Why Incyte Could Be Headed Even Higher

Shares of Incyte (NAS: INCY) hit a 52-week high on Tuesday. Let's take a look at how it got there and see whether clear skies are still in the forecast.

How it got here

To be as cliche as I possibly can: Incyte received approval from the Food and Drug Administration in November for its myelofibrosis drug, Jakafi, and since then, the crowd's gone wild!

With no previous FDA-approved drugs, this was big news for Incyte, a developmental-stage company focused on cancer and inflammation therapies. Although the market for myelofibrosis treatment includes a very small percentage of the population -- about 3,000 new cases each years in the United States -- it should be able to rapidly command the lion's share of the treatment market for moderate and high-risk MF.

Indications from Europe have also been encouraging that an approval there is not far off, which should greatly increase its MF treatment potential. The favorable opinion in Europe already triggered a $40 million milestone payment from Novartis (NYS: NVS) , Incyte's marketing partner, and the company could stand to earn another $60 million milestone payment once approval of Jakafi occurs in certain European nations.

In addition to Jakafi's approval, Incyte has a deep pipeline of drug hopefuls, although many are still in the early phases of clinical trials. Incyte is working with Eli Lilly (NYS: LLY) in advancing its inflammation drug segment with specific therapies targeting rheumatoid arthritis and psoriasis. It also has an ongoing phase 3 trial for polycythemia vera, a rare blood cancer, which has shown promising results.

But, as usual, things are never a cakewalk for clinical-stage companies and there are often plenty of failures to go along with the few successes. Incyte abandoned its study targeting a once-daily oral treatment for HIV/AIDS and also may need to share some of its MF patient pool with YM BioSciences (AMEX: YMI), assuming its own JAK1/JAK2 inhibitor receives FDA approval.

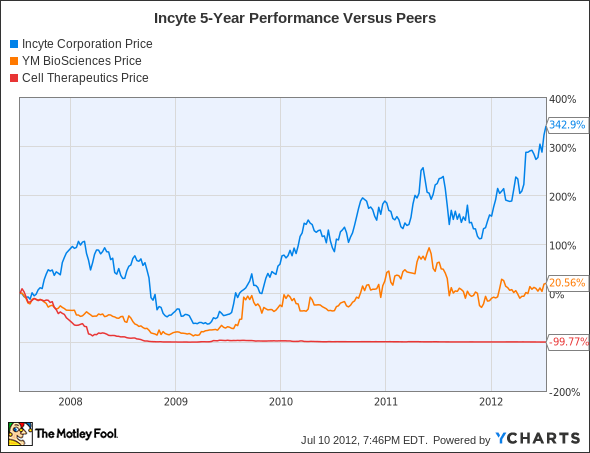

How it stacks up

Let's see how Incyte stacks up next to its peers.

Incyte's successes are very easily demonstrated by its five-year outperformance, while, on the other end of the spectrum, Cell Therapeutics (NAS: CTIC) turns in possibly the worst performance of the period, short of declaring bankruptcy.

I'd normally compare financial metrics here, staying consistent with our theme, but that seems rather pointless with all three companies heavily involved in clinical-stage development.

Cell Therapeutics, well known for its multiple FDA rejections for pixantrone and its heavy dilution of shareholders through secondary offerings, recently purchased an oral JAK2 inhibitor for myelofibrosis from S*BIO that's currently in late-stage trials for $30 million. Although the drug could treat areas of MF that are unmet at the moment, there were enough serious adverse events during earlier trials that, if persistent, could cloud its approval chances. Looks like another dud from Cell Therapeutics, if you ask me.

YM BioSciences' oral MF drug hopeful, CYT387, has shown promise, as my Foolish colleague Rich Duprey noted last month, but it's still far too early to herald it a success. With quite some time left before it would hit the market, the MF space is Incyte's to win or lose.

What's next

Now for the $64,000 question: What's next for Incyte? That's going to depend on whether it priced Jakafi too aggressively (it will cost $85,000 annually), whether it can get physicians to prescribe the drug (which shouldn't be a problem since there are few options available), and whether it draws the attention of a larger pharmaceutical company (ahem, Novartis and Eli Lilly) as a potential buyout candidate if it can get another drug or two approved from its pipeline.

Our very own CAPS community gives the company a two-star rating (out of five), with 86.2% of members who've rated it expecting it to outperform. Count me among the optimists, as I've ridden a CAPScall of outperform on Incyte to a 79-point gain.

You'd think that with such a huge outperformance I'd be ready to cash in my chips -- but that's not the case. With large pharmaceutical partners Novartis and Eli Lilly on its side, Incyte has an experienced marketing team ready for when it does get other drugs in its pipeline approved by the FDA. Incyte's focus on rare diseases is also prudent since it eliminates diving into overcrowded drug markets. True, this does lead to the fear that Incyte could price patients out of using its therapies, but I don't think that will be the norm. Incyte still appears to be a good value to me and I'll be riding this stock higher.

Craving more input on Incyte? Start by adding it to your free and personalized watchlist. It's a free service from The Motley Fool to keep you up to date on the stocks you care about most.

At the time thisarticle was published Fool contributor Sean Williams has no material interest in any companies mentioned in this article. You can follow him on CAPS under the screen name TMFUltraLong, track every pick he makes under the screen name TrackUltraLong, and check him out on Twitter, where he goes by the handle @TMFUltraLong.Try any of our Foolish newsletter services free for 30 days. We Fools don't all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.

Copyright © 1995 - 2012 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.