Why This AuRico Gold Smackdown Is Way Overdone

Even in the absence of the prolific dealmaker who built this well-positioned mid-tier gold producer, the shares of AuRico Gold (NYS: AUQ) are bound to see meaningful appreciation from this latest 52-week low.

AuRico shares careened as much as 17% lower on Tuesday after back-to-back press releases combined a reduction in anticipated 2012 output from the Ocampo mine in Mexico with news of CEO Rene Marion's looming departure for health reasons. Marion will step down (effective September 3) due to "a non-life threatening degenerative medical condition that will require his full attention as he undergoes treatment." Marion will stay on as a strategic advisor to the board of directors, while executive vice president and CFO Scott Perry will step into the CEO role.

Importantly, the chief operating officers for Canada and Mexico will remain in their respective positions. The company's Ocampo mine struggled with "unusually high turnover of skilled labor" that affected underground production during the second quarter. AuRico has responded with an "aggressive recruiting campaign," and will now look to contractors to assist with accelerated underground development. In light of the challenges at Ocampo, the uninterrupted oversight by COO Russell Tremayne will provide valuable continuity through the impending CEO transition.

Likewise, the ongoing ramp-up to commercial production at the Young-Davidson mine in Ontario will remain under the direction of COO for Canada operations Peter MacPhail. MacPhail has been with the project throughout the development process, having served for eight years as COO to prior owner Northgate Minerals before joining AuRico when they acquired Northgate last year. Young-Davidson remains on track to achieve commercial production during August, and to meet 2012 production guidance during this key phase of project execution.

Rene Marion cemented his reputation as a cunning industry consolidator by snatching Capital Gold and its producing gold mine El Chanate from rival bidder Timmins Gold (NYS: TGD) , even after Capital Gold stakeholder Sprott Asset Management threw its weight behind Timmins with a line of credit from Sprott Resource Lending. Next, Marion swooped in on Primero Mining (NYS: PPP) to block its proposed transaction with Northgate by issuing a superior and ultimately successful bid. Marion made both of these transformative moves during 2011, and in the process dealt his way into one of the industry's strongest production-growth trajectories. In May, AuRico divested its Australia operations for $55 million in cash. And just this week, the company completed the sale of its El Cubo mine and Guadalupe y Calvo development project to Endeavour Silver (NYS: EXK) for total consideration of up to $250 million. Taken together with its prior cash balance, these divestitures will stuff AuRico's treasury with roughly $380 million in cash and equity investments at a moment when additional strategic transactions are prime for the picking. The company also commands a $250 revolving credit facility for total liquidity of more than $600 million. Yamana Gold (NYS: AUY) placed the gold world on notice last month to watch for a major round of consolidation, and AuRico Gold is sitting pretty as a potential strategic buyer.

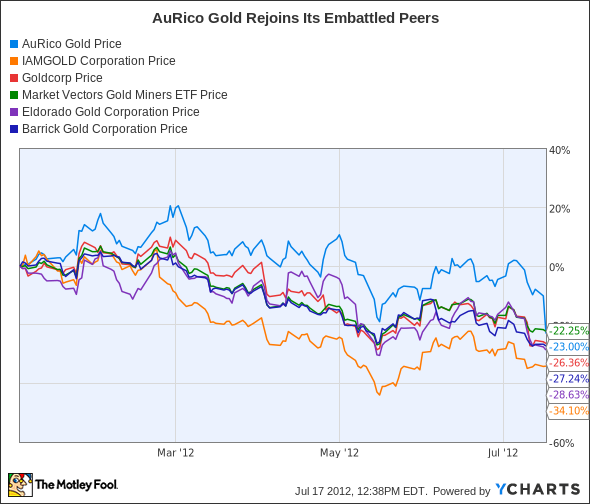

But, particularly following Tuesday's brutal sell-off, little reflection of those trailing strategic successes and exciting opportunities for continued growth can be seen in the stock's valuation. As the above year-to-date chart shows, AuRico outperformed its peer group throughout the first half of 2012, but abruptly rejoined the pack this week. Despite the modest setback at Ocampo, I still expect AuRico to produce at least 300,000 gold-equivalent ounces (GEOs) during 2012, and the company this week reiterated its guidance for between 390,000 and 445,000 GEOs for 2013 and between 450,000 and 530,000 GEOs for 2014.

My bullish CAPScall on the stock, issued in early 2010, has underperformed the S&P 500 by 56% amid the ongoing carnage in gold stocks at large. I believe the current share price belies the powerful cash flow potential of AuRico's existing asset base and organic growth outlook, and expect AuRico to add long-term shareholder value through continuation of the company's successful acquisitive growth. I see tremendous opportunity for gold investors adding to their quality share positions amid this ongoing correction, but I spy few Foolish bargains more alluring than these AuRico Gold shares beneath $7 per share.

Add AuRico Gold to My Watchlist

Add Endeavour Silver to My Watchlist

Add Timmins Gold to My Watchlist

Add Primero Mining to My Watchlist

The article Why This AuRico Gold Smackdown Is Way Overdone originally appeared on Fool.com.

Fool contributorChristopher Barkercan be foundblogging activelyand acting Foolishly within the CAPS community under the usernameTMFSinchiruna. Hetweets. He owns shares of AuRico Gold, Endeavour Silver, and Primero Mining. The Motley Fool owns shares of Primero Mining. The Motley Fool has adisclosure policy. We Fools may not all hold the same opinions, but we all believe thatconsidering a diverse range of insightsmakes us better investors. Try any of our Foolish newsletter servicesfree for 30 days.

Copyright © 1995 - 2012 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.