Cummins and These Two Stocks Look Incredibly Cheap

The recent market pullback has been harder on some stocks than others. Cyclicals, for example, have taken a beating as concerns over Europe and China have caused some investors to flee the high-beta stocks. But the recent downturn presents some excellent buying opportunities in this sector, among them engine-maker Cummins (NYS: CMI) . The share price of the manufacturer has fallen over 25% in the last three months despite no particular disappointing news to come out of the company. Cummins has beaten earnings estimates the last four quarters, and the stock now trades at a bargain-basement P/E of 9.3 with a forward multiple of 8.

Let's take a look at some other reasons the company looks like a buy.

History

Cummins may not have the brand premium that consumer-facing giants like Coca-Cola or Johnson & Johnson do, but founded in 1919 as one of the world's first diesel engine manufacturers, the company is just about as reliable. Revenues have grown consistently over the last 10 years, and shares have appreciated by about 1,000% in that time. Its balance sheet looks solid with twice as much cash as long-term debt, and it operates in over 190 countries and territories.

As an industry leader, Cummins sits on a number of valuable patents, and its experience in meeting strict EPA regulations gives it an advantage in competing in other countries where environmental regulations are expected to become tougher.

Growth

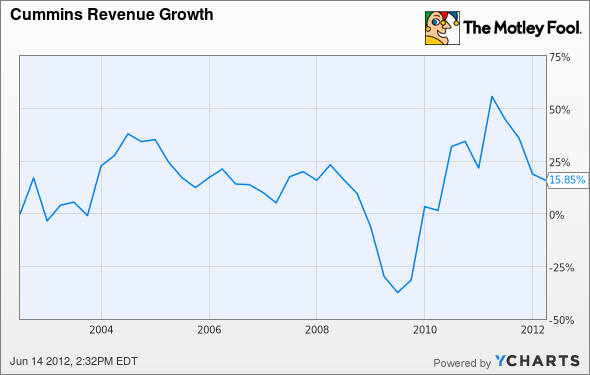

While Cummins is certainly a mature company, sales continue to forge ahead as the company finds new opportunities abroad.

CMI Revenue Growth data by YCharts

Sales climbed 36% last year, and analysts expect revenue to continue to grow around 10% this year and next with EPS jumping even more. Emerging markets have become a huge opportunity for the company as trucking is the lifeblood of the modern economy. In 2010, sales in China and Brazil grew by 70%, and sales in India increased 37%. While international growth appears to be slowing down with the global economy, it still remains an excellent long-term opportunity.

Natural gas opportunities

Westport Innovations (NAS: WPRT) may be getting much of the attention in the natural gas fuel market, but Cummins may be as big of a player as any when all is said and done. The joint venture between the two contributed more than half of Westport's revenue in its most recent quarter, and that segment is by far the most profitable part of Westport's business, contributing $4.8 million in net income in the last quarter to the still unprofitable company.

Cummins isn't stopping with the JV. In March, it said it would be developing a natural gas engine of its own: a 15-liter, heavy-duty, spark-injected version meant for on-highway applications. Production will start in 2014. Given its expertise and experience in diesel-engine building and its early inroads into natural gas engines, Cummins figures to be a major player if natural gas fueling takes off as some hope it will.

Other plays in the area

Cummins isn't the only machinery maker getting beaten down by the market pullback. Shares of earth-moving-equipment maker Caterpillar (NYS: CAT) are off almost 25% over the last three months. The stock has sunk so low that it trades at a forward P/E of just 7.6, and the manufacturer has also made moves into the natural gas game, recently announcing its own partnership with Westport to make natural gas engines for mining trucks and locomotives in response to growing demand for natural gas-powered vehicles.

Finally, Deere (NYS: DE) looks like a value play at today's prices. Shares of the world's largest maker of farm equipment are down about 15% from highs earlier this year, dropping its forward P/E down to 8.8. Meanwhile, earnings estimates have jumped in the last 30 days, and analysts are expecting revenue growth at 16% for the year.

All three of these machinery companies are industry leaders with brand value and staying power. They make necessary products that, while cyclical, need to be replaced and upgraded often. Despite an economic slowdown, their core business is not going away. Mr. Market looks foolish for discounting them so deeply.

To make matters more enticing, this group of stocks all pay solid dividends. If you're looking for more dividend picks, we've got a brand-new special free report on the best dividend payers in the Dow. It highlights three stocks that are all dividend aristocrats, consistently raising their payments, and that operate in stable businesses that will allow them to keep returning cash to shareholders for years to come. Get the names of these great companies in our free report: "The 3 Dow Stocks Dividend Investors Need." You can get your copy now by clicking right here.

At the time thisarticle was published Fool contributorJeremy Bowmanholds no positions in the companies in this article. The Motley Fool owns shares of Westport Innovations. Motley Fool newsletter services have recommended buying shares of Cummins and Westport Innovations. The Motley Fool has a disclosure policy. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. Try any of our Foolish newsletter services free for 30 days.

Copyright © 1995 - 2012 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.