3 Stocks to Sell Now

Unless Congress can agree on a plan to stave off cuts scheduled to begin in January, military spending will be reduced by $492 billion over a decade, with the first $55 billion cut in January. Domestic programs also will face reductions by $492 billion over a decade. These automatic cuts will occur because of the bipartisan congressional panel's failure last year to agree how to cut the deficit by $1.2 trillion over 10 years.

While not much will happen before November's elections, defense companies have already begun preparing for these cuts.

General Dynamics (NYS: GD) is heavily involved in all aspects of military and defense systems development and production -- land, sea, and air. Since the start of this year, GD's earnings quality has declined from an "A" to a "C."

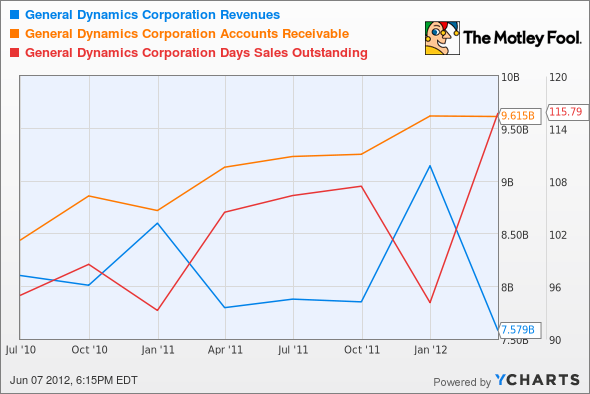

GD Revenues data by YCharts.

GD's chart should sound some alarms. Revenue is declining while accounts receivables and days sales outstanding are increasing. Receivables as a percentage of revenue are at 127% and growing. GD's high cost of sales means its gross margin is only 18%, which does not leave much room for operating or profit margins. In the face of potential defense spending cuts, GD added 5,000 employees last year and 11,500 since 2007. The company's cash conversion cycle -- the time it takes to convert sales to cash -- also has grown from 95 days to 115 days in two years. The government takes its sweet time paying its bills.

More alarms: Unearned revenue on the balance sheet -- prepayments for work or products that have not been delivered -- is declining and is a paltry $1.049 billion. GD also has $269 million and $310 million in deferred tax assets, and long-term deferred tax assets, respectively. This is a reserve account that will be used to pay future tax liabilities, and it will hurt cash flow when the account has been depleted. Last but not least, GD has a negative $4.68 tangible book value per share.

On Friday, June 8, the Navy awarded Raytheon (NYS: RTN) a continuation of a long-term contract to build Tomahawk Cruise Missiles, valued at $336 million. Raytheon has a TMF EQ Score rank of "D," which was "A" in January, so this contract may stave off the inevitable layoffs that many defense contractors have recently threatened. Full-time head counts have decreased year over year by 1,100 employees to 71,000. Raytheon's revenue metrics are very similar to GD's -- revenue was down slightly to $24.743 billion trailing 12 months. Gross margin is low at only 22%, but it's better than GD's 18%. Operating cash flow margin is decent at 9%. Raytheon's receivables are at "only" 81% of revenue.

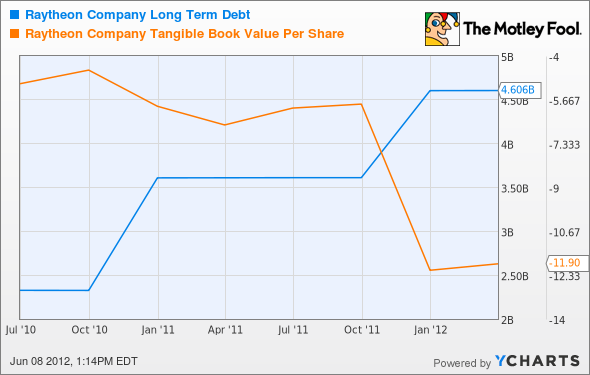

RTN Long Term Debt data by YCharts.

While most of Raytheon's metrics are better than GD's, alarm bells clang around its negative tangible book value of -$12.64 a share and rising long-term debt, which stands at $4.606 billion. Raytheon is not going out of business anytime soon, but tangible book value equals assets minus liabilities and intangibles like goodwil. The stock price has hardly moved since January, and the forward P/E of 9.16 is only slightly better than the trailing P/E of 9.41. This means that estimated earnings are not great. Perhaps the only thing great about owning Raytheon is the current 3.90% annual dividend yield ($2.00).

Northrop Grumman's (NYS: NOC) earnings quality rating moved down from "A" to "D" since January. Revenue metrics look similar to GD and Raytheon, as revenue declined 7.5% last 12 months from $27.963 billion to $25.896 billion. Of the three companies, balance sheet metrics look the best with receivables at 52% of revenue, and days sales outstanding at 48 days. Northrop takes only 40 days to convert sales into cash.

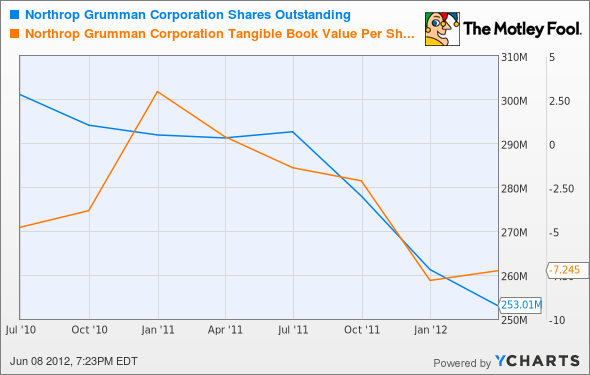

Alarm bells! Staffing dropped from 117,110 to 72,500 last year but 38,000 of the 44,610 jobs lost went with Huntington Ingalls Industries (NYS: HII) , Northrop's shipbuilding spinoff. Deferred revenue dropped from $1.9 billion to $1.75 billion during the year, indicating that the amount of available project work may be decreasing. Northrop's tangible book value is at negative $7.24 a share, and the company has also repurchased a lot of its shares. While Northrop has an operating cash flow margin of 8%, free cash flow was negative last quarter at -$182 million.

NOC Shares Outstanding data by YCharts.

Northrop's trailing P/E of 7.76 is smaller than the forward P/E of $8.54. Northrop pays a $2.20 dividend (3.60%), but there are a lot of safer stocks out there.

Foolish takeaway

Hard economic times warrant taking a defensive posture with your portfolio. Defense stocks are not defensive investments! Foolish readers should always make their investment decisions based on earnings quality.

To stay current on whether General Dynamics' earnings reports meet or beat expectations, be sure to add it, or any of the other companies mentioned here to My Watchlist, a totally free service offered by The Fool that keeps you current on your favorite stocks. Get started with the links below.

Add General Dynamics to My Watchlist.

Add Raytheon to My Watchlist.

Add Northrop Grumman to My Watchlist.

At the time thisarticle was published Fool contributorJohn Del Vecchiois Co-Advisor to Motley Fool Alpha and co-manager of the Active Bear ETF. You may follow him on Twitter @johnfdelvecchio. He does not own any shares in the companies mentioned in this article. The Motley Fool has adisclosure policy.

Copyright © 1995 - 2012 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.