What Do You Want From Your Dow Stocks -- Dividends or Capital Gains?

Coca-Cola (NYS: KO) , IBM (NYS: IBM) , and General Electric (NYS: GE) have a lot in common. They are all Dow Jones Industrial Average (NYS: ^DJI) component stocks, pay a dividend, and have huge cash flows. What these companies do with their cash should influence Foolish investment decisions.

Make no mistake -- cash flow is a very important component of determining earnings quality. Here is a list of possible uses for cash:

Acquisitions

Dividends

Stock buybacks

Investments

Loans

Dormant (do nothing)

I want to focus on dividends versus stock buybacks in this commentary. First, let's take a look at these companies' current dividend policies.

Stock | Dividend | Yield | Stock Price |

|---|---|---|---|

Coca-Cola | $2.04 | 2.7% | $75.00 |

IBM | $3.40 | 1.7% | $194.80 |

GE | $0.68 | 3.5% | $19.40 |

Source: Yahoo! Finance.

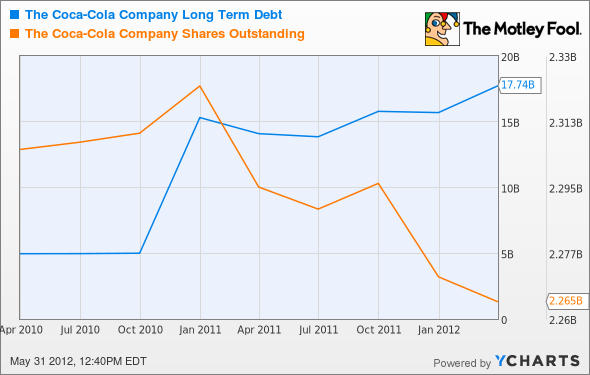

Coca-Cola

KO Long-Term Debt data by YCharts.

The chart above illustrates that in early 2011, Coke stepped up stock repurchases while adding debt to its balance sheet, suggesting that some of this debt was used for that purpose. Stock buybacks are considered bullish, but adding debt is not. The table below lists cash-related activities during 2010 and 2011.

Metric | Jan. 1, 2010 to Dec. 31, 2011 |

|---|---|

Net Long-Term Debt Issued (billions) | $6.813 |

Net Cash +/- (billions) | $5.782 |

Acquisitions (billions) | $3.488 |

Net Share Repurchases (billions) | $4.239 |

Shares Repurchased (millions) | 24 |

Dividends Paid (billions) | $8.368 |

Dividends Per Share Paid | $3.64 |

Stock Price +/-% Average Gain | 13.59% |

Stock Price With Dividend +/-% Average Gain | 16.89% |

Dividend Yield | 3.3% |

Source: TMF EQ Database.

Among other things, Coke repurchased 24 million shares for net $4.239 billion and paid $8.368 billion in dividends. Could the cash used for share repurchases have better benefited shareholders by increasing the dividend instead?

Metric | 2010 | 2011 |

|---|---|---|

Net Income (billions) | $11.8 | $8.572 |

Earnings Per Share | $5.12 | $3.75 |

Shares Outstanding (billions) | 2.308 | 2.284 |

Source: S&P Capital IQ.

From the table above, Coke's share buybacks represent $0.04 of 2011 per share earnings difference, or about $0.75 of Coke's share price. In January 2010, Coke's stock price was $55.15, and if you held 100 shares through the end of 2011, you would have received $364 in dividends and the stock would be worth $7,014 for a grand total of $7,378, or a 16.89% average annual return. The return without dividends would have been a 13.59%, so the dividend yield is 3.3%. The $0.75 share price difference reduces the total return by only 0.67% to 16.22%. If the $4.239 billion used to repurchase shares had instead been used to pay higher dividends, shareholders would have received $5.48 in dividends instead of $3.64, or a total return of 17.89%. Rational Foolish investors would prefer the higher dividend.

Clearly, however, it is in management's best interests to grow the stock price; that's how they get paid the big bucks! Because Wall Street focuses on revenue, earnings per share, and future guidance, a higher EPS will influence investor behavior and hopefully the stock price will rise due to buying activity. Mathematically, less shares in circulation equals a higher EPS. In Coke's case, the strategy seems to have worked even in a year when EPS actually declined.

Coke has raised its dividend consistently and can be expected to continue this policy. Even if share-price growth slows, and despite Coke's added debt levels, its healthy yield far outpaces bond yields, and the stock may be considered as a long-term buy.

