3 Reasons to Sell Deckers Outdoor

Specialty footwear manufacturer Deckers Outdoor (NYS: DECK) may have a list of pros working in its favor, but there are also a few cons. Check out some recent stats on the maker of Ugg boots, then read on to find out why this company may not be the perfect fit for your portfolio.

52-Week High | $118.90 |

52-Week Low | $47.01 |

Market Cap | $1.85 billion |

Price/Earnings Ratio | 10.03 |

CAPS Rating (out of 5) | *** |

Source: Yahoo! Finance.

1. Dependence on one brand in a portfolio of six

Across all of the company's distribution channels (wholesale, e-commerce, and direct retail), the Ugg brand accounted for 87.3% of sales in 2011. The next 9% went to Teva.

That's not a lot of diversity, and it leaves Deckers extremely vulnerable. Not only is the world of fashion finicky, but UGG boots are specifically suited for cold winters. This year's early mild temperatures hurt sales, which caused the company to come in below analysts' expectations in the first quarter.

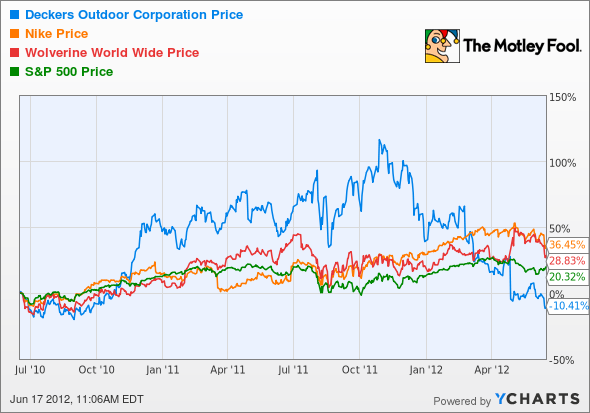

The stock fell 25% that day. Take look at how unstable it has been compared to competitors Nike and Wolverine World Wide:

2. The rising cost of supplies

Another reason investors should be weary of the dependence on the Ugg brand is the rising cost of supplies, especially sheepskin.

Deckers has done well establishing itself as a company that puts forth quality shoes. For Ugg boots, that means using only a specific type of sheepskin. So specific, in fact, that it leaves the company reliant on just two tanneries in the entire world. This doesn't give it a lot of pricing power, especially as supply has been steadily decreasing. In 2011 the price increased 27%, and in 2012 the company expects a 40% jump.

An 18.93% profit margin gives it some wiggle room, but investors need to ask how long the company can realistically absorb these costs. Uggs already have a high price tag, and as more and more imitators enter the market, it may be difficult for the company to justify that price tag, let alone raise it.

3. Dependence on a few big customers

In 2011, five of Deckers' largest customers (including Nordstrom, REI, and Zappos.com) accounted for 24% of overall sales. This was an improvement over 2010's 28.9%, but it's still a high number. The company prefers to sell its products to specific retailers in order to maintain its brands' niche images, but it might be worth diversifying for some added security.

Overall, Deckers has left itself vulnerable to a number of outside forces, and investors should take note. Knowing when to sell a company is tough, but finding great new companies to take its place in your portfolio can be even harder. Luckily, our analysts have put together a special free report full of information about three great stocks that can help you retire rich. Click here to read it now!

At the time thisarticle was published Fool contributor Amanda Buchanan holds no position in any company mentioned. Click here to see her holdings and a short bio. The Motley Fool has a disclosure policy. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. Try any of our Foolish newsletter services free for 30 days.

Copyright © 1995 - 2012 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.