Is It Time to Get Fired Up About Walter Energy?

Shares of Walter Energy (NYS: WLT) hit a 52-week low on Friday. Let's take a look at how it got there and see if cloudy skies are still in the forecast.

How it got here

One word can quickly summarize why Walter Energy is down in the dumps: coal.

Coal prices are weak across the board, from energy generation to metallurgical coking coal that is used to strengthen steel, and it's having a ripple effect throughout the country. Railroads are transporting less coal and electric utilities can't move quickly enough to retire coal-powered electric plants and convert them to run on cheap natural gas or other renewable fuels.

Walter's problems originate on the coking coal side of the business, where roughly 80% of its business is devoted to the steel-strengthening component. With its purchase of Western Coal last year, Walter broadened its international reach into Europe -- a move likely to have shareholders banging their heads against the wall in disgust at the moment. Long-term coking coal prices should recover, but near-term prices are in free-fall while operating expenses are rapidly rising - not a good combination.

Also dragging Walter down was news Friday that not only had Standard & Poor's downgraded its outlook to negative from stable, but a strike at BHP Billiton (NYS: BHP) between it and labor unions appears to be near an end. The strike had reduced overall metallurgical coal output and buoyed prices, but those prices once again are in jeopardy with production inevitably coming back on line.

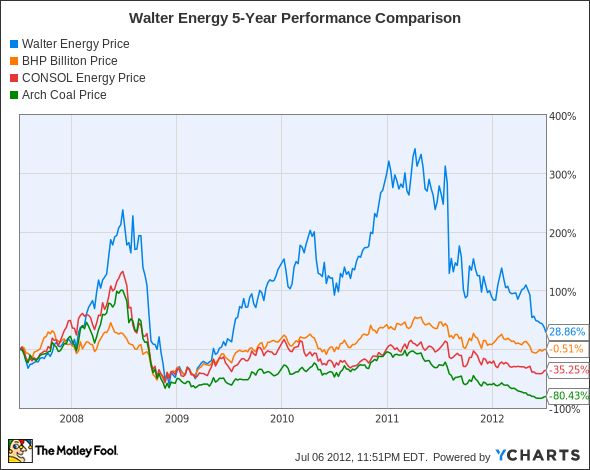

How it stacks up

Let's see how Walter Energy compares to its peers.

Despite hitting a new 52-week low, Walter's shareholders have little to complain about, as it's vastly outperformed CONSOL Energy (NYS: CNX) and the struggling Arch Coal (NYS: ACI) .

Company | Price/Book | Price/Cash Flow | Forward P/E | Debt/Equity |

|---|---|---|---|---|

Walter Energy | 1.1 | 4.0 | 5.1 | 109.8% |

BHP Billiton | 2.7 | 5.7 | 13.8 | 38.8% |

CONSOL Energy | 1.9 | 5.4 | 11.3 | 84.7% |

Arch Coal | 0.4 | 2.3 | 39.8 | 113.6% |

Sources: Morningstar and Yahoo! Finance.

The first thing you'll notice is that metallurgical coal producers are pretty cheap based on these metrics, but we have to also consider that earnings estimates have been falling rapidly. Arch Coal was valued at a single-digit forward P/E just a few months ago -- now it may not even remain profitable in 2013. CONSOL is now trading below two times book value, but it has turned to closing mines and reducing total work days to five in order to cut costs and control production. BHP Billiton gets a pass here, as its mineral mining operations are so diversified it can weather the downturn in metallurgical coal demand.

Debt is another key factor that investors are keeping an eye on. Patriot Coal (NYS: PCX) is teetering on the brink as it attempts to renegotiate its loan terms with its cash dwindling, more losses likely on the way, and one of its customers potentially defaulting on a contract. Arch Coal and Walter are the two companies on this list that could be raising a red flag. Arch's dwindling earnings raise the immediate concern, but Walter Energy has also missed Wall Street's estimates in three of the past four quarters.

What's next

Now for the $64,000 question: What's next for Walter Energy? The answer largely depends on how rapidly demand for steel improves in international markets and if Walter can weather the downturn given its hefty $2.3 billion in debt.

Our very own CAPS community gives the company a four-star rating (out of five), with a whopping 94.9% of members expecting it to outperform. I've yet to personally make a CAPScall on Walter Energy and I'm not quite ready to do so now, either.

Walter has a lot going for it in terms of growing its international presence and staying profitable thus far in a very weak coal environment. However, I can't overlook the great likelihood that Walter's earnings estimates are going to continue to fall as EU countries cut back on spending as austerity packages are enforced. The long-term demand for metallurgical coal should remain strong and pricing power will eventually return, but in the meantime, I'm going to keep my distance.

Even with coal and natural gas prices near their lows, there are always great deals to be had in the energy sector. Our team of analysts at Motley Fool Stock Advisor believes this so much that after poring over the entire energy sector, they've identified the only stock you need to own. Find out its identity by clicking here to get your free copy of this special report.

Craving more input on Walter Energy? Start by adding it to your free and personalized watchlist. It's a free service from The Motley Fool to keep you up to date on the stocks you care about most.

At the time thisarticle was published Fool contributor Sean Williams has no material interest in any companies mentioned in this article. You can follow him on CAPS under the screen name TMFUltraLong, track every pick he makes under the screen name TrackUltraLong, and check him out on Twitter, where he goes by the handle @TMFUltraLong.Motley Fool newsletter services have recommended buying shares of Walter Energy. Try any of our Foolish newsletter services free for 30 days. We Fools don't all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.

Copyright © 1995 - 2012 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.