Why Has Corning Gotten Smudged This Year?

The first half of 2012 is in the rearview mirror, and investors are gearing up for what looks to be an action-packed ending. There are bound to be some big winners -- and more than a few duds -- no matter what happens in the United States and abroad.

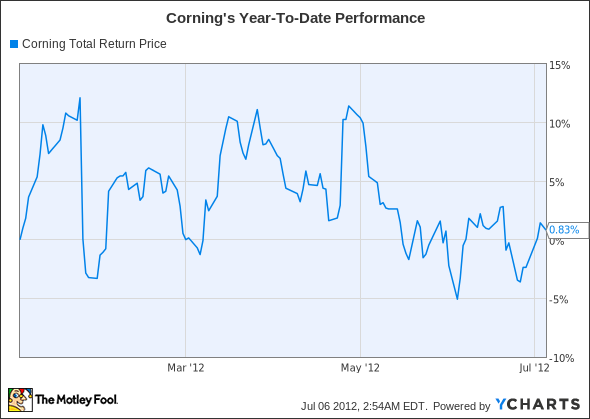

Will your favorite stock have its victory lap as we hit the home stretch, or will it get lapped? First-half performances can hold some clues, so let's look to the recent past to find out whether Corning (NYS: GLW) deserves a place in your portfolio going forward.

First-half recap

Corning has barely done anything in 2012, as you can see here:

GLW Total Return Price data by YCharts

Here are a few financial snapshots of its recent performance:

Market Cap | $19.6 billion |

Trailing-12-Month Revenue | $7.89 billion |

TTM Net Income | $2.52 billion |

TTM Free Cash Flow | $1.07 billion |

Most Recent Quarterly Revenue | $1.92 billion |

MRQ Net Income | $462 million |

MRQ Free Cash Flow | $350 million |

MRQ Revenue / Net Income YOY Change | (0.2%) / (38.2%) |

P/E and Forward P/E | 8.1 / 7.7 |

Price to Free Cash Flow | 18.3 |

Motley Fool CAPS Rating (out of 5) | ***** ( find out more by clicking here ) |

Source: Morningstar.

What the numbers don't tell you

The biggest red flag in Corning's most recent report was its big backslide on the bottom line. The company's LCD panel segment, by far its most profitable, has been suffering in the midst of a larger industry downturn. Should demand perk up again, Corning might not benefit enough to turn things around, as the TV industry (a major driver of LCD prices) has been circling the drain for years.

On the other hand, the company has been riding the mobile megatrend with its Gorilla Glass, which has found homes in over half a billion mobile devices around the world. Apple (NAS: AAPL) got that party started when Steve Jobs sought out a scratchproof front face for the first iPhone. Since then, most of Apple's mobile rivals have adopted the tough glass for their own devices. Microsoft (NAS: MSFT) made Gorilla Glass 2 the preferred surface of its new Surface tablet, and Google (NAS: GOOG) acquisition Motorola Mobility makes extensive use of Gorilla Glass throughout its mobile product line.

The market's been waiting for signs of improved profitability from Corning's specialty materials segment, which makes Gorilla Glass and its descendants, to approach its display technologies (LCD segment) profits. That's contributed to the stock's anemic performance, since many investors have been worried that the company has no cash cow to replace declining LCD panel profitability.

High levels of capital spending have also kept free cash flow depressed, leading to the discrepancy between Corning's P/E and its P/FCF ratios. Once that's fixed, the company's price may very well rise significantly.

Key second-half drivers are likely to remain centered on either a slightly implausible resurgence in Corning's display technologies segment, or the appearance of greater specialty materials profitability. I'd keep my eyes on the company's new Willow Glass, a bendable glass surface that makes Corning an ideal supplier for Samsung and Universal Display (NAS: PANL) , the duo behind an upcoming line of flexible OLED displays. Samsung plans to mass-produce the displays in the latter half of this year, but doesn't expect them to conquer the current-gen LCD displays of mobile devices until 2015.

You might have found the right stock to protect the outside of the mobile revolution, but do you know which company's best-positioned on the inside? The Motley Fool does, and we've got an exclusive free report on that company's prospects. It's got so much potential we've named it the key stock of the next trillion dollar revolution. Don't miss out -- claim your copy of this important report now.

At the time thisarticle was published Fool contributor Alex Planes holds no financial position in any company mentioned here. Add him on Google+ or follow him on Twitter @TMFBiggles for more news and insights.The Motley Fool owns shares of Universal Display, Microsoft, Corning, Google, and Apple. Motley Fool newsletter services have recommended buying shares of Google, Microsoft, Apple, Universal Display, and Corning. Motley Fool newsletter services have recommended creating bull call spread positions in Apple and Microsoft. The Motley Fool has a disclosure policy.We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. Try any of our Foolish newsletter services free for 30 days.

Copyright © 1995 - 2012 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.