Why Hewlett-Packard Could Go Lower

Shares of Hewlett-Packard (NYS: HPQ) hit a 52-week low Tuesday. Let's look at how it got here and see whether dark clouds lie ahead.

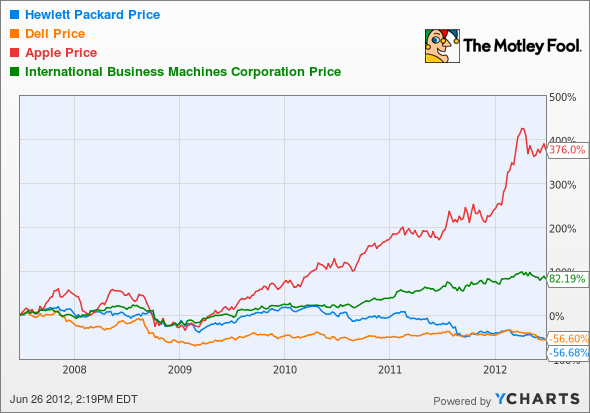

How it got here

Just over a month ago, the iconic PC maker found itself at a 52-week low, yet here we are again today at fresh lows, as shares continue to push lower. There are few, if any, positive catalysts on the horizon.

The past few years have been brutal for HP, with little to no strategic direction amid a revolving door in the CEO office, each with a radically different vision of HP's future. Thus far, HP has mostly missed out on the massive shift toward smartphones and tablets, assuming you don't include the short-lived TouchPad and Veer.

HP is reformulating its tablet strategy and should be among the launch partners for Microsoft's (NAS: MSFT) Windows 8 later this year, but therein lies the rub. The software giant gave us a glimpse of a world with Microsoft-made devices when it unveiled its Surface tablet last week. In the most extreme case, that's a world with a shrinking place at the table for hardware OEMs like HP, and Microsoft's entry into first-party hardware is a direct shot at hardware partners in more ways than one.

Microsoft must price the Surface aggressively if it hopes to compete with Apple's (NAS: AAPL) iPad in any meaningful way, yet doing so undercuts the very hardware partners it relies on, including HP, constraining their already razor-thin margins. Mr. Softy's move also signals that it thinks it needs to take the job into its own hands, expressing a lack of confidence that OEMs can do it properly.

With one of HP's oldest partners now turning into a competitor, HP shareholders have a lot to be worried about.

How it stacks up

Let's see how HP stacks up with some of its competitors and peers.

We'll include some other fundamentals for deeper comparisons.

Company | P/E (TTM) | Sales Growth (MRQ) | Net Margin (TTM) | ROE (TTM) |

|---|---|---|---|---|

Hewlett-Packard | 7.6 | (3%) | 4.2% | 12.6% |

Dell (NAS: DELL) | 6.8 | (4%) | 5.2% | 35.9% |

Apple | 13.9 | 58.9% | 27.1% | 47.1% |

IBM (NYS: IBM) | 14.4 | 0.3% | 15% | 74% |

Source: Reuters. TTM = trailing 12 months. MRQ = most recent quarter.

The commoditized PC hardware business ain't what it used to be. Looking at IBM's profitability and return on equity, it's easy to see why ex-CEO Leo Apotheker wanted oh-so-badly to spin off its PC business and become the next IBM. Then again, Dell is also putting together a Big Blue puzzle with various acquisitions in recent times. The life of a direct Apple competitor is brutal.

What's next?

I think HP will continue to underperform the market, so I'm also going to give it an underperform CAPScall today because of its lack of a cohesive strategy. Its core hardware business is lackluster, flat last quarter, while overall revenue shrank slightly. On top of that, it has little hope of tapping into the massive growth in smartphones and tablets.

Instead, here's a company that's very much tapping into smartphone and tablet growth, powering the next generation of mobile devices from the inside. Grab a free copy of this report to learn more.

The article Why Hewlett-Packard Could Go Lower originally appeared on Fool.com.

Fool contributorEvan Niuowns shares of Apple, but he holds no other position in any company mentioned. Check out hisholdings and a short bio. The Motley Fool owns shares of Microsoft, Apple, and IBM.Motley Fool newsletter serviceshave recommended buying shares of Apple and Microsoft, creating bull call spread positions in Apple and Microsoft, creating a synthetic long position in IBM. The Motley Fool has adisclosure policy. We Fools don't all hold the same opinions, but we all believe thatconsidering a diverse range of insightsmakes us better investors. Try any of our Foolish newsletter servicesfree for 30 days.

Copyright © 1995 - 2012 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.