Analysts Debate: Is Corning a Top Stock?

The Motley Fool has been making successful stock picks for many years, but we don't always agree on what a great stock looks like. That's what makes us "motley," and it's one of our core values. We can disagree respectfully, as we often do. Investors do better when they share their knowledge.

In that spirit, we three Fools have banded together to find the market's best and worst stocks, which we'll rate on The Motley Fool's CAPS system as outperformers or underperformers. We'll be accountable for every pick based on the sum of our knowledge and the balance of our decisions. Today, we'll be discussing Corning (NYS: GLW) , a long-standing glassmaker that supplies many of your favorite electronics manufacturers.

Corning by the numbers

Here's a quick snapshot of the company's most important numbers:

Statistic | Result (TTM or Most Recent Available) |

|---|---|

P/E and Forward P/E | 7.8 /8.2 |

Revenue | $7.89 billion |

Net Income | $2.52 billion |

Free Cash Flow | $1.07 billion |

Capital Expenditures | $2.31 billion |

Market Cap | $18.9 billion |

R&D Ratio | 8.9% |

Worldwide / U.S. Patents and Patents Pending | 12,150 / 4,200 |

Segments and 2011 Revenue Mix | Display Technologies: 40% |

Sources: Morningstar and company press releases. TTM = trailing 12 months.

Alex's take

Is Corning riding a dying trend to its doom, or is it ready to latch on to the mobile revolution for another major growth spurt? On one hand, Corning's flagship Display Technologies segment continues to suffer from declining profit margins, and is now suffering declining revenues, as the entire flat-panel industry dives for the bottom. On the other hand, the company's mobile-focused Specialty Materials segment continues to see strong demand from manufacturers looking for better glass for an ever-growing list of touchscreen devices.

If mobile is Corning's future, it'll have to start picking up some serious slack. The company's display segment hasn't always been its biggest revenue stream:

Sources: Company annual reports.

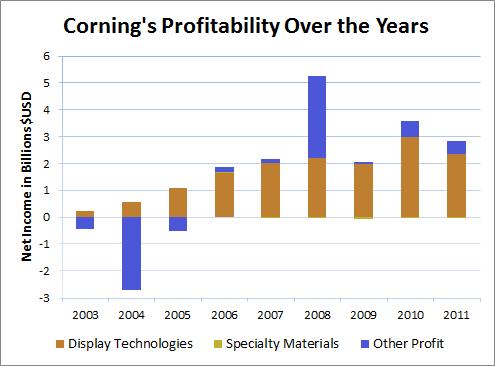

But since its inception, it's contributed the lion's share of Corning's profits:

Sources: Company annual reports.

Notwithstanding big one-time charges in 2004 and 2008, Corning's been so dependent on LCD panel manufacturers for its earnings that it might very well be floundering had the technology not caught on with consumers after the turn of the millennium. Display Technologies net income has always been strong, buoyed in part by additional earnings contributed by Samsung Corning Precision, a joint-owned LCD panel manufacturer.

Contrast that to the Specialty Materials segment, which has yet to significantly impact the bottom line despite rapid sales growth. That segment's first-quarter net margin was 7% -- not a bad haul, but a far cry from Corning's cumulative 24% net margin in the same period. According to Corning, the Specialty Materials segment's stronger net margin was in large part due to a lack of capital costs compared to prior periods. What happens when the company needs to handle greater demand once again? Will that slender profit margin be squeezed to death?

Corning's also moved into manufacturing glass for curved surfaces, which could be a new avenue of growth once Universal Display (NAS: PANL) and Samsung finally start rolling out long-promised bendable devices this year. However, if that high-tech glass is as low-margin as Gorilla Glass has been to date, it's a dangerous move for Corning, especially if bendable TVs start nudging their flat brethren out of the way.

I don't have enough information on Corning's next-gen glass, but at the moment, the company's simply far too dependent on a segment hammered by oversupply and declining profits. If technology takes a future shape that isn't flat, Corning's profits could flatten as well. For the time being, I'll keep my distance.

Sean's take

Talk about a tale of one company on two separate paths.

As Alex has pointed out, 40% of Corning's sales are derived from its LCD glass segment, which has been on a steady decline due to pricing pressure on the TVs that use Corning's glass. Sony's (NYS: SNE) TV division has lost money eight years in a row and contributed to a record-breaking $5.6 billion annual loss. Similarly, Panasonic posted an absurd $10.2 billion annual loss, its earnings dragged down by a 40% drop in plasma sales.

All of this offers little relief for Corning. TV sales should continue to decline thanks to persistent supply gluts. An improvement in mainstream picture quality beyond 1080p could boost sales temporarily, but consumers will be more cautious about stepping up their spending on new TV technologies after 3-D televisions failed to impress.

