This Mortgage REIT Looks Riskier Than Its Peers

For years, investors have been turning to real estate investment trusts as an alternative way to generate income from their portfolios. In particular, mortgage REITs, which use substantial leverage to buy mortgage-backed securities, have become incredibly popular, thanks to their double-digit dividend yields.

Yesterday's announcement from the Federal Reserve that it fully intends to do everything in its power to keep interest rates down for at least the next two years supported the bull case for mortgage REITs generally. But increasingly, it looks like there's a divide in the mREIT space, and investors should be aware of the implications before they choose one particular mREIT over another.

Diving dividends

Earlier this week, Chimera Investment (NYS: CIM) announced that it would reduce its second-quarter dividend to $0.09 per share, from its previous $0.11-per-share payout last quarter. The cut represents the fifth time the mortgage REIT has reduced its payout in less than two years, and the new payout will be exactly half what it paid in September 2010. Shares plunged more than 5% yesterday on the news, even as many other REITs rose.

By contrast, the dividend bug hasn't hit other mortgage REITs as badly. Annaly Capital (NYS: NLY) has also reduced its payout several times in recent years, but its payout has dropped by a little more than a quarter of its peak, and Annaly was able to sustain its current dividend for the second quarter. American Capital Agency (NAS: AGNC) has had an even longer track record of keeping its payouts stable, with the REIT making only two cuts since its 2009 peak payout and maintaining its $1.25-per-share quarterly distribution this quarter. ARMOUR Residential's (NYS: ARR) dividend is still more than 80% of its level from late 2010.

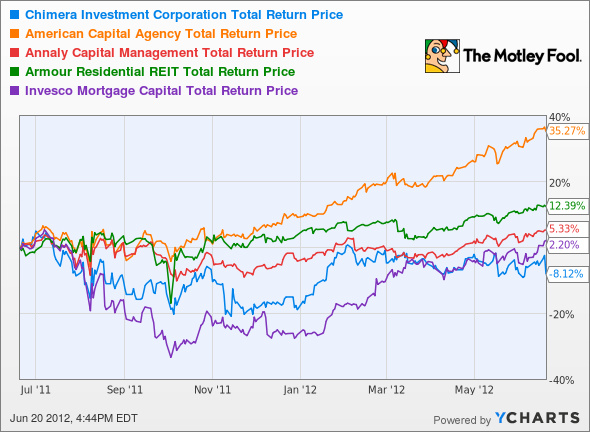

Chimera's falling dividends have hurt its returns badly. Even with a trailing dividend yield of 16.5% having supported its total returns, shares fell enough to give it a negative total return over the past year. As you can see below, that doesn't compare favorably with its peers.

CIM Total Return Price data by YCharts

One conclusion you could draw from this is that non-agency-backed mortgage debt hasn't performed as well as agency debt. Unlike Annaly, American Capital Agency, and ARMOUR, Chimera has substantial holdings of mortgage debt that's not backed by Fannie Mae or Freddie Mac.

The recent dividend cuts from Invesco Mortgage Capital (NYS: IVR) , which also carries debt other than agency-backed mortgage securities, tend to support that conclusion. Invesco did manage to sustain its $0.65-per-share dividend this quarter, but the payout is down 35% from its levels just a year ago. Still, it's managed to do what Chimera couldn't: eke out a positive total return.

Uncertain valuations

But another problem that has plagued Chimera has to do with accounting for non-agency mortgage debt. Chimera hasn't filed its annual report for 2011 or its first-quarter report for 2012, citing the need to "review the application of GAAP guidance to certain of its non-Agency assets." Then in March, Chimera's audit committee dismissed Deloitte & Touche as its accounting firm, replacing it with Ernst & Young.

Chimera has done its best to downplay the situation, arguing that while the "review may result in a material non-cash change in the GAAP operating results of the Company," it "will not affect the Company's previous announced GAAP or economic book values, actual cash flows, dividends and taxable income for any period." Nevertheless, its not being able to file reports for so long makes any investor nervous, especially in light of some of the accounting scandals that have plagued other sectors of the market in recent years.

What to do

Chimera has always been different from its mortgage REIT peers. In addition to its non-agency debt holdings, Chimera also uses far less leverage than its agency-focused peers -- perhaps because getting financing using agency debt as collateral is likely easier than for non-agency-backed securities.

Regardless of any accounting uncertainties, Chimera is clearly facing a more challenging business environment given its payout reductions, which signal lower net income. It does trade at a discount to book value, which suggests a potential bargain. But with shares that have been far more volatile, smart investors may decide that it makes more sense to stick with more predictable agency-focused mortgage REITs for now.

Instead of having to guess when mortgage REITs may cut dividends again, why not focus on companies that have grown their payouts over time? You can find some great examples in the Fool's special report on dividends, where you'll learn about nine stocks that will help you secure your future. It's free, so click here and get your copy today!

The article This Mortgage REIT Looks Riskier Than Its Peers originally appeared on Fool.com.

Fool contributor Dan Caplinger doesn't mind risk if the reward is there. He doesn't own shares of the companies mentioned. You can follow him on Twitter @DanCaplinger. The Motley Fool owns shares of Annaly Capital. Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Fool's disclosure policy is a risk-free proposition.

Copyright © 1995 - 2012 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.