How Far Can Electronic Arts Fall?

Shares of Electronic Arts (NAS: EA) hit a 52-week low yesterday. Let's take a look at how the company got there to find out whether cloudy skies remain on the horizon.

How it got here

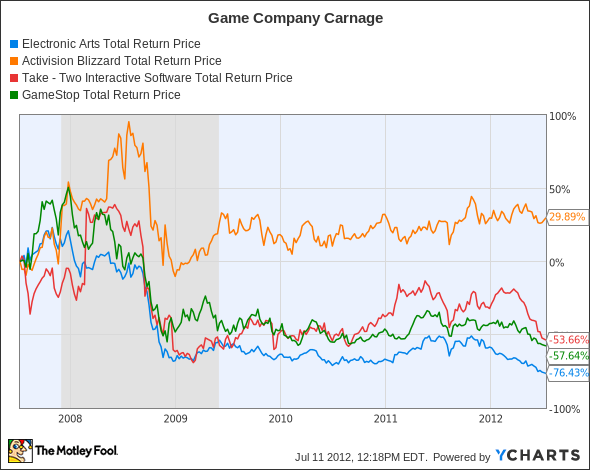

It has not been a good year for publicly traded gaming companies. Take-Two Interactive (NAS: TTWO) is dawdling near its own 52-week lows. Social gaming stalwart Zynga (NAS: ZNGA) has been one of the worst stocks on the market since its late-2011 debut. Even used-game retailer GameStop (NYS: GME) has fallen on its face this year as digital delivery competition heats up.

EA Total Return Price data by YCharts

The lone bright spot (if you can call it that) is Activision Blizzard (NAS: ATVI) , which remains flat for the past year despite record-breaking sales for its decade-in-the-making Diablo III. EA, for its part, hasn't yet reaped the fruits of its would-be World of Warcraft killer Star Wars: The Old Republic. Huge outlays on producing, supporting, and advertising the game returned a profit in the fourth quarter, but it wasn't enough to stem fears of widespread subscriber defections.

What you need to know

Game companies are all over the map numbers-wise. EA sits in the middle of the pack, with a slim net margin and a high P/E. As you'll soon see, that's a rarity for EA, which hasn't seen positive earnings for years.

Company | P/E Ratio | Net Margin (TTM) | Free Cash Flow (TTM) |

|---|---|---|---|

Electronic Arts | 50.5 | 1.8% | $105 million |

Activision Blizzard | 14.3 | 21.6% | $894 million |

Take-Two Interactive | N/M | (13.2%) | ($96 million) |

Zynga | N/M | (40.3%) | $136 million |

GameStop | 7.3 | 3.6% | $450 million |

Source: Morningstar. N/M = not material, negative earnings. TTM = trailing 12 months.

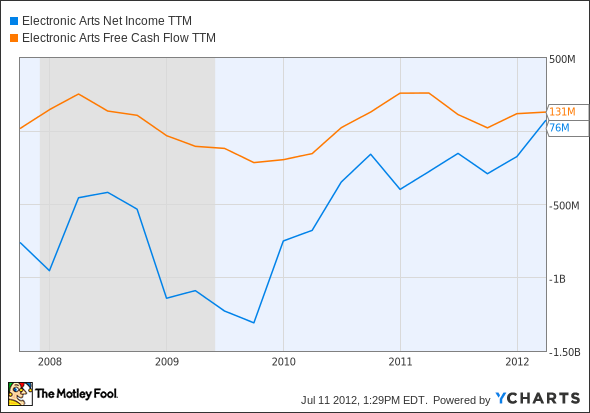

Earnings might be elusive for EA, but it's at least managed to keep its free cash flow above water for nearly two years:

EA Net Income TTM data by YCharts

This discrepancy isn't all that unusual -- Zynga, despite being unprofitable on its income statement, reports solid cash flow. EA's price to free cash flow is slightly better than its P/E, sitting at 35.1 at the moment. That's not all too reassuring for investors threatened not only by possible weakness in the company's flagship MMO, but by the trend toward cheaper, quicker, smaller games spurred by mobile devices. If Activision can't deliver big gains despite breaking sales records every year, what hope does EA really have for long-term outperformance?

Fool tech analyst Eric Bleeker laid out the challenges facing EA and its competitors last month. I've made many of the same points as well, and you can see my rationale against owning EA (or any other game publisher) by clicking this link. My fellow Fool Dan Caplinger has another valuable point to ponder: EA is a very European-focused company, and that reliance is likely to damage its earnings as Europeans keep tightening their belts.

What's next?

Where does EA go from here? That will depend, in large part, on the long-term success of The Old Republic. If subscribers stick around, EA could finally have the stable cash flow needed to push back against Activision's dominance. The company's social push, which now includes top Facebook titles The Sims Social and SimCity Social, has yet to bear profitable fruit, but is also worth watching.

The Motley Fool's CAPS community has given EA a two-star rating. Although 88% of our CAPS players expect the stock to reverse its slide, many are only willing to offer bullish sentiment for the short term, which explains the stock's low rating.

Interested in tracking this stock as it continues on its path? Add EA to your watchlist now for all the news we Fools can find, delivered to your inbox as it happens. Still on the hunt for stocks that can hold up for the long haul? Take a look at The Motley Fool's free report on "3 American Companies Set to Dominate the World." Like EA, they've all got global ambitions -- but unlike EA, they've been long-term profitable, and their growth is just getting started. Click here to get the free information you need for a great buy today.

At the time thisarticle was published Fool contributor Alex Planes holds no financial position in any company mentioned here. Add him on Google+ or follow him on Twitter @TMFBiggles for more news and insights.The Motley Fool owns shares of GameStop and Facebook. The Fool owns shares of and has written calls on Activision Blizzard. Motley Fool newsletter services have recommended buying shares of Take-Two Interactive and Activision Blizzard. Motley Fool newsletter services have recommended writing covered calls on GameStop. Motley Fool newsletter services have recommended creating a synthetic long position in Activision Blizzard. The Motley Fool has a disclosure policy.We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. Try any of our Foolish newsletter services free for 30 days.

Copyright © 1995 - 2012 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.