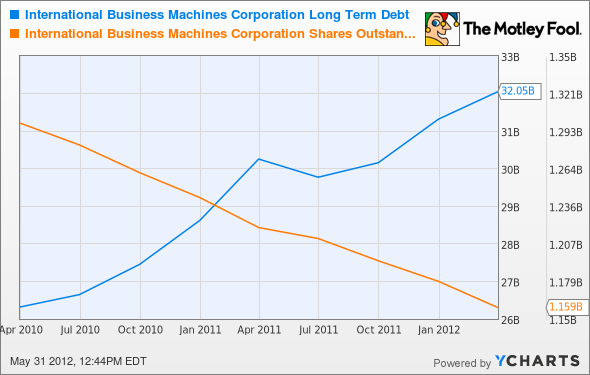

IBM

IBM's chart shows that it has added debt while simultaneously reducing its float, much like Coke. IBM's average annual return for 2010 and 2011 was 19.75%. Adding in $5.50 in dividends boosts the average return to 21.85%, or a yield of 2.1%. During this time IBM spent net $24.194 billion to eliminate 71.8 million shares, which boosted net income in 2011 by $0.75 and is worth $10.34 in share price. Without the boost to earnings through stock repurchases, the return would have been 15.8%, a difference of nearly 4%.

IBM Long-Term Debt data by YCharts.

IBM also added net $2.582 billion in long term debt and paid $6.65 billion in dividends. If only half of the $24 billion that was used to repurchase stock had instead been paid to shareholders in dividends, shareholders would have received $12.00 in dividends instead of $5.50. This $12.00 translates into 4.59% dividend yield, which is more than the return provided by artificially boosting net income to achieve higher earnings per share and share price. In general, my opinion is that the earnings quality of IBM relative to Coke is lower, which should be factored into consideration.

General Electric

GE Long-Term Debt data by YCharts.

By contrast, GE has reduced both shares outstanding and long term debt.

Metric | Jan. 1, 2010 to Dec. 31, 2011 |

|---|---|

Net Long-Term Debt Repaid (billions) | $94.149 |

Net Share Repurchases (billions) | $2.718 |

Dividends Paid (billions) | $11.248 |

Dividends Per Share Paid | $1.00 |

Stock Price +/-% Average Gain | 6.17% |

Stock Price With Dividend +/-% Average Gain | 9.19% |

Source: TMF EQ Database.

GE spent $2.718 billion to reduce its float by 70 million shares. This was worth $0.01 per share earnings, or only $0.15 share price. Average annual return with this price adjustment is lower at 5.72%. If this money were used to pay higher dividends, it would have added $0.24 to shareholders' wallets, or a total yield of 9.91%. Again, shareholders would prefer the higher yield. The good news is that GE Capital is again paying dividends to its parent, and GE has rapidly increased its dividend since 2009 and is deleveraging its balance sheet. However, GE is the most opaque company of the three. They no longer bring good things to life and one cannot be certain where earnings are being generated in any given quarter.

Metric | 2010 | 2011 |

|---|---|---|

Net Income (billions) | $11.344 | $13.120 |

Earnings Per Share | $1.06 | $1.24 |

Shares Outstanding (billions) | 10.661 | 10.591 |

Source: S&P Capital IQ.

Foolish takeaway

Among the three, Coca-Cola is the least difficult business to understand and has easily assessable earnings quality. Despite buying back shares to boost earnings, the yield is still relatively attractive and people will be quenching their thirst with Coke for decades to come.

One of the great things about companies like Coca-Cola, IBM, and GE is the great dividends they pay, but there are even better ones out there. You can read about them in our special free report: "Secure Your Future With 9 Rock-Solid Dividend Stocks." To see which dividends made the grade, click here now.

The article What Do You Want From Your Dow Stocks -- Dividends or Capital Gains? originally appeared on Fool.com.

Fool contributor John Del Vecchio is co-advisor to Motley Fool Alpha and co-manager of the Active Bear ETF. You may follow him on Twitter @johnfdelvecchio. He does not own any shares in the companies mentioned in this article. The Motley Fool owns shares of IBM and Coca-Cola. Motley Fool newsletter services have recommended buying shares of Coca-Cola and creating a synthetic long position in IBM. The Motley Fool has a disclosure policy.

We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insightsmakes us better investors. Try any of our Foolish newsletter services free for 30 days.

Copyright © 1995 - 2012 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.