 11.5 | 36.2%^ | 24.9% | N/A |

Chesapeake Energy | 19.8 | 46.2% | 17.3% | 0.7 |

Xylem | 16.1 | 39.6%^ | 10.4% | 0.6 |

Source: Morningstar. NM = not meaningful due to negative results.

* Revenue growth calculated from 2009 annual results and TTM results.

^ Most recent quarter.

On the other hand, Heckmann's the only unprofitable company of the bunch, and its gross margins are worse than the others. Halliburton has similar gross margins, but is far more established, and has an easier-to-calculate upside. CARBO, which makes some nitty-gritty stuff that drillers mix with Heckmann's water for better fracking fluid, has done even better, and has no debt to speak of.

Chesapeake is perhaps the best company to use as a reference for Heckmann's performance, as it's one of Heckmann's largest customers. Its transition away from dirt cheap natural gas is still in progress, which threatens Heckmann's growth in the upcoming year.

What's next?

What lies ahead for Heckmann? Wall Street doesn't see a lot of upside. Two analyst firms downgraded the company after its post-earnings crash. There are undoubtedly headwinds to push past, from the obvious nat-gas drilling drawdown to the less-clear impact of a damaging drought on Heckmann's resources and its expected demand.

The Motley Fool's CAPS community hasn't been turned off yet, giving Heckmann a four-star rating, with a nearly unanimous 97% of our CAPS players expecting the company to rebound and beat the indexes going forward. You can add me to that optimistic crowd -- I've placed an outperform CAPSCall on Heckmann in the hope that yesterday's huge drop represents a bottom to bounce off of.

Interested in tracking this stock as it continues on its path? Add Heckmann to your Watchlist now, for all the news we Fools can find, delivered to your inbox as it happens. If you're looking for other stocks to take advantage of the world's growing need for energy, the Fool's got a free report for you. We've selected three stocks for $100 oil, and you can find out more about these long-term outperformers at no cost. Just click here to get the information you need.

The article What the Heck Is Going on With Heckmann? originally appeared on Fool.com.

Fool contributor Alex Planes holds no financial position in any company mentioned here. Add him on Google+ or follow him on Twitter @TMFBiggles for more news and insights.The Motley Fool owns shares of CARBO Ceramics, Chesapeake Energy, and Heckmann. Motley Fool newsletter services have recommended buying shares of Halliburton. The Motley Fool has a disclosure policy. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. Try any of our Foolish newsletter services free for 30 days.

Copyright © 1995 - 2012 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.