When Will the Market Like Facebook Again?

Shares of Facebook (NAS: FB) have been unfriended by more than a few investors this month, and the social network continues to hit new all-time lows in its short public life. Let's take a look at how it got here to find out whether there are still cloudy skies ahead.

How it got here

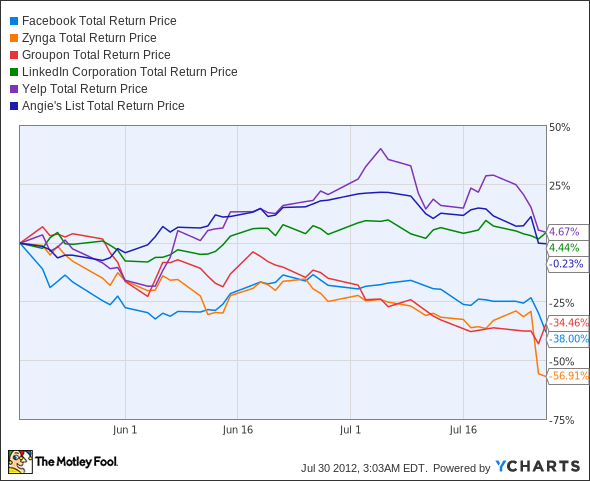

Facebook's semi-symbiotic relationship with social-game maker Zynga (NAS: ZNGA) was front and center last week. Zynga's terrible earnings report started a slide that only gained steam once Facebook's own earnings showed progress that fell below the Street's lofty expectations.

The New York Times now hears "echoes of the crash of 2000," although this one is pretty quiet, since the Times only bothered to identify four stocks crashing. Groupon (NAS: GRPN) has been a worse performer than Facebook since the latter's IPO and has lost an astounding 71% of its value since going public last November.

Netflix, the Times' fourth horseman of Dot-comageddon, is cheap compared to any of these companies, and it isn't even a social play. Yelp (NAS: YELP) and Angie's List, both pure social plays, are flat for the post-Facebook period. Meanwhile, LinkedIn (NAS: LNKD) soldiers on.

FB Total Return Price data by YCharts.

If this is a sign of a new tech bust, it's a pretty hazy one. Why has the market soured so much more on Facebook (and, to a similar extent, Groupon and Zynga) than it has on Angie's List and Yelp, which have never turned a profit or had positive free cash flow? Let's take a look at the numbers.

What you need to know

Facebook shares a couple of stock-valuation similarities with LinkedIn. They're the only two profitable companies on this social-media list, and they're both valued at double-digit price-to-sales ratios. That's about where the similarities end, since Facebook has lost a third of its value since going public, while LinkedIn is the only gainer on our list:

Company | P/E Ratio | Price to Sales | Market Cap | Change From IPO |

|---|---|---|---|---|

82 | 10.3 | $65 billion* | (37.6%) | |

Zynga | NM | 1.8 | $2.3 billion | (67.5%) |

Groupon | NM | 2.6 | $4.9 billion | (70.9%) |

708.4 | 17.3 | $10.7 billion | 11.1% | |

Yelp | NM | 12.7 | $1.2 billion | (20.6%) |

Angie's List | NM | 6.3 | $748 million | (19.8%) |

Source: Yahoo! Finance and Google Finance. NM = not material due to negative earnings.

*Facebook's market cap is misrepresented on most major finance sites.

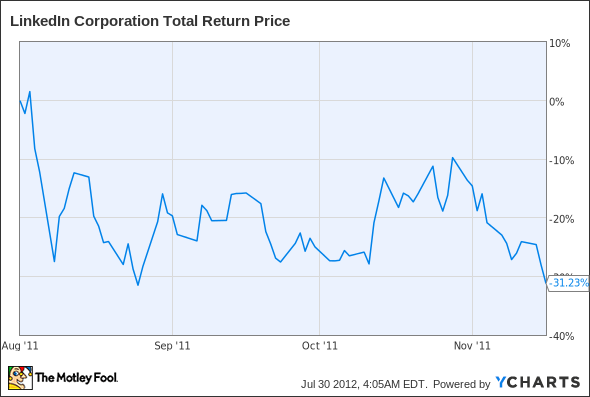

There aren't a lot of conclusions that can be drawn by simply examining this list. Why has LinkedIn been so resistant to the declines plaguing its social peers? Zynga and Groupon have been savaged by the financial press -- perhaps more than Facebook, despite the greater interest nonfinancial media has given to Facebook's major moves. LinkedIn, Yelp, and Angie's List have been wallflowers by comparison, but it's also worth considering timing. From its IPO until its secondary offering in mid-November, LinkedIn performed nearly as poorly as Facebook has:

LNKD Total Return Price data by YCharts.

As you can see, LinkedIn plunged -- only to go on a tear that has lasted to the present day:

LNKD Total Return Price data by YCharts.

Will Facebook soon have a turnaround of its own? Its growth rates are less impressive than those of LinkedIn, which has doubled its revenue last quarter from the year-ago quarter. Facebook has a much bigger user base to contend with, which makes a promise of outsized growth much harder to keep. On the other hand, Facebook won't have as far to fall to be considered "cheap."

What's next?

Facebook is closer to LinkedIn than it is to Zynga or Groupon, which have both had their business models under well-deserved scrutiny since going public. Facebook's clearly profitable, though its profit growth seems to be slowing. It has multiple streams of revenue -- although I'm not sure how long Facebook should (or will) rely on Zynga as a major secondary source of revenue.

The Motley Fool's CAPS community has given Facebook a one-star rating, with 57% of our CAPS players expecting the company to keep dropping. Our players clearly don't think Facebook is cheap yet.

Interested in tracking this stock as it continues on its path? Add Facebook to your Watchlist now, for all the news we Fools can find, delivered to your inbox as it happens. Facebook might not be the growth story of the year, but there are plenty of opportunities if you know where to look. "The Motley Fool's Top Stock for 2012" is one. The report on this potential multibagger is free for a limited time, so get the information you need while it lasts.

The article When Will the Market Like Facebook Again? originally appeared on Fool.com.

Fool contributor Alex Planes holds no financial position in any company mentioned here. Add him on Google+ or follow him on Twitter @TMFBiggles for more news and insights.The Motley Fool owns shares of Facebook, Linkedin, and Netflix. Motley Fool newsletter services have recommended buying shares of Facebook, Linkedin, and Netflix. The Motley Fool has a disclosure policy. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. Try any of our Foolish newsletter services free for 30 days.

Copyright © 1995 - 2012 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.