3 Big Pharma Plays for Your Portfolio

Heavyweight prizefighter Jack Dempsey once said, "The best defense is a good offense," but the terms have been reversed to be, "The best offense is a good defense." For investing, I prefer the latter. Stocks in the health-care sector of the Standard & Poor's indexes are recognized as defensive plays; i.e., when you feel like the market is about to send your portfolio down for the count, you want to be invested in stocks that can take the hits and last the entire fight.

Several big pharmaceutical companies are set to report earnings next week, among them Bristol-Myers Squibb (NYS: BMY) , Eli Lilly (NYS: LLY) , and Amgen (NAS: AMGN) . Rather than rely on analysts' recommendations, let's take a look at these stocks for earnings expectations, and more importantly earnings quality.

The Motley Fool Earnings Quality Score database looks at stocks in the S&P indexes and ranks them "A" through "F" based on price, cash flow, revenue, and relative strength among other things. Stocks with poor earnings quality tend to underperform, so we look for trends that might predict future outcomes.

Bristol-Myers Squibb | Eli Lilly | Amgen | |

|---|---|---|---|

Listed Reporting Date | July 25 | July 25 | July 26 |

Estimated EPS (quarter) | $0.49 | $0.76 | $1.54 |

Year-Ago EPS (quarter) | $0.56 | $1.18 | $1.37 |

YOY % Change | (12.50%) | (35.59%) | 12.41% |

Estimated Revenue (billions) | $4.46 | $5.58 | $4.08 |

Year-Ago Revenue (billions) | $5.43 | $6.25 | $3.96 |

YOY % Change | (17.86%) | (10.72%) | 3.03% |

EQ Score (week of 7/13) | F | C | F |

Source: Biz.Yahoo.Com!

Bristol-Myers Squibb | Eli Lilly | Amgen | |

|---|---|---|---|

Estimated EPS (year) | $1.93 | $3.29 | $6.15 |

Year-Ago EPS (year) | $2.28 | $4.41 | $5.33 |

YOY % Change | (15.35%) | (25.40%) | 15.38% |

FY Estimated Revenue (billions) | $17.95 | $22.69 | $16.38 |

Last Full Year Revenue (billions) | $21.46 | $24.29 | $15.58 |

YOY % Change | (16.36%) | (7.05%) | 5.13% |

Source: Biz.yahoo.com.

Bristol-Myers Squibb

Bristol-Myers displays improved gross, operating, and net profit margins over the last two years, as well as declining costs and higher operating and net income. Cash management issues have hurt earnings quality. Accounts receivables and inventory levels are trending upward, and days in inventory have increased to 102 days. Bristol is also slow to pay creditors, as days payable outstanding has increased from 125 at 167 days in two years. This demonstrates Bristol's manipulation of cash flow.

Bristol also has been busy spending cash, as the last 12 months show a lot of activity. Bristol had net income of $3.824 billion, and $4.746 billion in cash from operations, but spent $2.851 billion on acquisitions; $705 million net to repurchase shares and $2.268 billion for dividends, ending with -$1.098 billion change in cash. Bristol recently acquired Amylin Pharmaceuticals, which gives it diabetes drug Bydureon. This acquisition should be accretive to earnings going forward, but we'll have to wait and see.

Bristol's philosophy over the last several years has been to reward very patient investors with generous dividends (currently $1.36 annually, yielding 3.8%), while it works to land its next big blockbuster drug to achieve capital appreciation. The Amylin deal may contribute toward the growth goal. The stock has only increased 1.26% since the start of 2012, from $35.01 to $35.45 currently. If you think you can live with a 5% return and good appreciation potential with the Amylin acquisition, then Bristol-Myers is a consideration. And remember -- it's about defense.

Eli Lilly

Lilly has the lowest P/E ratio (11.45) and highest dividend ($1.96, or 4.4% yield) of the group. Its earnings story is also estimated to be the worst of the group on declining revenues, which is no doubt the reason for the low P/E. Operating and net profit margins, while acceptable at 25% and 18%, respectively, have been declining. Inventory levels are low and declining but days in inventory are high at 185 days. Receivables and payables are on a par with the competition, which means they aren't great.

Debt is a modest 27% of revenue. Last-12-months cash flows include $1.537 billion debt repaid, $2.181 billion dividends paid, $503 million in acquisitions, and $3.360 billion invested in securities. Net change in cash is -$2.384 billion. Lilly has added 13.6 million shares since 2010. This means two things: Per-share earnings are diluted with the added shares, and cash is not being used to repurchase shares. The stock has appreciated 5.67% during the year.

Lilly needs a megadrug, and fortunately it has several diabetes drugs in late-stage trials along with Alzheimer's treatment solanezumab. Despite its earnings outlook, Lilly could see significant price appreciation if these drugs are successful. In my opinion, Lilly is worthy of a position in a defensive portfolio.

Amgen

Amgen is estimated to achieve the best revenue and earnings gains of our group, and will doubtless receive buy recommendations from analysts. But the stock has appreciated 21.37% since January, which is more than estimates warrant. Moreover, costs are rising and operating and net profit margins have declined since 2010. The operating cash flow margin last 12 months has also been declining.

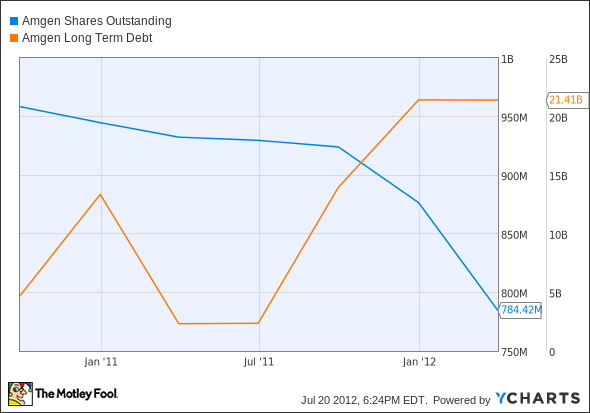

Inventory levels, receivables and days sales outstanding are all rising. Days in inventory are 336 days, and the cash conversion cycle is 284 days. Come on! The chart below shows a sickly tactic to boost earnings. Debt has doubled since 2010 and Amgen spent $9.3 billion to repurchase shares. Take two aspirin and don't call me in the morning.

AMGN Shares Outstanding data by YCharts

Foolish bottom line

Defensive, dividend-paying stocks are the tonic for what is ailing your portfolio, but don't be fooled by misguided analysts' recommendations. Foolish readers should base investment decisions on earnings quality.

If you like dividends, don't forget to get your copy of the Motley Fool report "Secure Your Future With 9 Rock-Solid Dividend Stocks." To see which dividends made the grade, click here now.

At the time thisarticle was published Fool contributorJohn Del Vecchiois Co-Advisor to Motley Fool Alpha and co-manager of the Active Bear ETF (NYS: HDGE) . You may follow him on Twitter @johnfdelvecchio. He does not own any shares in the companies mentioned in this article.The Motley Fool has adisclosure policy.We Fools may not all hold the same opinions, but we all believe thatconsidering a diverse range of insightsmakes us better investors. Try any of our Foolish newsletter servicesfree for 30 days.

Copyright © 1995 - 2012 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.