Will Nike's Performance Influence Its Olympics Success?

Nike (NYS: NKE) is the undisputed world's largest sporting goods equipment and clothing manufacturer. On June 28, Nike reported a rare quarterly earnings miss, citing $1.17 EPS versus the Street's estimated $1.37. Nike ended its fiscal year at $4.73 EPS versus an estimated $4.93. Despite raising prices last year, quarterly revenue came in lighter than estimated also: $6.47 billion versus $6.51 estimated.

Mark Parker, CEO, noted in the latest earnings conference call:

We've faced significant input cost pressures throughout the year, as well as some unexpected items in the fourth quarter... we remain confident that our earnings will grow faster than revenue over the long-term... We will see continued uncertainty in the global economy, commodities and labor costs will continue to fluctuate, currency pressures increase, especially in Europe and the Emerging Markets and China's economy is expected to grow more slowly than we've seen over the past 5 years.

Starting with Income Statement metrics, we see revenue increasing but margins and earnings numbers reversing and trending lower over the last fiscal year. This reinforces Mr. Parker's comment regarding cost pressures.

Quarterly Results | May 31, 2012 | May 31, 2011 | May 31, 2010 |

|---|---|---|---|

Revenue (millions) | $6,470 | $5,766 | $5,077 |

YOY % Change | 12.21% | 13.57% | |

Cost of Goods Sold % Revenue | 57% | 54% | 53% |

Operating Income (millions) | $743 | $773 | $683 |

YOY % Change | (3.88%) | 13.18% | |

Net Income (millions) | $549 | $594 | $522 |

YOY % Change | (7.58%) | 13.79% | |

Earnings per Share | $1.17 | $1.23 | $1.05 |

YoY % Change | (4.88%) | 17.14% |

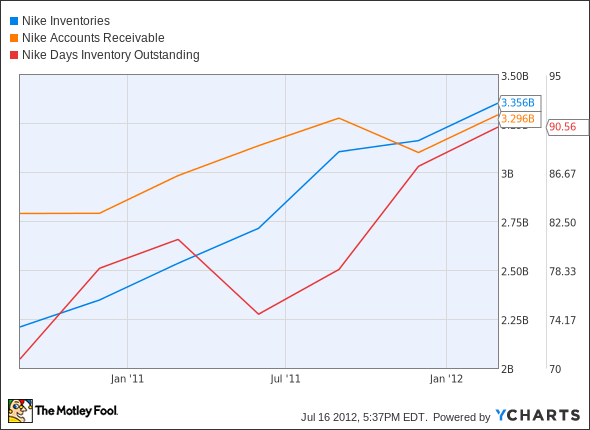

But the chart below explains why one of the world's most endeared brands has poor earnings quality. The Motley Fool's earnings quality score database has consistently ranked Nike between "F" and "D" since the start of the year.

NKE Inventories data by YCharts (Note: Chart reflects data up to Feb. 29, 2012.)

Quarterly Results | May 31, 2012 | May 31, 2011 | May 31, 2010 |

|---|---|---|---|

Inventories | $3,350 | $2,715 | $2,041 |

YOY % Change | 23.39% | 33.03% | |

Accounts Receivable (millions) | $3,280 | $3,138 | $2,650 |

YOY % Change | 4.53% | 18.42% | |

Days in Inventory | 83 | 77 | 70 |

YOY % Change | 7.79% | 10.00% |

S&P Capital IQ.

The chart above reflects data ending Feb. 29, 2012, but the table has the most recent data. They both show that Nike has had a growing inventory problem. Inventory growth is outpacing revenue growth. "Cost pressures" have forced price hikes, but retailers and sports aficionados are not sidling up to the starting line. Excess inventory can only be moved via price discounts, and will cause a lower "swoosh" on Nike's margins.

Mr. Parker commented he thinks Nike's earnings will grow faster than revenue over the long term. Nike did in fact advance earnings 17% based on revenue growth of 13% last year, but this year inventories and input costs outpaced revenue. However, Nike has been reducing its shares outstanding to boost net income and earnings numbers. Last quarter the tactic worked as well as a pair of worn-out Air Jordan sneakers. One positive is that Nike has been paying down long-term debt, and so it does not appear to be using debt to fund its share repurchases.