On the flip side, Corning's other four segments are the bread and butter of where I see strong growth over the next decade.

Its specialty chemicals segment is set to grow by double digits as its nearly scratchproof Gorilla Glass is the dominant choice of smartphone makers. Communications, which makes up about one-quarter of sales, should be a source of stability as small-and-mid-tier telecom companies continue to build out their broadband infrastructure.

Corning's environmental technologies segment, which produces substrates and filters for gasoline- and diesel-powered engines, should also be a source of cash flow stability as vehicle sales continue to rebound. Finally, Corning's life sciences segment could soon provide much higher returns, thanks to its recent purchase of the Biosciences Discovery Labware unit from Becton Dickinson (NYS: BDX) .

The real X factor that helped me make my decision given this bifurcation is Corning's healthy balance sheet. Corning has just shy of $3.7 billion in net cash and has averaged $1.16 billion in free cash flow since 2007. I feel that time frame's a fair gauge, since it encompasses both recessions and expansions. Tack on a 2.3% dividend yield, and you have all the makings of a successful long-term buy.

Travis' take

Before we get into what I think about Corning's business, I think it's worth taking a minute to discuss the company's confusing accounting statements, given the significant investments it's made in joint ventures.

Samsung Corning Precision and Dow Corning (a chemicals-focused partnership with Dow Chemical (NYS: DOW) ) are both major contributors to Corning's earnings, but neither shows its worth in the company's standard income statement or balance sheet. You have to dig down about 120 pages in the 10-K, because both are equity investments of 50% or less, which means that financial statements aren't consolidated. But they do show up on the net income line as a single line item called "equity in earnings of affiliated companies."

When you look at the company's numbers above and see $2.52 billion in net income on $7.89 billion in revenue, it may look like a 32% net margin, but alas, it is not. In 2011, Corning actually generated more than half of its net income from these two equity investments, but we should note that the total earnings from these equity investments fell 25% from the year before. Net sales at the companies were a combined $11.6 billion, so they're actually bigger than Corning itself.

It's also important to note that combined current assets were $9.1 billion, only offset by $1.8 billion in debt. Dow Corning had $2.2 billion in cash and equivalents and all the aforementioned debt. Samsung Corning Precision added another $2.7 billion in cash. These valuable items don't show up on Corning's balance sheet because of the rules of the equity accounting method. They are important to consider, given Corning's $3.7 billion in net cash, if we're looking for sheer value -- something Sean brought up earlier.

Whew! Now that the accounting mumbo jumbo's out of the way, I have space for a few sentences about Corning's actual business.

I am worried about the development of increasingly higher-quality thin films and glass in both the smartphone and television market, which puts continued pressure on margins. As competition evolves and products like glass become more commoditized, I think earnings will likely continue to fall. The increasing size and quantity of televisions that drove growth over the last decade will also die as consumers put less value on incremental improvements, a trend that doesn't bode well for Corning.

But while I think pressure will continue in Corning's main markets, I think the company's ability to evolve and innovate will keep it relevant and profitable. Trading at just 7.8 times trailing earnings and 8.2 times forward earnings -- and considering its strong (if complicated) balance sheet -- Corning is still a good value. The value is strong enough for me to give a green thumbs-up, but I reserve the right to revisit that if earnings continue their rapid decline at Corning's two joint ventures in coming quarters.

The final call

After much debate (and a good deal of education on the arcane financial arrangements behind Corning's balance sheet), we three Fools have grudgingly come to an agreement. By a vote of two to one, we're giving Corning an outperform CAPSCall on our TMF Young Guns CAPS portfolio. We hope this call will bolster our strong performance -- we're beating the market by 53 points over 11 picks since Analysts Debate began earlier this year.

Corning could be the biggest buy you can make for the outside of your smartphone, but it's what's inside that's the real "Trillion-Dollar Revolution." Find out more about The Motley Fool's favorite stock in the mobile hardware war in our exclusive free report -- click here for the information you need for another great buy today.

At the time thisarticle was published Fool contributors Travis Hoium, Alex Planes, and Sean Williams do not have positions in any companies mentioned. You can follow Travis on Twitter at @FlushDrawFool, Sean at @TMFUltraLong, and Alex at @TMFBiggles.The Motley Fool owns shares of Universal Display and Corning. The Motley Fool has sold shares of Sony short. Motley Fool newsletter services have recommended buying shares of Corning, Becton Dickinson, and Universal Display. The Motley Fool has a disclosure policy. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. Try any of our Foolish newsletter services free for 30 days.

Copyright © 1995 - 2012 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.