Is Walgreen a Buy Today?

Shares of Walgreen (NYS: WAG) climbed more than 10% yesterday on news that the drugstore and pharmacy benefits manager Express Scripts (NAS: ESRX) finally reunited after a messy breakup earlier this year. The market is rewarding both of these stocks on their new multiyear agreement. However, I don't think Walgreen is out of the woods just yet.

Let's take a closer look at the implications of the new reimbursement deal and see why investors may want to sit on the sidelines before jumping into shares of Walgreen.

The damage is done

Relationships, especially professional ones, often require compromises between those involved. Unfortunately for Walgreen, it took nearly seven months to finally reach an understanding with Express Scripts -- a drawn-out process that cost the country's largest drugstore chain billions in sales.

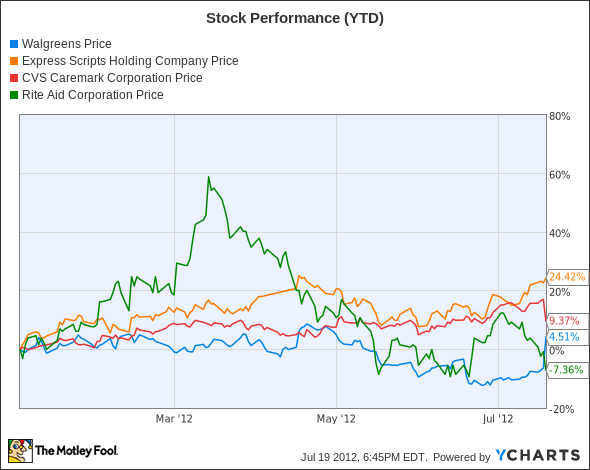

In addition to lost revenue, the dispute also boosted business for Walgreen's competitors, including CVS Caremark (NYS: CVS) and Rite Aid (NYS: RAD) . That's because after the pharmacy retailer refused to renew its contract with Express Scripts, millions of patients in the Express network were forced to fill their prescriptions elsewhere.

Aggressive marketing campaigns by both CVS and Rite Aid earlier this year also didn't help. CVS ran an ad saying: "Have you been notified that your pharmacy may stop accepting your Express Scripts insurance? We can help." Now it's Walgreen's turn to incentivize customers to return, which won't be easy.

Playing nice

Having now made peace with the pharmacy benefits manager, Walgreen is hoping to pick up the pieces. However, being back in the Express Scripts network may not be enough for Walgreen to win back lost members.

In fact, CEO Larry Merlo of rival CVS is confident that his company can hold on to at least half of the customers it's gained so far from Walgreen. And who can blame him? Anyone who has ever transferred prescriptions from one pharmacy to another knows how frustrating the process can be.

This is likely to have a negative impact on the company's earnings in the quarters to come.

All told, I expect pharmacy sales at Walgreen to continue to slide in the second half of the year, despite its newly inked contract with Express Scripts. While the stock was riding higher this week on the news, let's see how it measures up to industry peers year to date.

Walgreen hasn't been an investor favorite in recent months. At the same time, shares of the pharmacy retailer boast an attractive dividend yield of 3.2% and trade at just over 11 times earnings. It's also worth considering that Walgreen has a rich history of rewarding patient shareholders. Last month, management raised its quarterly payout by more than 22% to just over $0.27 a share, or $1.10 annually.

But wait, there's more

Enticing dividends and strong financials bode well for investors. However, to be fair we need also consider the added risks brought on by Walgreen's recent $6.7 billion splurge on a portion of European drugstore chain Alliance Boots. That's an expensive bid for what is said will be a 45% stake in Boots.

As if gaining major European exposure during a time of such uncertainty in the region isn't bad enough, Walgreen also plans to take on billions in debt to fund the cash-and-stock deal. At this point, I'm finding it difficult to see the value in what appears to be a risk-all play.

Take it or leave it?

With all the pros and cons, what's an investor to do? Walgreen gets high marks for its position as an industry leader and overall healthy balance sheet. Still, there's no denying that management's initial decision to drop Express Scripts was a bonehead move that will probably haunt Walgreen into fiscal 2013. The seemingly sporadic merger with the European pharmacy giant also adds unnecessary risk to this name.

Given these reasons, I think investors would be wise to sit this one out -- at least while Walgreen navigates new British drug regulations and works toward rebuilding its status within the Express Scripts network. In the meantime, I invite you discover three winning stocks with solid dividend payouts in this free report from The Motley Fool. Get instant access to this free report, while it's still available.

The article Is Walgreen a Buy Today? originally appeared on Fool.com.

Fool contributor Tamara Rutter owns no shares of any companies mentioned in this column. Follow her onTwitter, where she uses the handle@TamaraRutter, for more Foolish insights and investing advice. The Motley Fool owns shares of Express Scripts. Motley Fool newsletter services have recommended buying shares of Express Scripts. We Fools don't all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. Try any of our Foolish newsletter services free for 30 days. The Motley Fool has adisclosure policy.

Copyright © 1995 - 2012 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.