Sprint Strikes a 52-Week High: Are More Gains Ahead?

Shares of Sprint (NYS: S) hit a 52-week high last week, finally reversing a long slide. Let's take a look at how it got here to find out whether there are clear skies ahead.

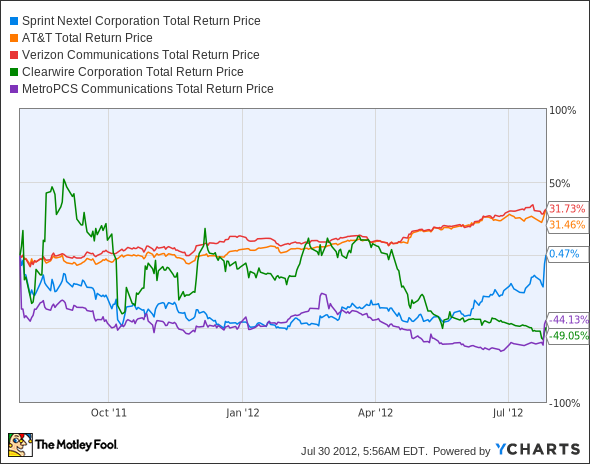

How it got here

Sprint's still unprofitable, but there seems to be light at the end of its tunnel at last. The company's Nextel dead weight is nearly shed, and revenue per user ticked up in its most recent quarter. There was enough good news in Sprint's quarterly earnings to lift network provider Clearwire (NAS: CLWR) -- but the latter's own report wasn't bad, either. One key difference between Sprint and its network provider is that Sprint's been edging up all year, and last week's move finally brought it into positive territory for the past 52 weeks:

S Total Return Price data by YCharts.

Smaller carrier MetroPCS (NYS: PCS) also had good news last week, but like Clearwire, it has a long way to go to erase the past year's slide. Carriers (NYS: T) and (NYS: VZ) have ridden their safe status to straight-line gains, and remain the gold standard for domestic telecom investments. Will Sprint's latest move be the start of a longer period of growth, or is it destined to continue underperforming the big two? Let's look closer at the numbers to find out.

What you need to know

Sprint's got a way to go yet, as its price-to-free-cash-flow ratio is still much higher than AT&T or Verizon's. It's also considerably more expensive than MetroPCS, which has done quite well without the same high level of capital expenditures as the major wireless carriers:

Company | P/E Ratio | Price-to-Free-Cash-Flow Ratio | Debt-to-Equity Ratio | Trailing-12-Month Capital Expenditures |

|---|---|---|---|---|

Sprint | NM | 57.3 | 2.1 | $3.51 billion |

Clearwire | NM | NM | 4.2 | $156 million |

MetroPCS | 10.0 | 14.0 | 1.5 | $786 million |

AT&T | 53.8 | 15.4 | 0.6 | $20.27 billion |

Verizon | 48.1 | 8.4 | 1.3 | $14.45 billion |

Source: Morningstar. NM = not meaningful due to negative results.

One major positive for Sprint in this comparison is that, despite its higher level of debt, it's done a better job at retiring that debt than its telecom peers:

S Long Term Debt data by YCharts.

Sprint still maintains over $20 billion in long-term debt, but efforts toward paying it off seem to be winning over Wall Street. Since Sprint's bonds have lower credit ratings than AT&T and Verizon, it has somewhat more impetus to lower its debt levels. As it sheds Nextel assets and starts making the most of its iPhone subscribers, Sprint ought to be in better shape to retire more debt.

What's next?

Sprint may have better times ahead, but long-term shareholders are still far away from the levels seen five years ago. Sprint's still 80% below its 2007 highs. Can this turnaround sustain enough momentum to recapture those highs? Sprint hasn't been profitable in years, and its free cash flow's also been diminished in the past few quarters. Regaining profitability might not be on the near-term horizon, but a strong showing on the cash flow statement next quarter would be a big sign that this rally's sustainable.

The Motley Fool's CAPS community has given Sprint a two-star rating, but 81% of our CAPS players expect the company to beat the market in the future.

Interested in tracking this stock as it continues on its path? Add Sprint to your Watchlist now, for all the news we Fools can find, delivered to your inbox as it happens. Sprint might keep gaining, but you can't tie your hopes up in one stock. Diversify into other long-term opportunities, which you can read about here: "3 Stocks That Will Help You Retire Rich." Find out more about them in our free report -- click here to get the information you need today.

The article Sprint Strikes a 52-Week High: Are More Gains Ahead? originally appeared on Fool.com.

Fool contributor Alex Planes holds no financial position in any company mentioned here. Add him on Google+ or follow him on Twitter @TMFBiggles for more news and insights.The Motley Fool has a disclosure policy. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. Try any of our Foolish newsletter services free for 30 days.

Copyright © 1995 - 2012 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.