Is This Growth Stock a Misunderstood Value Play?

There are many moving parts in VMware's (NYS: VMW) stock price today:

The second-quarter report showed 22% revenue growth and 24% higher non-GAAP earnings year over year, beating Wall Street's earnings estimates while matching sales expectations. All of this was in line with the pre-announcement VMware made last week.

VMware also announced a $1.3 billion acquisition, adding software-based networking expert Nicira to the business portfolio. That's a big, splashy splurge that overshadows the four completed and one pending buyouts VMware has conducted in the last 12 months. Nicira brings along an all-star cast of clients, including key cloud computing player Rackspace Hosting (NAS: RAX) and all-around Internet titan eBay (NAS: EBAY) , showing the large-scale applications of its unique networking technologies.

Management is very cautious about sales trends in the third quarter, because federal spending could be soft in this election year and you never know what Europe will do next. All told, third-quarter sales growth should slow down somewhat to roughly 20% year over year. The Nicira buy won't make a significant difference to this year's results.

If you thought that VMware would be a totally different animal under incoming CEO Pat Gelsinger, it seems you'd be wrong -- despite Gelsinger's hardware expertise from years of service at Intel (NAS: INTC) , he must have given at least rubber-stamp approval to this software deal.

In fact, Gelsinger showed up to this week's earnings call despite the fact that he's not taking office until August, and talked himself warm over the opportunity to manage network architectures with pure software tools. He seems pretty excited about the whole Nicira idea.

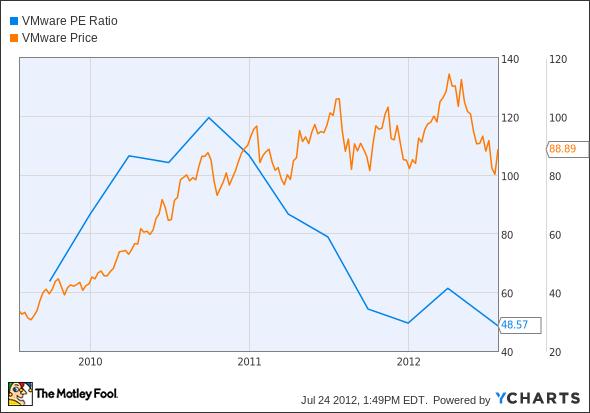

All things considered, this was another fine quarter for VMware that answered more questions than it raised. It's not a traditional value stock by any means, but the forward P/E ratio has slithered below 30. For a high-octane grower like VMware, that's pretty affordable. And it's getting cheaper thanks to rising fundamentals, not a plunging share price:

VMW P/E Ratio data by YCharts.

The stock honestly should have popped on a report like this, but instead muddled along with a confused market. I just started a bullish CAPScall on VMware to capture this insidious discount while it's still available. But if the risk-reward ratio in this growth stock still rattles your nerves, The Fool has found a no-brainer growth company worthy of being called "The Motley Fool's Top Stock for 2012." Click here to learn more, but hurry while the report is still totally free.

The article Is This Growth Stock a Misunderstood Value Play? originally appeared on Fool.com.

Fool contributorAnders Bylundholds no position in any of the companies mentioned. Check outAnders' holdings and bio, or follow him onTwitterandGoogle+. The Motley Fool owns shares of Intel.Motley Fool newsletter serviceshave recommended buying shares of Rackspace Hosting, eBay, Intel, and VMware. The Motley Fool has adisclosure policy. We Fools may not all hold the same opinion, but we all believe that considering a diverse range of insights makes us better investors. Try any of our Foolish newsletter servicesfree for 30 days.

Copyright © 1995 - 2012 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.