3 Reasons to Sell Spectrum Pharmaceuticals

This is the sequel to my recent article outlining three reasons Spectrum Pharmaceuticals (NAS: SPPI) looks like a good investment. If you'd like to hear the good news first, follow this link.

But there's another side of the story investors should hear. Understanding the risks is just as important to an investment thesis as knowing what's so great about a company.

Shortages rarely last forever

The biggest risk for Spectrum is the same one that's been present for nearly two years now. The company has seen a sharp increase in sales of Fusilev while generic-drug makers -- Teva Pharmaceuticals (NYS: TEVA) , APP Pharmaceuticals, and Bedford Laboratories -- have struggled to keep a related generic product available for doctors.

The longer the shortage goes on, the more used to using Fusilev doctors get, and the easier it will be for Spectrum to hold onto the market share it's gained after the generic becomes available again.

That makes sense in theory, but it's difficult to know exactly what doctors will do until the shortage subsides. And even if doctors want to prescribe the branded drug, they might come under pressure from hospital formularies and insurance companies to prescribe the generic if it's readily available.

Still a drug developer

Spectrum doesn't discover drugs; it in-licenses all the drugs it sells. Fusilev came from Targent, and the company's non-Hodgkin's lymphoma drug, Zevalin, was originally developed by Biogen Idec (NAS: BIIB) and sold to Cell Therapeutics (NAS: CTIC) before Spectrum eventually gained full control of the drug.

But not all of the cast-offs Spectrum licenses are for drugs ready to sell. The company also licenses drug candidates that still have to pass clinical trials before they'll start producing revenue. While Spectrum eliminates some risk by licensing drugs after they've been through at least some clinical trials, the risk profile for their pipeline isn't that much different from the average biotech's, because late-stage molecules tend to cost more to develop.

The company has two late-stage assets: belinostat for T-cell lymhopmas and other solid tumors and apaziquone for bladder cancer. There are also six drugs in earlier stages of development.

Data from a pivotal clinical trial for belinostat is due out in the fourth quarter. Spectrum is more insulated than a drug developer like MannKind (NAS: MNKD) , which will crash and burn if its lead product doesn't pass upcoming clinical trials, but Spectrum is nowhere near the level of a big pharma that can just shake off a phase 3 trial failure.

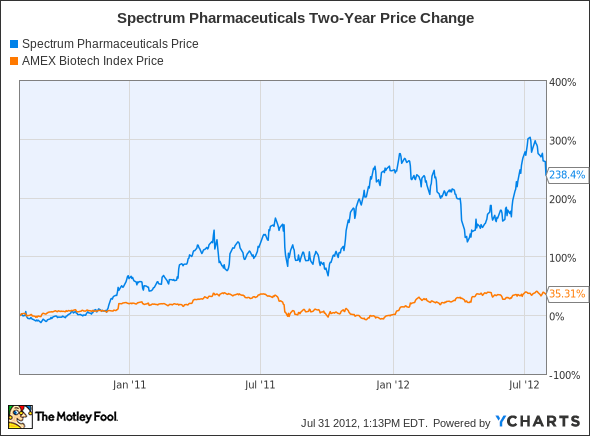

Hard to value

Spectrum has more than doubled over the past two years, handily beating a biotech index.

But it's not the overall run-up that worries me. The company became profitable, and the P/E sits at only 11, so it's not as if investors are pricing in monster growth.

The bigger problem investors should notice from the chart is the huge up and down drafts on the chart. As far as I know, there weren't any major changes that caused the huge run-ups or the decreases. I think investors are rightfully a little anxious about Fusilev's sales, and that causes jitters every time the stock runs up.

Foolish take

If you can confidently say that Fusilev sales are here to stay for the long term, Spectrum is probably a good buy at this point. I don't have that confidence; I'm not confident they'll go away, either, so I wouldn't short the stock.

Sometimes you can lay out the risks and benefits of own a company and decide the company is just too hard to read to justify an investment. In that case, most investors would be best off watching from the sidelines.

The corollary, of course, is to invest in what you know. The Fool's free report has three suggestions for companies that middle-class America should be keenly aware of. Get your copy for free.

The article 3 Reasons to Sell Spectrum Pharmaceuticals originally appeared on Fool.com.

Fool contributorBrian Orelliholds no position in any company mentioned. Check out hisholdings and a short bio. We Fools don't all hold the same opinions, but we all believe thatconsidering a diverse range of insightsmakes us better investors. Try any of our Foolish newsletter servicesfree for 30 days. The Motley Fool has adisclosure policy.

Copyright © 1995 - 2012 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.