NKE Shares Outstanding data by YCharts

Nike still has trailing and forward P/E ratios of 19.59 and 15.66, respectively. Nike's dividend yield is 1.5% ($1.44 per share). Analysts estimate next year's earnings to increase 10% to $5.21 per share, and sales to be at $25.34 billion -- a 5% increase. Yes, Nike is the dominant industry player. Yes, Nike's stable includes superstar athletes like Michael Jordan, Tiger Woods, and LeBron James. No, the metrics don't justify Nike's stock price. If you own it, hold it. If you're looking to get in, wait for Europe's situation to improve.

The competition

Two major competitors are Adidas and Puma. Both companies are on the DAX German Stock Exchange, so comparison is difficult. Nonetheless, summary tables follow.

Adidas | Dec. 31, 2011 | YOY % Change | Dec. 31, 2010 | YOY % Change | Dec. 31, 2009 |

|---|---|---|---|---|---|

Revenue | 13,344 | 11.29% | 11,990 | 15.50% | 10,381 |

Net Income | 670 | 17.96% | 568 | 131.84% | 245 |

EPS | 3.21 | 18.45% | 2.71 | 116.8% | 1.25 |

Inventories | 2,482 | 17.13% | 2,119 | 44.05% | 1,471 |

Accounts Receivable | 1,707 | 2.4% | 1,667 | 16.66% | 1,429 |

Source: S&P Capital IQ. In millions (euros) except per-share data.

Puma | Dec. 31, 2011 | YOY % Change | Dec. 31, 2010 | YOY % Change | Dec. 31, 2009 |

|---|---|---|---|---|---|

Revenue | 3,009 | 11.18% | 2,706.4 | 10.59% | 2,447.3 |

Net Income | 230.4 | 13.95% | 202.2 | 161.58% | 77.3 |

EPS | 15.36 | 14.20% | 13.45 | 154.73% | 5.28 |

Inventories | 587.1 | 9.37% | 536.8 | 22.08% | 439.7 |

Accounts Receivable | 533.1 | 19.26% | 447 | 28.67% | 347.4 |

Source: S&P Capital IQ. In millions (euros) except per-share data.

Both companies have returned better results to shareholders over the past two years than has Nike. Of the three, Puma appears to have the highest margins, although Adidas appears to be growing faster.

Under Armour (NYS: UA) and lululemon athletica (NAS: LULU) can be considered Nike competitors in the sports apparel space. Under Armour has a high P/E ratio of 51 and a forward P/E of 32, both higher than its price performance and its revenue growth (22.8%) or earnings growth (26.88%) estimates. Accounts receivable, inventory levels, and days in inventory (now at 141 days) have all more than doubled in the past two years while revenue has increased only 68%. Inventory as a percent of revenue is high at 84%. Under Armour has an earnings quality score of "F" and will likely be an underperformer.

By contrast, Lululemon's revenue has more than doubled since 2010, and so has its earnings per share. Inventory levels are much lower than Under Armour's, and inventory turns are shorter at 77 days. Lululemon has almost no accounts receivable and no long-term debt. Lululemon's forward P/E of 26 is lower than EPS growth estimate of 28% and its estimated sales growth of 35%. I would rate this stock a buy.

Foolish takeaway

With the Summer Olympics starting later this month, the battle may often be between global brands as well as individual competitors and nations. Foolish readers should base investment decisions on earnings quality.

Nike makes our list of 3 American Companies Set to Dominate the World, but what are the other two? Pick up a copy of our special report to find out. It's entirely free of charge, so claim your copy today by clicking here.

The article Will Nike's Performance Influence Its Olympics Success? originally appeared on Fool.com.

Fool contributorJohn Del Vecchiois co-advisor to Motley Fool Alpha and co-manager of the Active Bear ETF (HDGE). You may follow him on Twitter @johnfdelvecchio. He does not own any shares in the companies mentioned in this article. The Motley Fool owns shares of Under Armour and lululemon athletica.Motley Fool newsletter serviceshave recommended buying shares of lululemon athletica, Under Armour, and Nike.Motley Fool newsletter serviceshave recommended creating a diagonal call position in Nike.Motley Fool newsletter serviceshave recommended creating a bear put spread position in Under Armour. The Motley Fool has adisclosure policy.We Fools may not all hold the same opinions, but we all believe thatconsidering a diverse range of insightsmakes us better investors. Try any of our Foolish newsletter servicesfree for 30 days.

Copyright © 1995 - 2012 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.