Time to Buy Rambus?

Rambus (NAS: RMBS) recently made headlines because small-cap research firm Sidoti & Co. initiated a "buy" rating with a $10 price target. The stock surged more than 6% ($0.31). As Foolish readers know by now, many investors will attempt to make a short-term profit by buying when there appears to be some enthusiasm around a stock, and then quickly selling to lock in the gain. With a $5 price target, 1,000 shares would have rewarded the nimble hit-and-run artist with a one-day gain of $310, assuming they got in at $5 and got out at $5.31, the closing price.

We don't recommend this type of speculation because it amounts to gambling and, statistically speaking, you only win 50% of the time. But it's worth looking at Rambus' trend data over the last two years to see if it might be worthwhile to put your toe back into the water, metaphorically speaking; to hold it if you are currently a shareholder, or to sell and wait for a re-entry point.

Rambus is a small-cap information technology company that creates, designs, develops, and sells patent licenses for architectures to digital electronics products and systems, and light emitting diode technology as well as computer systems security, among other things. The company carries no inventory, which is common among such companies.

The company notes in its annual report that the majority of revenue comes from licensing its cache of 1,386 patents using fixed, variable, or fixed and variable payments that can be one payment or a series of payments over time. Rambus had $312.7 million in revenue last 12 months versus $224.05 million the 12 months prior. However, expected revenue for this fiscal year is $248.1 million. Revenue should always be your starting point when considering a stock, and so you need to look at the income statement.

I'll go easy on these quarterly metrics, but after reviewing you should get the picture.

Metric | 3/31/2012 | 3/31/2011 | 3/31/2010 |

|---|---|---|---|

Cost of goods sold | 11% | 5% | 1% |

Selling, general & admin. | 46% | 38% | 15% |

Gross margin | 89% | 95% | 99% |

Operating margin | (19%) | 20% | 70% |

Net profit margin | (44%) | (7%) | 93% |

Earnings per share | ($0.25) | ($0.04) | $1.28 |

Source: S&P Capital IQ.

Clearly, Rambus' costs have spiraled out of sight. Notably, while the cost of goods sold is only 11%, meaning its variable and project-based costs are low, SG&A costs are very high at 46%, and the table does not show another $38.4 million in research and development costs during the quarter that caused the operating margin to drop to 19%.

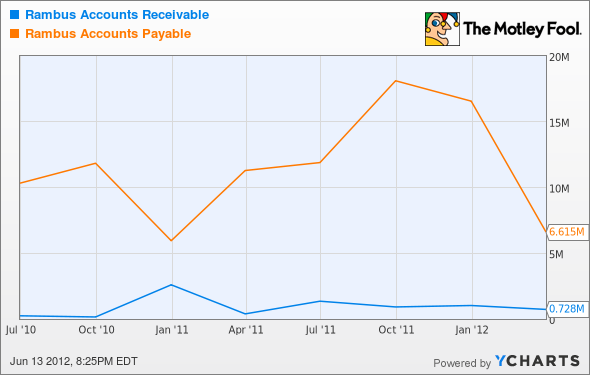

Unfortunately, the cash picture looks bleak as well. Operating cash flow margin for the last 12 months is at 15%, down from a recent high of 73%. For the most recent quarter ending March 31, operating cash flow was -$10.9 million. It only takes Rambus one day to collect its receivables, probably because they don't have many receivables -- only $728,000. Payables were at $6.62 million and days payable outstanding -- the time taken to pay its bills -- averaged 172 days, way down from last year's 470 days.

RMBS accounts receivable data provided by YCharts.

Whenever payables greatly exceed receivables both in terms of size and time taken to collect versus pay, you should recognize that the company may have cash flow problems. Simply put, it is very difficult to pay your bills when you don't have cash on hand to pay. Long-term debt must be used to replenish cash accounts, especially when cash from operations is negative.

Since Rambus' earnings were negative last quarter (at -$0.25 a share), negative the last 12 months (at -$0.60) and analysts are projecting more losses this year, earnings can't help in the decision to buy, sell, or hold. The book value (value of total assets minus total liabilities) is $408.4 million, or $3.70 a share, but goodwill and other intangibles is $333.6 million, or 81.7% of book value. This is much too high; it may indicate overvalued assets on the balance sheet. The tangible book value is only $0.68 a share, versus $1.20 at the end of 2011, and $2.68 in 2010. While it's really hard to put a value on patents owned, if Rambus were to declare bankruptcy, after payments to debtors and taxes, there would not be much left over for shareholders.

RMBS long-term debt data provided by YCharts.

Foolish takeaway

To summarize, the fundamentals don't support a $10 stock price. Rambus is a company in decline that has not yet taken the painful steps to reduce costs. The company employs only 456 people, but is overwhelmed with overhead and R&D costs that are too high, while variable and direct costs are, frankly, too low. Declining revenue projections suggest a slowing sales pipeline and, more importantly, the need for a sales model with a higher recurring revenue stream. If Rambus were to sell some patents it would provide a one-time revenue event, but this is unsustainable to revenue or earnings. A sell order would be in order, as well as a close eye focused on improvements in costs and revenues to find a re-entry point.

To stay current on whether Rambus' earnings meet or beat expectations, be sure to add it, or any of the other companies mentioned here to My Watchlist, a totally free service offered by The Motley Fool that keeps you current on your favorite stocks. Also, if you'd like to read up on our analysts' top idea for capitalizing on the next trillion-dollar revolution in mobile, take a look at our special free report by clicking here now!

At the time thisarticle was published Fool contributorJohn Del Vecchiois co-advisor to Motley Fool Alpha and co-manager of the Active Bear ETF. You may follow him on Twitter @johnfdelvecchio. He does not own any shares in the companies mentioned in this article. The Motley Fool has adisclosure policy. We Fools may not all hold the same opinions, but we all believe thatconsidering a diverse range of insightsmakes us better investors. Try any of our Foolish newsletter servicesfree for 30 days.

Copyright © 1995 - 2012 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.