What's Next for SUPERVALU

Shares of supermarket chain SUPERVALU (NYS: SVU) are selling for half off after a disastrous quarterly report last week. Earnings per share came in at just half of analyst estimates at $0.19/share, and the company suspended what had been a juicy 7% dividend in order to throw more money at its heavy debt burden. Management also revealed the company was looking into strategic alternatives, aka, a potential buyout, as both revenue and profits were down from a year ago. The company blamed increased competition for the slide in sales, having lowered prices in response to rivals' actions. SUPERVALU also took the ominous action of withdrawing all previous guidance for the fiscal year, including earnings per share and same-store sales.

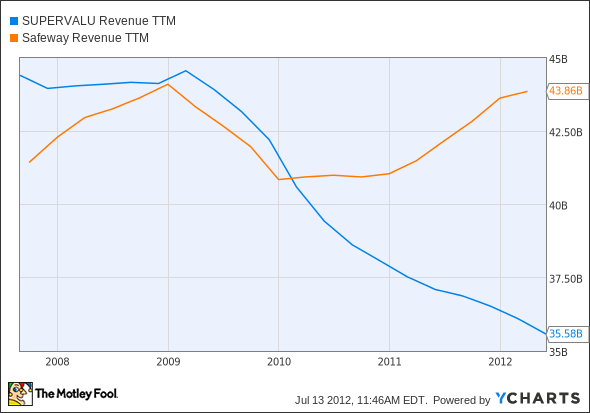

Supermarket sweep

While the market's reaction to the report was probably deserved, especially considering the dividend suspension, what was odd was that SUPERVALU dragged the whole industry down with it. Safeway (NYS: SWY) dropped 12% Thursday while Kroger (NYS: KR) fell 4%. After the SUPERVALU debacle, Safeway looks like a real bargain, trading at prices not seen since the '90s. The chain also offers a 4.4% dividend yield and has not faced the recent struggles plaguing SUPERVALU. The market's making a mistake by lumping all of these stocks together.

SVU Revenue TTM data by YCharts

Since a post-recession dip, these two companies have traveled separate paths. Safeway has steadily grown revenue since 2010 while SUPERVALU can't escape its downward spiral. Analysts also expect Safeway to grow earnings per share by more than 10% this year and another 7% in 2013.

It's not you; it's the industry

As retail giants Wal-Mart (NYS: WMT) and Target have made inroads into food sales, traditional supermarkets have been on the decline over the last decade with their share of U.S. grocery sales dropping from 66% in 2000 to just 51% last year.

Analysts have explained the plight of mid-range supermarkets with the consumer hourglass theory, a trend following the financial crisis that shows consumers have traded up toward luxury brands like Whole Foods or down to discount chains like Family Dollar. Those stocks have thrived over the past few years. Shares of Whole Foods have jumped more than 1,000% since bottoming after the crash, and Family Dollar is up nearly 400% since 2008. Wal-Mart's been no slouch either of late -- shares of the retail behemoth are up about 50% in the last year, soaring in recent months on the strength of an impressive Q1 earnings report. Groceries now account for 55% of the chain's domestic revenue up from 41% in 2008. Even traditional player Kroger had some good news recently, reporting that same-store sales had climbed 4.2% in its most recent quarter.

You might be selling it, but I'm not buying it

In the press release, CEO Craig Herkert blamed the miserable quarter in part on an "increasingly competitive environment," but it's worth noting that SUPERVALU's competitors don't appear to be suffering from the same affliction. While some observers might point to the sluggish economy as impacting the quarter, supermarkets should be well insulated from economic downturn, as they sell necessary goods. If anything, consumers may cut down on restaurant spending and save more of their food budget for the grocery store.

The reality is that bad management is the culprit here. Its 2006 decision to buy the struggling Albertson's chain turned into an albatross, loading the company with more than $8 billion in debt and giving it too many brands to successfully manage. Net income never grew and has struggled to remain in positive territory since the financial crisis. The "strategic alternatives" the company is now seeking may be the best option left.

Foolish takeaway

There's surely value for the right party somewhere here, and at an EPS of $0.19/share last quarter, this would be a good deal for shareholders if management could just hold that line. With about 2,500 locations under its umbrella nationwide, each store is only valued at about $2.6 million based on its current enterprise value of $6.63 billion. I'm betting there would be plenty of interested buyers at those prices seeing as build-outs often cost much more than that.

Sears Holdings (NAS: SHLD) may serve as a model here. The broad-based retailer is as dysfunctional as any in the industry, and its balance sheet is debt-laden in much the same way as SUPERVALU's, but the stock has soared this year as the company has closed underperforming stores and sold off real estate. The market sees this as an asset play.

While there may be headwinds in the industry from the likes of Wal-Mart and others, supermarkets aren't facing any serious threat in the way other retailers are from Amazon.com, and even a giant like Wal-Mart can only gobble up so much market share. Whether it's through a buyout, a management overhaul, or a strategic transformation, SUPERVALU will make some sort of a turnaround. These stores aren't worthless.

While Wal-Mart may be one of the main reasons SUPERVALU's stuck in the mud, our analysts think the world's No. 1 retailer is losing its own battle on another front. A setback for Wal-Mart could be a gain for a SUPERVALU and other traditional supermarkets. Find out how this transformation could impact you in our special free report: "The Death Of Wal-Mart: The Real Cash Kings Changing the Face of Retail." You can get your free copy now. All you have to do is click right here.

The article What's Next for SUPERVALU originally appeared on Fool.com.

Fool contributorJeremy Bowmanholds no positions in the companies in this article. The Motley Fool owns shares of Supervalu. Motley Fool newsletter services have recommended creating a bull call spread position in Wal-Mart Stores. Motley Fool newsletter services have recommended buying calls on Supervalu. The Motley Fool has a disclosure policy.We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. Try any of our Foolish newsletter services free for 30 days.

Copyright © 1995 - 2012 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.