Is First Niagara Financial Ready to Pour Down Profits?

Shares of First Niagara FinancialGroup (NAS: FNFG) hit a 52-week low on Tuesday. Let's take a look at how it got there and see if cloudy skies are still in the forecast.

How it got here

Biting off more than you can chew is always a fear shareholders have about the companies they invest in. That appears to be the primary factor pulling shares of First Niagara Financial to a new 52-week low.

In 2011, First Niagara agreed to purchase 195 bank branches from HSBC (NYS: HBC) for a sum of $1 billion. To pay for the deal First Niagara shareholders saw a dramatic -- and dilutive -- increase in outstanding shares as the company turned to share issuances to raise financing for the deal. The move was made to broaden its reach and boost its assets in New England, although antitrust regulators mandated the company sell almost 20% (37) of the acquired branches to KeyCorp (NYS: KEY) for $110 million to clear regulatory hurdles. First Niagara also sold additional branches to Community Bank System and Financial Institutions.

Plainly put, the transition hasn't been as smooth as many had anticipated. First Niagara has dealt with customer attrition rates of 2%, which is not bad by most standards, and shareholders were walloped with huge share offerings. First Niagara also chose to lighten its mortgage-backed securities portfolio recently by selling $3.1 billion worth of the securities to pay down debt. The move will be a near-term burden on profitability considering interest rates are at record lows, but it reduces leverage, which will be helpful to the company when interest rates do begin to rise.

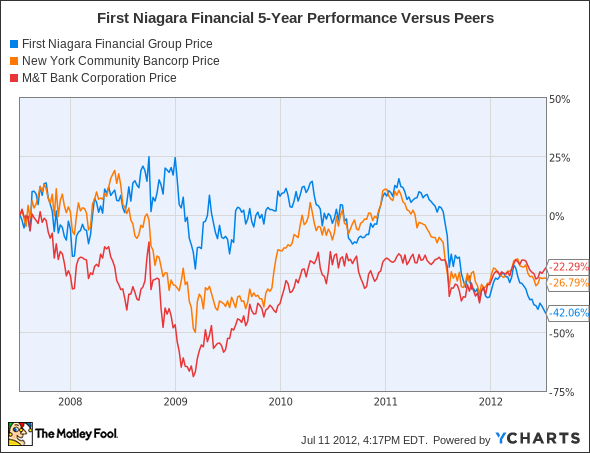

How it stacks up

Let's see how First Niagara stacks up next to its peers.

Few savings and loan banks in the Northeast have been spared over the past five years, with equally bad results from First Niagara, as well as New York Community Bancorp (NYS: NYB) and M&T Bank (NYS: MTB) .

Company | Price/Book | Forward P/E | Dividend Yield |

|---|---|---|---|

First Niagara Financial | 0.6 | 6.6 | 4.3% |

New York Community Bancorp | 1.0 | 10.8 | 8.1% |

M&T Bank | 1.2 | 10.9 | 3.4% |

Source: Morningstar; yields are projected.

While all three S&Ls here present compelling values in their own right, each comes with its own set of risks.

For New York Community Bancorp, the Fool's Matt Koppenheffer recently dissected three reasons investors should consider selling. Particularly compelling is that fact that while many of New York Community's peers have set aside a good chunk of loan loss reserves to cover more than 100% of nonperforming loans, New York Community itself has only set aside enough to cover 26% of non-performing loans (though it's not as bad as it looks since some of those loans are backed by the FDIC). Plain and simple, investors don't like risk, but they do love that 8.1% yield.

M&T Bank's biggest issue has been its lack of adequate liquidity compared with its peers. It commands the highest market capitalization of the three, but its tier 1 common capital ratio is just a hair higher than 7%.

With its asset sales of its newly acquired HSBC banks nearly complete, the risks associated with First Niagara relate mainly to its leverage and near-term reduced earnings potential.

What's next

Now for the $64,000 question: What's next for First Niagara Financial? That's going to depend on whether its increased presence in the Northeast will actually translate into bottom-line results and whether the company can begin another streak of dividend growth after halving its dividend to $0.08 a quarter in 2012.

Our very own CAPS community gives the company a four-star rating (out of five), with 92.1% of members who've rated it expecting it to outperform. Count me among the optimists, as I too made a CAPScall on First Niagara with an outperform rating in April and am currently down 14 points on that call.

In addition to its big increase in assets, I also applaud First Niagara for proactively reducing its leverage now as opposed to running for the exits when everyone else does after 2014. Another factor that can't be overlooked is First Niagara's healthy tier 1 capital ratio, which currently sits at 15.6%. Prior to its HSBC purchase, it had been a dividend superstar, and I feel it could be once again if it continues to conservatively manage its assets.

The banking industry may not be the easiest sector to break down or sort out. Luckily, our analysts at Motley Fool Stock Advisor have done the hard work for you and have used the smartest investors in the world, including Warren Buffett, to determine what companies those individuals are buying. Click here for your access to this free special report and find out what companies the smartest investors are buying.

Craving more input on First Niagara Financial? Start by adding it to your free and personalized watchlist. It's a free service from The Motley Fool to keep you up to date on the stocks you care about most.

At the time thisarticle was published Fool contributorSean Williamshas no material interest in any companies mentioned in this article. You can follow him on CAPS under the screen nameTMFUltraLong, track every pick he makes under the screen nameTrackUltraLong, and check him out on Twitter, where he goes by the handle@TMFUltraLong.The Motley Fool owns shares of KeyCorp. Try any of our Foolish newsletter servicesfree for 30 days. We Fools don't all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has adisclosure policy.

Copyright © 1995 - 2012 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.