Are Baker Hughes' Fortunes About to Turn?

Shares of Baker Hughes (NYS: BHI) hit a 52-week low on Monday. Let's take a look at how it got there and see whether cloudy skies are still in the forecast.

How it got here

Baker Hughes provides such a wide array of services to the oil and natural gas industry that it'd be an article in and of itself to describe what it does. In short, Baker Hughes' drilling and fluid-based products are what allow drillers to get oil and natural gas out of the ground.

As you can expect, oil services companies haven't fared very well with the news that many exploration and production companies are cutting back on spending, specifically tied to high supply and near-record-low natural gas prices. Earlier in the month Chesapeake Energy (NYS: CHK) announced plans to cut $3 billion out of its capital expenditures budget over the next three years, while Canada's largest natural gas producer, Encana (NYS: ECA) , not only reduced spending, but has also jettisoned some of its natural gas interests in British Columbia.

Baker Hughes' earnings have recently felt the pangs of this slowdown in terms of reduced pricing power in its pressure pumping product line and through higher expenses to necessitate a product changeover to a more oil-centric-drilling view.

Not everything has been bad news, however. According to Baker Hughes in its latest weekly rig count, there were 1,966 active rigs as of last week whereas there were only 1,882 active rigs last year. Even with the spending cuts, rigs and the need for products and maintenance is up overall. It's still worth noting, though, that oil-drilling rigs outnumber natural gas rigs by a count of almost three-to-one.

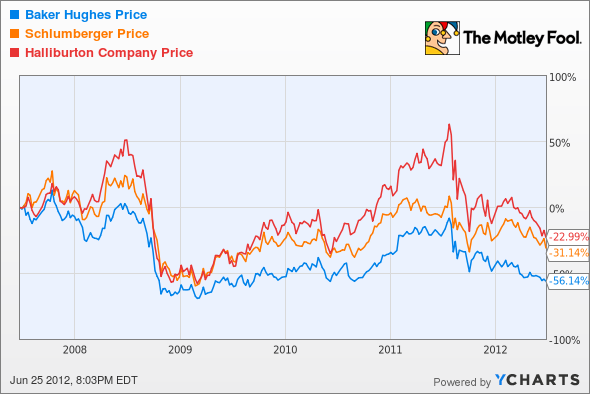

How it stacks up

Let's see how Baker Hughes stacks up next to its peers:

Despite legal issues associated with the Deepwater Horizon rig disaster, Halliburton (NYS: HAL) has outperformed both Baker Hughes and sector giant Schlumberger (NYS: SLB) over the past five years; although make no mistake about it, these are not returns to write home about.

Company | Price/Book | Price/Cash Flow | Forward P/E | Debt/Equity |

|---|---|---|---|---|

Baker Hughes | 1 | 12.3 | 8.3 | 27.6% |

Schlumberger | 2.5 | 13.4 | 11.3 | 31.3% |

Halliburton | 1.8 | 6.5 | 6.9 | 34.8% |

Source: Morningstar, Yahoo! Finance.

This is one of those rare cases where there isn't a huge difference between these three oil service giants. Even with sizable amounts of debt for all three, strong cash flow from operations and the value of their assets means there's little worry in covering interest payments. All three are also reasonably valued with Baker Hughes trading right around book value and Halliburton at just seven times forward earnings.

The only true differentiating factor between these three stocks is inherent risk. Halliburton is currently being sued by BP for costs incurred at Deepwater Horizon and could trade cheaply until that weight is lifted from its back. Both Baker Hughes and Schlumberger are suffering from transitional risk as they shift their product lines away from natural gas and toward oil-based drilling.

What's next

Now for the $64,000 question. What's next for Baker Hughes? That question is going to depend on whether or not drilling demand for oil remains strong (which is itself dependent on oil prices remaining high), and if it can successfully regain its pressure segment pricing power.

Our very own CAPS community gives the company a four-star rating (out of five), with a whopping 96.3% of members expecting it to outperform. Although I've yet to make a CAPScall on the company, I'm now ready to enter a rating of outperform on Baker Hughes.

The reasons for the outperform rating are pretty simple. For one, Baker Hughes is growing margins at a faster clip than both Halliburton and Schlumberger which should help close that huge performance gap over the past five years. Second, rig counts are up, not down, year-over-year which I see as a good sign for overall industry health, despite the oil-to-gas transition. Finally, Baker Hughes has performed well internationally with Latin America and Europe/Africa/Russia's Caspian region demonstrating double-digit revenue growth. This is cheap growth at a reasonable price and I'm happy to add it to my CAPS portfolio here.

Baker Hughes isn't the only stock that looks ready to take advantage of consistently high oil prices. Our analysts at Motley Fool Stock Advisor have weeded through countless oil and gas companies to find the top three that'll benefit as oil prices rise. We've already taken a quick look at Schlumberger, one of those selections. If you'd like to find out about the other two, simply click here for access to this free special report.

Craving more input on Baker Hughes? Start by adding it to your free and personalized watchlist. It's a free service from The Motley Fool to keep you up to date on the stocks you care about most.

The article Are Baker Hughes' Fortunes About to Turn? originally appeared on Fool.com.

Fool contributor Sean Williams has no material interest in any companies mentioned in this article. You can follow him on CAPS under the screen name TMFUltraLong, track every pick he makes under the screen name TrackUltraLong, and check him out on Twitter, where he goes by the handle @TMFUltraLong.The Motley Fool owns shares of Chesapeake Energy. Motley Fool newsletter services have recommended buying shares of Chesapeake Energy and Halliburton. Try any of our Foolish newsletter services free for 30 days. We Fools don't all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.

Copyright © 1995 - 2012 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.