Is Alpha Natural Resources a Steel of a Deal?

Shares of Alpha Natural Resources (NYS: ANR) hit a 52-week low on Thursday. Let's take a look at how it got there and see if cloudy skies are still in the forecast.

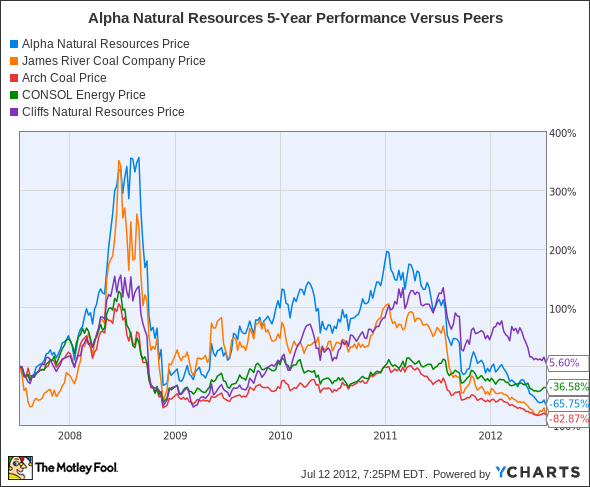

How it got here

We don't have to dig too deeply (pun completely intended) to decipher why Alpha Natural Resources is hitting a new 52-week low -- blame it on coal.

Alpha Natural Resources supplies both steam coal, used by utilities in electrical generation, and metallurgical coal used to strengthen steel. The drop in prices across both sectors has been steep and precipitous with utilities abandoning coal in favor of natural-gas-powered facilities and a general global slowdown hampering steel sales. That is a recipe for disaster for much of the coal sector.

We've begun to see those fears translate into tangible worries as Patriot Coalfiled for bankruptcy protection earlier this week after failing to renegotiate the terms of its loans. James River Coal (Nasdaq; JRCC) also dove in sympathy, as it has $416 million in net debt and large expected quarterly losses to contend with in the near-term.

In response to weakened demand, low coal prices, and growing supply worries, many coal companies have taken to cutting production, closing mines, and even jettisoning coal assets. Alpha Natural reduced the midpoint of its production guidance by 7.5 million tons in the first-quarter. Both Arch Coal (NYS: ACI) and CONSOL Energy (NYS: CNX) have turned to closing mines. CONSOL even went one step further and cut its work schedule to five days a week to save on expenses. Cliffs Natural Resources (NYS: CLF) has actually been selling some of its metallurgical coal assets, agreeing to sell its 45% stake in the Sonoma Coal Mine in Australia for $143 million.

How it stacks up

Let's see how Alpha Natural Resources stacks up next to its peers.

The race to the bottom is on, and outside of Cliffs Natural, whose outstanding dividend has boosted its appeal among investors, it's anyone's game.

Company | Price/Book | Price/Cash Flow | Forward P/E | Debt/Equity |

|---|---|---|---|---|

Alpha Natural Resources | 0.2 | 2.2 | N/M | 40.1% |

James River Coal | 0.2 | 0.5 | N/M | 152.7% |

Arch Coal | 0.4 | 2 | 34.4 | 113.6% |

CONSOL Energy | 1.9 | 5.4 | 11.3 | 84.7% |

Cliffs Natural Resources | 1 | 3.1 | 3.8 | 53.7% |

Sources: Morningstar and Yahoo! Finance. N/M = not meaningful.

If you can stand the risk and don't mind weeding through the coal companies that have very limited access to capital, the coal sector looks like a screaming buy.

In all fairness, most of Cliffs Natural Resources' sales come from its iron ore mining operations; but even so, its dividend growth and yield of 5.5% is impressive -- as is its extremely cheap valuation.

CONSOL and Arch also offer quarterly payments to shareholders, albeit they are heading in separate directions. CONSOL's yield of 1.7% may not be much to look at, but at least it's on the rise. Arch Coal recently slashed its quarterly payout from $0.11 to $0.03 in order to conserve cash.

Alpha Natural is still in the process of realizing its cost synergies from its merger with Massey Energy one year ago. Although it's been a bumpy ride, Alpha is the best-capitalized of the bunch with access to $1.8 billion in cash plus revolving credit.

Finally, James River Coal is a disaster and its valuation reflects this. With few lending prospects available and losses expected over the coming quarters, it may follow Patriot Coal down the path to bankruptcy.

What's next

Now for the $64,000 question: What's next for Alpha Natural Resources? The answer is going to depend on whether coal prices and demand improve on both the thermal and metallurgical ends, and if Alpha Natural is prudent with its spending and production so as not to overextend itself during a very weak period of demand for coal.

Our very own CAPS community gives the company a three-star rating (out of five), with 94.7% of members expecting it to outperform. Although I've yet to make a CAPScall in either direction on Alpha Natural, I'm going to stick with my general bullishness on the long-term outlook of coal and enter a CAPScall of outperform.

The reasoning here is pretty simple: I feel coal is a strong long-term buy! Much of coal's recent declines are because of a warmer-than-normal winter and record-low natural gas prices which caused utilities to switch over to natural gas. As I've proposed before, the weather is hardly a consistent indicator of success (for all we know next winter could be colder than normal), and natural gas prices would rebound -- and they have! As these factors return to more normalized levels, demand for coal will pick up and well-capitalized companies like Alpha Natural, which are now bigger and realizing the cost savings of its Massey Energy merger, will be ready to capitalize!

Even with coal and natural gas prices near their lows, there are always great deals to be had in the energy sector. Our team of analysts at Motley Fool Stock Advisor believes this so much that after poring over the entire energy sector, they've identified the only stock you need to own. Find out its identity by clicking here to get your free copy of this special report.

Craving more input on Alpha Natural Resources? Start by adding it to your free and personalized watchlist. It's a free service from The Motley Fool to keep you up to date on the stocks you care about most.

At the time thisarticle was published Fool contributor Sean Williams has no material interest in any companies mentioned in this article. You can follow him on CAPS under the screen name TMFUltraLong, track every pick he makes under the screen name TrackUltraLong, and check him out on Twitter, where he goes by the handle @TMFUltraLong.Try any of our Foolish newsletter services free for 30 days. We Fools don't all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.

Copyright © 1995 - 2012 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.