Is Apple Going to Miss Earnings Again?

Mark your calendars: Apple (NAS: AAPL) reports fiscal third-quarter earnings on July 24. Leading up to the release, analysts are already chiming in with what to expect, and interestingly some think a miss might be in store.

Contestant No. 1

Last week, Wedge Partners analyst Brian Blair said the iPhone maker might not hit the Street's iPhone estimates. In the first two quarters of its fiscal year, Apple put up mind-boggling unit sales of 37 million and 35 million iPhones. That's just over 72 million iPhones in the first half of the year, almost matching the 72.3 million units sold throughout all of the prior year.

Blair thinks iPhone unit sales may have ticked down to between 28 million and 30 million units, which could miss if estimates end up north of 31 million units. Keep in mind that analysts constantly tweak their estimates for Apple, so the consensus is always a moving target. Blair also expects the fiscal fourth quarter, ending in September, to see a significant drop-off as it did last year, when Apple missed, because consumers are now well attuned to Apple's annual upgrade cadence. Even if this happens, he thinks Apple will bounce back with monster iPhone sales of 45 million to 50 million in the December quarter.

Contestant No. 2

Topeka Capital Market's Brian White, who seems dead-set on having the highest Street price target on Apple, notes that sales activity among a handful of component suppliers that he tracks is below historical norms, implying potential iPhone weakness. This basket, which he's dubbed the "Apple Monitor," thanks Apple for between 50% and 60% of sales.

Sales fell 13% sequentially among these companies, when they're normally about flat. White acknowledges that this could easily be weakness in other sectors, particularly as there's been pessimism over broader IT spending.

Contestant No. 3

BMO Capital Markets analyst Keith Bachman thinks the next two quarters will be "challenging" as we approach this year's iPhone introduction, although he did increase his price target by a whole $5, from $695 to $700. His model clearly now predicts that Apple should be worth a whopping 0.7% more than previously thought -- an entire Lincoln more! Apple shareholders rejoice!

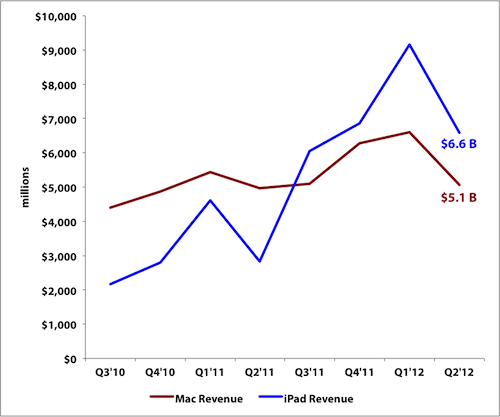

When looking a little further out, though, Bachman is raising his estimates over the next six quarters, which will factor in the next iPhone launch. He also sees iPad sales eating into Mac sales as expected cannibalization sets in, reducing his Mac estimates over that time frame by 40%.

Source: Earnings press releases.

I wouldn't be too worried, though, since the iPad is already a bigger business than the Mac and has been for the past four quarters, and they carry rather enviable margins.

Contestant No. 4

Barclays Capital's Ben Reitzes isn't scared. He thinks some of these fears are "overblown" but still thinks a miss may be possible. Even if Apple doesn't meet expectations, however, he doesn't consider it a concern and thinks investors are looking for iPhone sales in the 27 million ballpark. Reitzes also pegs iPad sales around 14.2 million, but the number could be boosted even higher because of the reduced price of the iPad 2s that are selling into educational institutions.

Street analysts are notorious for having no idea how to forecast Apple's sales. Some of this pessimism is even weighing on suppliers, like Cirrus Logic (NAS: CRUS) , which was down as much as 10% today on no specific news relating to itself. Since the company relies so heavily on iDevice sales for its audio codec revenue, a little bit of iPessimism goes a long way with bringing it down.

Any way you slice it, even if Apple sells 27 million iPhones, which would be on the low end of estimates, that's still 35% growth from last year and more than $17.5 billion in revenue. Hard to call that a miss.

Apple has plenty of room to run, and this new report outlines all the reasons why. Grab yourself a copy to see what our own top tech analyst has to say about the Mac maker's prospects.

At the time thisarticle was published Fool contributorEvan Niuowns shares of Apple, but he holds no other position in any company mentioned. Check out hisholdings and a short bio. The Motley Fool owns shares of Cirrus Logic and Apple.Motley Fool newsletter serviceshave recommended buying shares of Apple and creating a bull call spread position in Apple. We Fools don't all hold the same opinions, but we all believe thatconsidering a diverse range of insightsmakes us better investors. Try any of our Foolish newsletter servicesfree for 30 days. The Motley Fool has adisclosure policy.

Copyright © 1995 - 2012 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.