What is Going on With the Middle Class?

The recession reacquainted millions of Americans with the idea of a household budget. That's great news for savers, and horrible news for the luxury goods business. Or that's what we all thought. Things have taken an odd turn recently. It looks like both luxury goods and discounters are now a great place to invest. Let's take a closer look, and figure out what the heck Americans are thinking.

The flagging middle

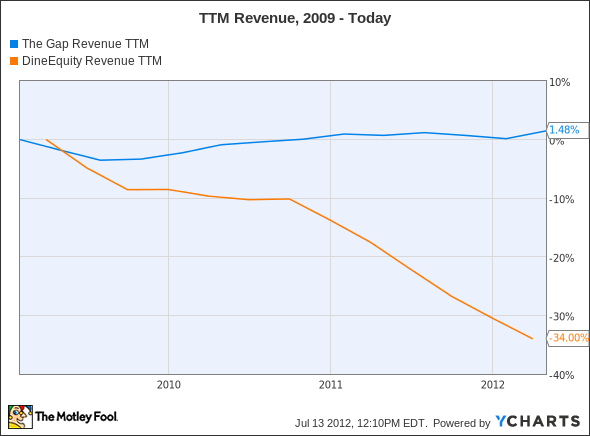

In order to understand what's happening on the fringes of the retail space, let's set the bar for middle-America. There aren't many brands that scream middle-class like Gap (NYS: GPS) , and the DineEquity restaurant brands, including Applebee's. If Americans had merely pulled back on luxury spending, these two should have weathered the storm without too much heartache. As it turns out, there has been plenty of heartache.

As the following chart shows, Gap's revenue has struggled to stay flat since 2009. DineEquity has slipped 34% over the same period. Both brands suffered from a cost-conscious public, and an inability to conform to consumers' new needs for value.

Revenue TTM data by YCharts

If these two are the baseline reading for middle-America, then let's take a look at the outliers' performance -- the high and low brands.

Milk and diamonds

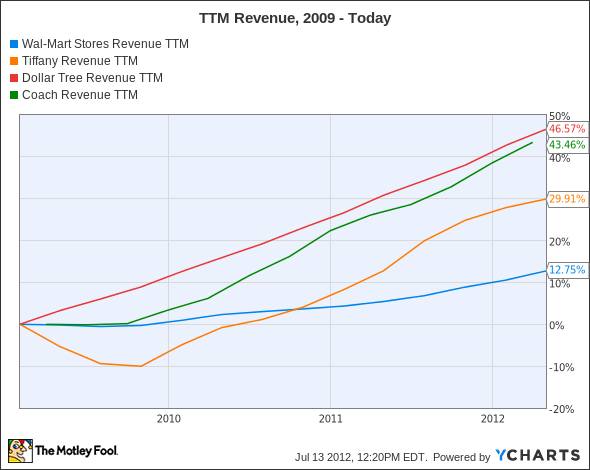

Again, let's look at a couple of clearly-defined brands. Walmart (NYS: WMT) has, since the dawn of time, touted its low prices and accessibility. What's better than cheap? One dollar. Dollar Tree (NYS: DLTR) will act as our second low-end retailer.

On the high end, it doesn't get much pricier than diamonds and designer bags. Tiffany's (NYS: TIF) and Coach (NYS: COH) make for comparable brands. They both operate boutiques, and can be found in larger department stores. Both have made inroads into the middle class recently, but are still considered luxury goods. How have the cheap and expensive fared over the same period?

Revenue TTM data by YCharts

Boom.

Welcome to crazytown

While this might make little sense on the surface, the Wall Street Journal has a theory. The paper calls it a high-low trend, where "[s]hoppers pinch pennies on basics but splurge when they see something they really want." This explains the ground falling out from the middle-class centered brands, and the strength on the high and low ends of the retail spectrum.

The problem with this theory is that it clearly cherry picks. While the charts I presented earlier do reflect what's happening, they don't show the whole story. Lots of other companies are doing well in the middle, and others on the extremes are doing poorly.

I prefer my own explanation -- the sofa-bed theory. We've all sat and slept on sofa-beds, and they're horrific. They are both bad sofas and bad beds. But they try to have it both ways. I think a lot of brands in the middle are trying to have it both ways, to be both expensive and affordable. While on the extremes, companies are realizing that their strengths lie in being really cheap or really expensive.

Dollar Tree saw a 5.6% increase in comparable store sales last quarter. This was slightly higher than the 4.8% that Walmart had over the same period. Both of the retailers have focused on their core strengths in order to drive up sales. As they continue to manage their niches, both of these companies should continue to provide solid revenue growth to investors.

The bottom line

When the economy picks up, the middle class brands may have a resurgence. The Journal might be right about Americans holding off on medium-sized items, and any influx of cash into American wallets could alleviate retailers' problems. However, the sofa-bed theory accounts for more situations. It's another way to phrase the idea of diworsification.

Companies try to do more things than they have the skills to do well. As a result, consumers end up sleeping on lumpy beds, and sitting on couches with bars in them. At some point, people get fed up and just wait until they have enough money to buy the nice new couch. Then they save up for the nice new bed.

I like what Walmart is doing both in the U.S. and abroad -- well, not the bribery thing. International operating income rose 21% last quarter. No one else seems to be breaking into the international markets with the gusto that Walmart is displaying. That it's performed well during the recession is just icing on the cake.

But international sales aren't the only thing that matters. There's huge demand waiting to be unleashed in the U.S., once people are able to get back to some sense of normal. The Fool has a special report explaining why The Future is Made in America. In it, we detail which companies are positioned to change the face of manufacturing in the U..S. You can learn all about it by getting your free copy today.

The article What is Going on With the Middle Class? originally appeared on Fool.com.

Fool contributorAndrew Marderdoes not own any of the stocks covered in this article. The Motley Fool owns shares of Tiffany.Motley Fool newsletter serviceshave recommended buying shares of Coach.Motley Fool newsletter serviceshave recommended creating a bull call spread position in Wal-Mart Stores.Motley Fool newsletter serviceshave recommended shorting Tiffany. The Motley Fool has adisclosure policy. We Fools may not all hold the same opinions, but we all believe thatconsidering a diverse range of insightsmakes us better investors. Try any of our Foolish newsletter servicesfree for 30 days.

Copyright © 1995 - 2012 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.