The Incredible Bargain of Eldorado Gold

Some folks just have a knack for walking the path less traveled -- something this gold miner has been doing all along.

Eldorado Gold (NYS: EGO) has set itself apart from the competition in multiple ways. For starters, the company has a tendency to focus its operations in regions where few of its U.S.-traded competitors have a foothold. That trait was evident first in the company's highly successful foray into China, and more recently in its bold move into Greece with the $2.4 billion acquisition of European Goldfields earlier this year.

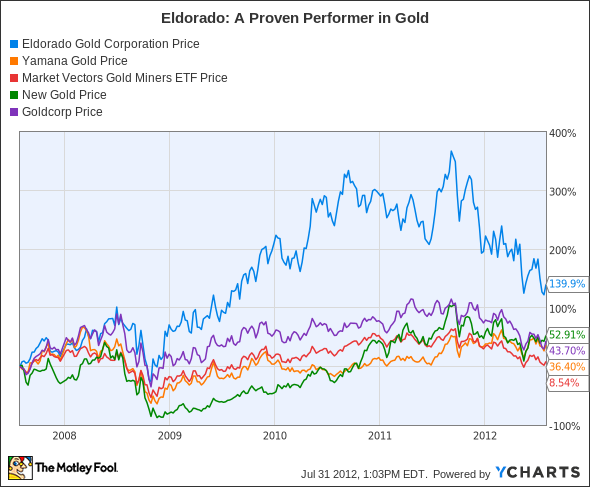

Second, and of particular interest to shareholders, the company has tended to deliver returns that the majority of its competitors have simply failed to provide through this famously challenging period for the gold mining industry at large. As the following chart will show, Eldorado Gold's 140% advance over the trailing-five-year period has this miner walking its own road as a clear outperformer among the mid-tier miners of gold. Rivals Yamana Gold (NYS: AUY) and New Gold (NYS: NGD) have managed to outperform the dismal 8.5% advance of the Market Vectors Gold Miners ETF (NYS: GDX) .

Recalling the company's many successes, and even its own share of setbacks along the way toward one of the industry's most aggressive production growth forecasts, I find myself flabbergasted to see these shares trading as low as they have been lately. Sure, the 20% reduction in anticipated 2012 production -- from an initial target of 808,000 ounces to the revised 660,000 ounces revealed this week -- presents adequate cause for a haircut. But investors need to understand that none of the production shortfalls recorded in the miner's second-quarter results represented game-changing issues of any kind. Eldorado has amassed a sizable stockpile of gold concentrate from the Efemcukuru mine in Turkey (containing 42,000 ounces of gold) that awaits final processing at the Kisladag mill, and the Jinfeng mine in China suffered a major production decline (45% year-over-year) as the operation strips waste from the open pit. These are strictly near-term setbacks, and so Eldorado's long-term growth outlook remains intact.

Still a golden ticket even with adjusted expectations

However, acute increases in mine construction costs and operating costs have forced even major miner Barrick Gold (NYS: ABX) to dramatically revise project economics and reassess its growth trajectory. Working a sizable margin of safety into the industry's growth projections is therefore a wholly sensible adaptation for investors. So when Eldorado speaks of achieving 160% production growth over the next five years (targeting 1.7 million ounces by 2016), I am inclined to adjust my own expectations to a more conservative range of 1.2 million to 1.4 million ounces by 2016. After all, I'd much rather be surprised to the upside than vice versa! Since that adjusted expectation still represents a prompt doubling of output from the company's revised 2012 target, I see plentiful opportunity for meaningful earnings growth to drive further outperformance for the stock within my adjusted scenario.

Speaking of adjusted expectations, let's have a look at how the market valuation of Eldorado's growing reserve base fits into our discussion of the bargain I perceive the current share price. In February 2011, I compared market valuations of proven and probable gold reserves among a group of popular miners, and found Eldorado's enterprise value at the top of the heap (at 42%) relative to the value of its underground reserves. Since that time, Eldorado's corresponding valuation has plummeted to just 18% of the market value ($44.39 billion at $1,620 gold) of its newly expanded reserve base (27.4 million ounces). Stated another way, Eldorado's enterprise value is equivalent to just $287 for each of the miner's reserve ounces. That's 38% less than Goldcorp's corresponding reserve valuation of $452 per ounce. Although I consider Goldcorp the best of the majors, I find no justification whatsoever for a reserve-valuation disconnect of such proportion.

Of course, reserve ounces only retrieve their peak shareholder value when they come out of the ground, so any thorough attempt to value miners must also hone in on projected earnings and cash flow. By applying consensus metal-price assumptions to its own production targets, Eldorado envisions $1.8 billion in operating profit by 2015. After applying my own adjustments to yield a more conservative production outlook, I still find the current share price representing an unreasonably low multiple to the anticipated profitability looming on Eldorado's horizon.

Even if Eldorado were to produce an operating profit of just $1.2 billion in 2015, the current market capitalization stands at just 6.5 times that figure. And for a crude price-to-2015-earnings snapshot, let's apply the recent second-quarter relationship between operating profit and net profit (again using my adjusted conservative production estimates), and I am comfortable anticipating 2015 profit of $675 million. At just 11.4 times that figure, I consider shares of Eldorado Gold extremely desirable at this juncture. I will continue to maintain my bullish CAPScall on the stock, which has been in place without interruption since 2007. And I will continue to scour this gold market for outlandish bargains like this one, and invite readers to bookmark my article list or follow me on Twitter.

Add Eldorado Gold to My Watchlist.

Add Barrick Gold to My Watchlist.

Add Yamana Gold to My Watchlist.

Add New Gold to My Watchlist.

The article The Incredible Bargain of Eldorado Gold originally appeared on Fool.com.

Fool contributor Christopher Barker can be found blogging actively and acting Foolishly within the CAPS community under the username TMFSinchiruna. He tweets. He owns shares of Eldorado Gold and Goldcorp. Motley Fool newsletter services have recommended buying shares of Market Vectors Gold Miners ETF. The Motley Fool has a disclosure policy. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. Try any of our Foolish newsletter services free for 30 days.

Copyright © 1995 - 2012 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.