3 Good Lines for Align

Investors in Align Technology (NAS: ALGN) have plenty to smile about. Shares in the medical-device company are up more than 50% in the past year. More smiles might be on the way if the following three trend lines mean what I think they mean.

1.Teen population

Align's Invisalign system helps treat malocclusion (misaligned teeth) using plastic orthodontic aligners. The company touts several benefits that Invisalign offers compared with braces, including near-invisibility, comfort, and easier dental hygiene.

As you might expect, the teen market helped drive Align's growth in recent years. Most of the company's sales are generated from North America, Europe, and Japan. Why stop at the developed nations? Align isn't.

The company has taken steps to expand globally beyond its core markets. In 2011, Align launched Invisalign in several of the largest cities in China. It also has distribution partners in other emerging markets, including Latin America and Russia.

What does the potential teen market look like for the less developed nations?

Source: United Nations Population Division data and author extrapolations.

Despite a plateau beginning after 2005, the growth in the less developed world's teen population should resume a nice uptrend within a few years. That could present great opportunities for Align down the road.

There is a bit of good news for developed nations as well. While the teen population in these countries has declined over the past decade, UN data shows that increasing birth rates in recent years should lead to a rebound in the near future.

2.Trained doctors

Since only trained doctors can provide Invisalign to patients, Align's fortunes depend on how many professionals know how to follow the process. With greater growth prospects in international markets, training dentists and orthodontists in other countries is important. How do things look on this front?

Source: Company 10-K reports.

Source: Company 10-K reports.

Source: Company 10-K reports.

Align Technology has seen steady growth in the number of trained international professionals in the past three years. The temporary slower increase in 2011 resulted from delaying training while the rollout of the new Invisalign G3 product was completed.

Another positive trend is a slight increase in the average number of cases that each doctor purchases from Align. More doctors times more products shipped per doctor equals more good news for the company.

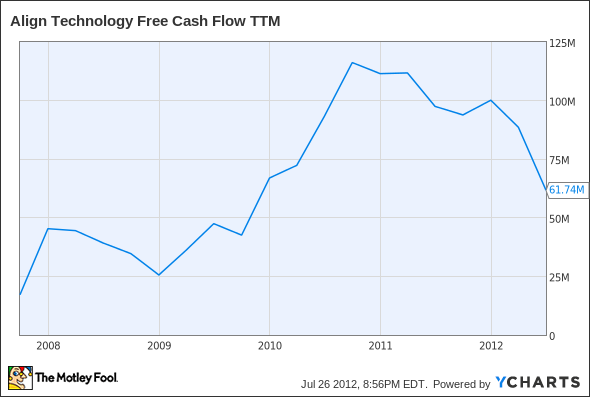

3.Free cash flow

Here's a look at the trend for Align's free cash flow on a trailing-12-month basis.

ALGN Free Cash Flow TTM data by YCharts

Everything looks great through 2011, but then free cash flow starts falling. That can't be good, right? Actually, it can.

The primary reason for the decline is Align's acquisition of Cadent in 2011. Cadent makes 3-D digital scanning solutions for orthodontics and dentistry. A doctor who uses Cadent's intra-oral scanner can make digital scans of a patient's mouth and send the scan electronically to Align. Align then uses the 3-D scan to rapidly manufacture custom aligners specifically for the patient. The older method required the doctor to make a polyvinyl-siloxane impression of the patient's mouth and ship the physical impression to Align.

Cadent looks like a good fit. My view is that this acquisition will prove to be a big positive for Align over the long run.

Other lines

Not every line is good news for Align. Fellow Fool Seth Jayson makes a solid argument in a recent article on why the company's earnings aren't as good as they might seem. The lineup of rivals looks tough as well.

Giant 3M (NYS: MMM) makes many products, including orthodontic appliances. The company's Incognito invisible braces particularly directly challenge Invisalign, while 3M's 3-D scanners go head-to-head with Cadent scanners.

Sirona Dental (NAS: SIRO) touts itself as the world's largest manufacturer of dental technology. Its 3-D scanners also compete against the Cadent scanners. Dentsply (NAS: XRAY) is yet another rival. The company makes products that could be considered threats to Invisalign.

Then there's the complex relationship with Danaher (NYS: DHR) . A legal settlement in 2009 gave Danaher 10% ownership in Align. The two companies agreed to a seven-year deal to collaborate on a joint product but still compete against each other.

Bottom line

Several trends appear to be in Align's favor. Should investors buy now?

The stock seems to be priced highly, with a trailing P/E of 32. This multiple is significantly higher than the values for any of the competitors mentioned here. It might be best to wait for a pullback before buying. After all, the most important line is your bottom line.

For some more great ideas for your bottom line check out The Motley Fool's free report "3 Stocks That Will Help You Retire Rich". Get your free copy now.

The article 3 Good Lines for Align originally appeared on Fool.com.

Fool contributorKeith Speightsowns no shares in the stocks mentioned above.Motley Fool newsletter serviceshave recommended buying shares of 3M and creating a diagonal call position in 3M. We Fools don't all hold the same opinions, but we all believe thatconsidering a diverse range of insightsmakes us better investors. Try any of our Foolish newsletter servicesfree for 30 days. The Motley Fool has adisclosure policy.

Copyright © 1995 - 2012 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.