Why Pitney Bowes Hasn't Delivered in 2012

As we've hit the halfway point for 2012, now's a good time to look back at what's happening with the stocks that interest you. By making sure you know the important things that a company accomplished -- as well as the setbacks it experienced -- you can make a better decision about whether it's a smart investment for your portfolio.

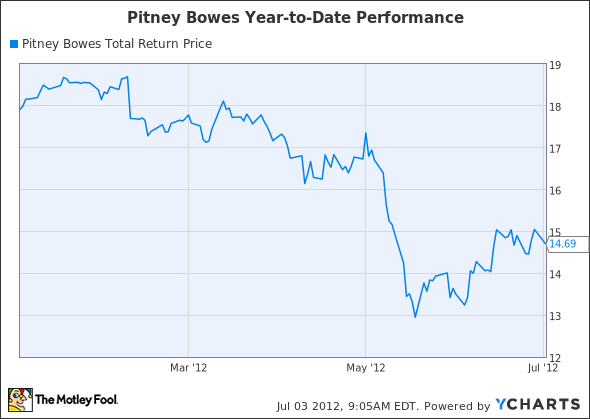

Today, let's take a look at Pitney Bowes (NYS: PBI) . The company best known for its postage machines has struggled to adapt to weakness in mail delivery and the rise of electronic and digital communications. But what's attracted attention lately has been its massive dividend yield. Let's take a quick look at how the stock is doing so far this year.

PBI Total Return Price data by YCharts

Stats on Pitney Bowes

2012 YTD Return | (17.2%) |

Market capitalization | $2.94 billion |

Revenue, Most Recent Quarter | $1.26 billion |

Year-Over-Year Revenue Growth, Most Recent Quarter | (5.1%) |

Net Income, Most Recent Quarter | $159 million |

Year-Over-Year Net Income Growth, Most Recent Quarter | 83.9% |

Trailing Dividend Yield | 10.2% |

CAPS Rating (out of 5) | *** |

Sources: S&P Capital IQ, company reports.

Why has Pitney Bowes been stamped "Return to sender" in 2012?

Pitney Bowes is a good example of what happens when technology brings big changes to an industry. The company was once the dominant player in equipment that facilitated corporate mailings, a staple that every successful business had to have. But the Internet revolution changed everything for Pitney Bowes, as traditional mail volumes have plunged, sending the Postal Service to the brink of insolvency and spelling big trouble for those businesses that rely on the mail for their livelihood.

In particular, Pitney Bowes has missed out on some opportunities. It ceded much of the digital postage market to Stamps.com (NAS: STMP) despite the market's being a natural extension of Pitney Bowes' business.

Pitney Bowes isn't going down with a fight, though. It secured deals with FedEx (NYS: FDX) and United Parcel Service (NYS: UPS) to try to cash in on the delivery volume that has resulted from Internet retail. It also took steps to put its intellectual property to better use by making an agreement with Facebook (NAS: FB) to use Pitney Bowes software for geocoding.

That last point emphasizes something many people don't know about Pitney Bowes: It has a diverse set of businesses under its roof. The key question, though, is whether those businesses will be successful enough to maintain a double-digit dividend that at present takes up nearly all of its income.

Pitney Bowes is value-priced and has plenty of potential reward to go with the risk it brings to the table. If you'd rather look at prospects that aren't quite as aggressive, let me invite you to learn about three smart long-term stock plays in the Fool's latest special report. It's yours for the taking and is absolutely free, but don't miss out -- click here and read it today.

Click hereto add Pitney Bowes to My Watchlist, which can find all of our Foolish analysis on it and all your other stocks.

At the time thisarticle was published Fool contributor Dan Caplinger doesn't own shares of the companies mentioned. The Motley Fool owns shares of Facebook. Motley Fool newsletter services have recommended buying shares of FedEx. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Fool has a disclosure policy.

Copyright © 1995 - 2012 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.