Why Is the Market Ignoring Halliburton in 2012?

The first half of 2012 is in the rearview mirror, and investors are gearing up for what looks to be an action-packed ending. There are bound to be some big winners -- and more than a few duds -- no matter what happens in the United States and abroad.

Will your favorite stock have its victory lap as we hit the home stretch, or will it get passed by? First-half performances can hold some clues, so let's look to the recent past to find out whether Halliburton (NYS: HAL) deserves a place in your portfolio going forward.

First-half recap

Halliburton started the year on a positive note with solid fourth-quarter results and got more good news when BP's (NYS: BP) contentious court battle had a major ruling, absolving the oil services company of greater liability. That high note didn't last long:

HAL Total Return Price data by YCharts

Here are a few financial snapshots of its recent performance:

Statistic | Result |

|---|---|

Market Cap | $26.1 billion |

TTM Revenue | $26.42 billion |

TTM Net Income/Loss | $2.96 billion |

TTM Free Cash Flow | $822 million |

MRQ Revenue | $6.87 billion |

MRQ Net Income/Loss | $627 million |

MRQ Free Cash Flow | ($48 million) |

MRQ Revenue / Net Income Year-Over-Year Change | 30% / 22.7% |

P/E and Forward P/E | 8.4 / 7.3 |

Price to Free Cash Flow | 31.8 |

Motley Fool CAPS Rating (out of 5) | **** |

Source: Morningstar. TTM = trailing 12 months. MRQ = most recent quarter.

What the numbers don't tell you

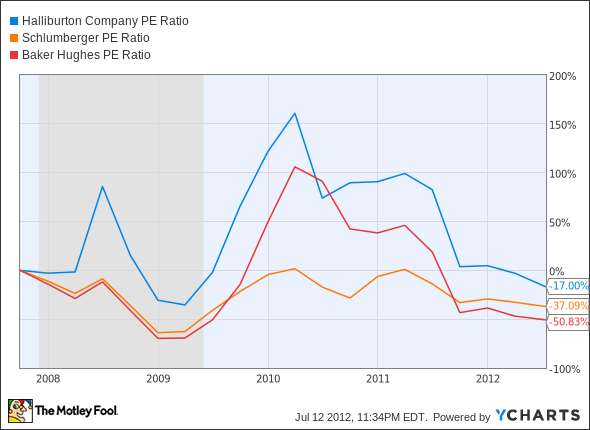

Halliburton, along with drilling-services peers Schlumberger (NYS: SLB) and Baker Hughes (NYS: BHI) , turned in a trifecta of solid first-quarter results this spring. That didn't stop the three companies from descending toward low points in the second quarter. Since the stock-price declines weren't tied to falling profit, it's meant that this trio of companies is trading at its lowest set of valuations in years:

HAL P/E Ratio data by YCharts

Despite all the positive news early this year, Halliburton shareholders have also had some cause for concern. Fool analyst Jason Moser thinks the stock's attractively valued but attributes its share-price slide to market pessimism over a strategic shift.

Crude oil drilling has been on the upswing, but the long nat-gas glut appears to be drawing to a close, as my fellow Fool Travis Hoium pointed out last month. Halliburton's hydraulic fracturing expertise could wind up a liability if nat-gas producers continue to reduce their operations. Chesapeake Energy (NYS: CHK) , which has had plenty of problems of its own, has been key to that strategic shift. The second-biggest nat-gas extractor cut its production early this year.

Halliburton's diversified enough to weather the nat-gas pullback, with IT services and other oilfield support. Since the company's one of the leading developers of nat-gas extraction technology, any inevitable uptick in nat-gas exploration will be a boon to Halliburton's still-growing bottom line. One thing to be wary of, however, is Halliburton's history of market underperformance. Since 1980, Halliburton's shares have returned far less than simply investing in a dividend-paying index fund. Will that trend be turned on its head in the second half of 2012? We'll have to wait and see.

If you're on the hunt for other stable dividend stalwarts, The Motley Fool has just the thing for you. We've put together a free report with nine great dividend-paying stocks for our readers, and it's still available for a limited time. Click here to find out more about the "Nine Rock-Solid Dividend Stocks" that can secure your future.

The article Why Is the Market Ignoring Halliburton in 2012? originally appeared on Fool.com.

Fool contributorAlex Planesholds no financial position in any company mentioned here. Add him onGoogle+or follow him on Twitter,@TMFBiggles, for more news and insights. The Motley Fool owns shares of Chesapeake Energy.Motley Fool newsletter serviceshave recommended buying shares of Halliburton. We Fools don't all hold the same opinions, but we all believe thatconsidering a diverse range of insightsmakes us better investors. Try any of our Foolish newsletter servicesfree for 30 days. The Motley Fool has adisclosure policy.

Copyright © 1995 - 2012 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.