Will Standard Pacific Keep Building on Its Recent Success?

Shares of Standard Pacific (NYS: SPF) hit a 52-week high on Wednesday. Let's take a look at how it got there and see if clear skies are still in the forecast.

How it got here

Despite being a homebuilder concentrated in the absolute worst states for housing -- California, Florida, Nevada, and Arizona -- Standard Pacific managed to stave off bankruptcy during the height of the credit crisis and has been profitable in two straight quarters.

The keys to Standard Pacific's rapid rebound are its land purchases made during the recession, which it garnered for a fraction of what it had been paying years earlier, and historically low lending rates, which have allowed homebuyers to buy homes in most cities at levels that make it actually cheaper to buy than rent. We've seen the strength of these moves translated into Standard Pacific's bottom line. In the first quarter, new orders rose 43% while Standard Pacific's backlog catapulted 55%. Most important, the company's gross housing margin continued to improve and now sits at 20.3%. While not as high as the 22.5% gross housing margin Lennar (NYS: LEN) reported yesterday, it remains one of the few homebuilders sporting a gross housing margin north of 20%.

The housing sector, including Standard Pacific, isn't out of the woods, however. A large influx of foreclosed homes and homes that are delinquent but not yet included in foreclosed housing figures are lining up to hit the market over the next two years. These homes will add to already depressed home prices and could damage what little pricing power homebuilders have. If you recall, KB Home (NYS: KBH) tried, unsuccessfully, to raise home prices last quarter.

Also, as my Foolish colleague Dan Caplinger pointed out, low interest rates also have a catch-22 effect on housing. While they do spur lending activity, the fact that the Federal Reserve insists on keeping rates low throughout 2014 gives potential homebuyers little reason to rush into their purchase, and many are simply waiting for home prices to drop further.

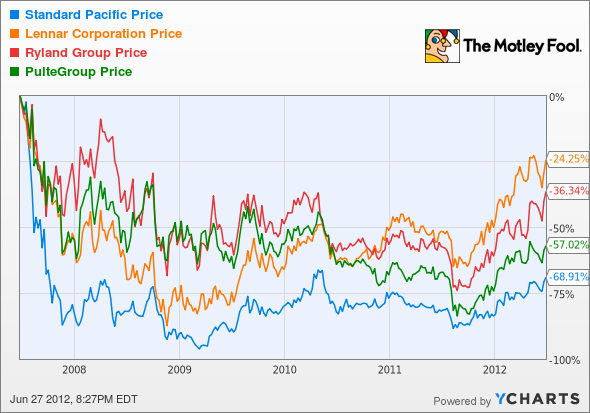

How it stacks up

Let's see how Standard Pacific stacks up next to its peers.

Consider this a five-year period worth forgetting for the homebuilding sector.

Company | Price/Book | Price/Cash Flow | Forward P/E | Gross Housing Margin (MRQ) |

|---|---|---|---|---|

Standard Pacific | 1.9 | NM | 24.8 | 20.3% |

Lennar | 2.1 | NM | 23 | 22.5% |

Ryland Group (NYS: RYL) | 2.5 | NM | 17.2 | 18.4% |

PulteGroup (NYS: PHM) | 2 | 21 | 25 | 18.7% |

Sources: Morningstar, company press releases. NM = not meaningful. MRQ = most recent quarter.

Lennar is, without question, the leader of this group. It maintains a small dividend, the best housing margin (meaning it makes the most out of each dollar), can control its costs, and just reported a ridiculous 61% increase in its backlog yesterday. As for the rest of the group, it's sort of a race to see who can be the best of the worst.

PulteGroup is a company I've derided in recent months for its complete lack of pricing power. Its April-ended quarter did demonstrate the first home sales price increase in some time, but the losses continued to stream in. Pulte hasn't been profitable since 2006, while shareholders have witnessed the outstanding share count rise by 50%.

Ryland isn't much better. It too reported a strong increase in new orders and backlogs, but, like PulteGroup, also recorded a loss. Having not turned an annual profit since 2006, Ryland gets a slight nod over Pulte for not diluting shareholders; however, it gets no reprieve for the fact that its cash pile is still shrinking.

Finally, Standard Pacific has minimized the magnitude of its losses in recent years, but it diluted shareholders to death with secondary offerings during the recession to stay afloat.

What's next

Now for the $64,000 question: What's next for Standard Pacific? That largely depends on whether low lending rates spur buying, whether home prices stabilize, and whether the U.S. job market improves. Right now anything that's "less bad" is considered a godsend in this sector.

Our very own CAPS community gives the company a two-star rating (out of five), with just 58.8% of the members who've rated it expecting it to outperform. Although I've yet to make an official CAPScall, I'm ready to start Standard Pacific with a rating of underperform.

My reasoning here is pretty simple and follows much of the same thesis I have for the homebuilding sector: that home prices will head lower. There are simply too many foreclosed homes ready to hit the market for us to think that future home prices won't be affected negatively. Also, Standard Pacific's $1.38 billion in debt is a burden that I still feel is too difficult to overcome. In its latest quarter, interest payments increased $17 million year over year while cash inflows from operating activities were just $23.6 million. That's like throwing small rocks at a T. rex. I expect this and much of the homebuilding sector to underperform moving forward.

Whether or not the homebuilding sector is right for you, there's plenty of value to be found in our latest special report that lists three stocks that could help you retire rich. See which companies our analysts fancy by clicking here to be magically whisked away to a not-so-fantasy land where you can get this report for free!

Craving more input on Standard Pacific? Start by adding it to your free and personalized watchlist. It's a free service from The Motley Fool to keep you up to date on the stocks you care about most.

The article Will Standard Pacific Keep Building on Its Recent Success? originally appeared on Fool.com.

Fool contributor Sean Williams has no material interest in any companies mentioned in this article. You can follow him on CAPS under the screen name TMFUltraLong, track every pick he makes under the screen name TrackUltraLong, and check him out on Twitter, where he goes by the handle @TMFUltraLong.Motley Fool newsletter services have recommended writing naked calls on Standard Pacific. Try any of our Foolish newsletter services free for 30 days. We Fools don't all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.

Copyright © 1995 - 2012 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.