1 Great Dividend You Can Buy Right Now

Dividend stocks are everywhere, but many just downright stink. In some cases, the business model is in serious jeopardy, or the dividend itself isn't sustainable. In others, the dividend is so low it's not even worth the paper your dividend check is printed on. A solid dividend strikes the right balance of growth, value, and sustainability.

Today, and one day each week for the rest of the year, we're going to look at one dividend-paying company that you can put in your portfolio for the long term without too much concern. This isn't to say these stocks don't share the same macro risks that other companies have, but they are a step above your common grade of dividend stock. See last week's selection.

This week, I'm going to follow through with my threat to pound the table of retail outperformers and show you why Guess? (NYS: GES) is a dividend payer you can count on.

Anything you can do, it does better

The name may inspire confusion, but after reviewing the various aspects of Guess?' operations, I was left with no opinion other than that this is a remarkably cheap, well-run, shareholder-friendly apparel and accessory manufacturer.

The first thing that stood out to me is just how rapidly Guess? is growing relative to its peers despite the fact that it's possibly the cheapest company in retail, period!

Company | Price / Book | Price / Cash Flow | Forward P/E | 5-Year Revenue CAGR |

|---|---|---|---|---|

Guess? | 2 | 6.8 | 8.1 | 17.8% |

Michael Kors (NYS: KORS) | 16.5 | 64 | 41.9 | 60.1%* |

Fossil (NAS: FOSL) | 3.7 | 18 | 10 | 16.2% |

Abercrombie & Fitch (NYS: ANF) | 1.6 | 9 | 7.9 | 4.6% |

Ralph Lauren (NYS: RL) | 3.5 | 14.8 | 14 | 9.8% |

Sources: Morningstar, author's calculations. CAGR = compound annual growth rate. *2-year annualized growth rate used.

From chic designer brands like Ralph Lauren and Michael Kors to teen hot spot Abercrombie & Fitch, Guess? puts them all to shame. I even included Fossil since Guess? is a direct price-point watch and accessories competitor.

As you can see, Michael Kors (which has a manufacturing deal in place with Fossil) offers the fastest growth rate -- 36.1% same-store sales growth in the U.S. in its latest quarter, to be exact -- but its valuation would send value investors running in the other direction. Abercrombie & Fitch and Fossil offer historically low valuations, but both have suffered from the European spending slowdown. Ralph Lauren presents compelling dividend growth, but has simply come up short to Guess? in terms of sales growth over the past five years.

For Guess?, these metrics speak to its ability to master two key factors: branding and pricing.

Guess?' portfolio of products fit a price point that rarely stretches consumers' wallets, which gives it a nice niche in moderately priced apparel and accessories (not too cheap, not too expensive). Guess? is also able to capitalize on consumers' want for brand-name merchandise. It's true that Guess? is no Louis Vuitton, but it also comes with a considerably smaller price tag. Offering affordable brand-name merchandise is exactly why TJX and Ross Stores have performed so well for so many years and should be a driving force behind Guess?' double-digit growth rate moving forward.

As always, no stock is completely without risks. Just as Fossil and Abercrombie have suffered from a slowdown in Europe, so has Guess?, which saw sales decline 10% in U.S. dollars (unfavorable currency translation accounted for 5% of the decline). However, Guess? is having considerable expansionary success in Germany, China, and Russia and is in a strong enough position to weather this downturn.

Get out your Sharpie -- you're going to need it!

But let's get back to what Guess? does right and why we're looking at this company in the first place: its shareholder-first approach to running its operations.

The first thing I often look for in order to judge whether a company is able to pay a healthy dividend and expand a retail business is strong cash generation and, if possible, a sizable net cash position. Guess? has generated $234 million in net free cash flow over the trailing 12 months and boasts a net cash position of $477 million, or $5.30 per share. Check and check!

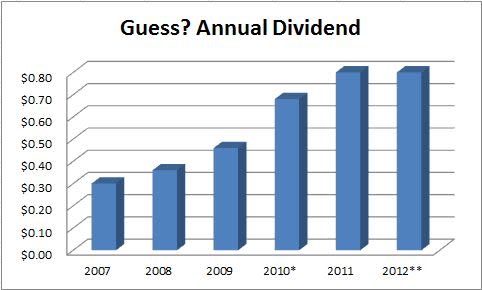

The next thing I often look for is a yield that's not only equal to or higher than the industry average, but one that's growing.

Source: Dividata. *Excludes $2 special dividend. **Assumes quarterly payout of $0.20 for remainder of 2012.

Guess?' current yield of 2.8% crushes many of its peers' (with former great dividend featureAmerican Eagle Outfitters being one of the few exceptions), while its quarterly payout has grown from just $0.06 in early 2007 to $0.20 currently. That equals an annual growth rate of 27.2%. Check and check again!

Finally, I look for alternate examples beyond a dividend that a company actually does care about its shareholders. Guess? provides two.

First, in 2010 Guess? used its sizable cash hoard to pay out a special $2 per-share dividend. Secondly, Guess? has been actively repurchasing its own shares. The company has repurchased 8.2 million shares worth $231 million under its original $250 million repurchase program, and it just approved an additional $500 million repurchase program three weeks ago. More checks!

Foolish roundup

Guess? may have its fair share of growth problems in Europe like many retailers, but it stands head and shoulders above its peers in terms of consistent growth, value, and its shareholder-first ethos. I'm so confident in Guess?' ability to outperform that I'm going to also enter a CAPScall of outperform on the company.

If you're craving even more dividend ideas, I invite you to download a copy of our special report "Secure Your Future With 9 Rock-Solid Dividend Stocks," which is loaded with income-producing companies hand-selected by our top analysts. Best of all, this report is free, so don't miss out!

At the time thisarticle was published Fool contributor Sean Williams has no material interest in any of the companies mentioned in this article. You can follow him on Motley Fool CAPS under the screen name TMFUltraLong, track every pick he makes under the screen name TrackUltraLong, and check him out on Twitter, where he goes by the handle @TMFUltraLong.The Motley Fool owns shares of Guess? and Fossil. Motley Fool newsletter services have recommended buying shares of Guess? and Fossil, writing covered calls on Guess? and, in a separate newsletter service, shorting shares of Fossil. Try any of our Foolish newsletter services free for 30 days. We Fools don't all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy that's always in fashion.

Copyright © 1995 - 2012 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.