Analysts Debate: Is Life Technologies a Top Stock?

The Motley Fool has been making successful stock picks for many years, but we don't always agree on what a great stock looks like. That's what makes us "motley," and it's one of our core values. We can disagree respectfully, as we often do. Investors do better when they share their knowledge.

In that spirit, we three Fools have banded together to find the market's best and worst stocks, which we'll rate on The Motley Fool's CAPS system as outperformers or underperformers. We'll be accountable for every pick based on the sum of our knowledge and the balance of our decisions. Today, we'll be discussing Life Technologies (NAS: LIFE) , a research-focused biotechnology company that offers a range of medical and life science products, including genomic sequencing and medical consumables.

Life Technologies by the numbers

Here's a quick snapshot of the company's most important numbers:

Statistic | Result (TTM or Most Recent Available) |

|---|---|

P/E and Forward P/E | 18.2 / 9.5 |

Revenue | $3.82 billion |

Net Income | $417 million |

Free Cash Flow | $684 million |

Market Cap | $7.3 billion |

R&D Ratio | 9.7% |

Patents Held | More than 4,000 |

Sequencing Machines Sold | 700+ in 2011 |

Sources: Morningstar and company press releases.

Alex's take

Life Tech's made incredible progress against sequencing leader Illumina (NAS: ILMN) since buying start-up Ion Torrent two years ago. At the time of the acquisition, the company promoted Ion Torrent's machines in the $50,000 to $100,000 range. It's is now about to roll out a machine that's costlier, at $149,000, but which has achieved beyond-exponential increases in sensor density and total genome sequencing ability. The earlier machine's abilities topped out at about 165 million sensors, but the new Ion Proton machine, scheduled for wide release by the third quarter, will top out next year at 660 million.

The materials expenses of the Ion Proton push its per-genome sequencing cost under $1,000, which is an important barrier to widespread use. That puts the machine out ahead of Illumina's latest, which costs $740,000 and has not yet promised to bring per-genome costs below the four-figure threshold. Based on Life Tech's progress, sequencing should soon become very cheap:

Sources: National Human Genome Research Institute and author's calculations.

Life Tech and Illumina are both slightly down over the past two years, but Life Tech is now trading at a valuation more consistent with mature enterprises than high-growth stocks while Illumina maintains its sky-high P/E. Illumina's never traded below a 40 P/E in the past few years, while much of Life Tech's recent history has seen it trade for about half of that.

According to one market research report, the total global market for genome sequencing products was about $3 billion last year and will reach $6.6 billion by 2016. I think that may be an understatement, but based on Life Tech's and Illumina's reported earnings last year, each company controlled about a third of the total market. So why is the market treating Illumina like a sure thing and Life Tech as an also-ran, when Life Tech is far more diversified and can better withstand government cutbacks that slammed Illumina last year?

There are risks in such a fast-moving industry. Smaller competitors such as Pacific Biosciences (NAS: PACB) or Affymetrix (NAS: AFFX) might finally put out the world-beating sequencing systems they've promised for so long. Start-up genomics companies, such as Illumina-backed Oxford Nanopore, might push the technology past Life Tech's ability to catch up.

But today, Life Tech has the cheapest accurate sequencing machines and is backed by nearly twice as much annual R&D spending as Illumina. If the ultimate goal of a sequencing company is to make its products accessible to the average patient, Life Tech has to have the advantage. If it doesn't stumble, this is a stock for the long haul.

Sean's take

For anyone who's followed my views on the life sciences sector over the past year, you'd know that I'm incredibly optimistic regarding the potential for sustainable growth as the population grows and ages, and technologies become cheaper and more precise. Life Technologies looks like the perfect example of a company that not only is an ethically great investment that will change lives, but could also make investors a good deal of money over the long term.

As Alex explained, the driving force behind the company's recent stream of news is the release of its Benchtop Ion Proton Sequencer. Aside from sounding like futuristic device from Star Trek, this handy machine can sequence the human genome in just one day for the cost of $1,000. Compare that with previous models just a few years ago that took weeks and cost an average of $5,000 to $10,000, and you can see what a world of difference this technology is making. In addition, the cost of the sequencer, $149,000, is well below the $500,000 to $750,000 that similar sequencers cost just a few years ago.

For me, the most exciting tool in Life Technologies' arsenal of products is its Ion AmpliSeq Cancer Panels, which it recently presented at ASCO. The skinny is that this recently released machine allows scientists to screen dozens of genes in cancer research samples within hours. Currently it's capable of detecting 700 mutations in 46 known cancer genes. This type of research could drastically cut pre-clinical study time length and biotech research firm costs. In fact, GlaxoSmithKline (NYS: GSK) recently partnered with Life Technologies in late 2011 to develop a companion test for a cancer drug.

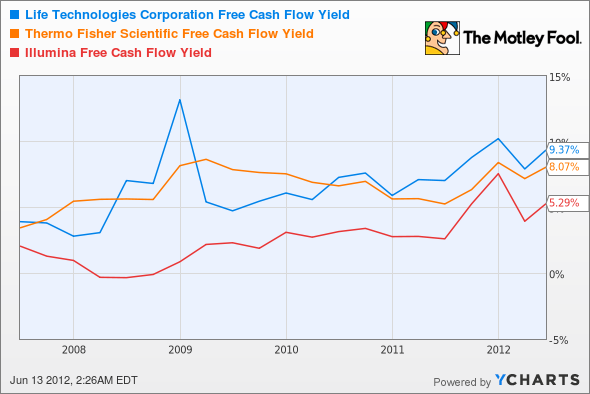

From a fundamental perspective, Life Technologies is -- not to sound like a bird -- cheap, cheap, cheap! Aside from trading at just under 10 times forward earnings, Life Technologies offers the biggest tell-tale sign of value in its free cash flow yield:

LIFE Free Cash Flow Yield data by YCharts

As you can see, Life Tech's free cash flow yield has been steadily on the rise, leaving Illumina in the dust. Simply put, it's producing more free cash flow from its operations relative to its market value than its peers; that's a formula for success and the final reason I think it's set to outperform.

Travis' take

There's no doubt that the products and services Life Technologies provides are exciting and have the possibility of changing medicine in a meaningful way, but we're getting gushy about a company that has a lot yet to prove. Alex wonders why the stock isn't trading at a higher multiple, but I see a company whose growth has gone from 28.7% growth over the past five years to 5.2% in the past year and will hit just 2% to 4% in 2012, according to management predictions.

My other problem is that Life Technologies is chasing lower costs in a business that has a lot of competition. Alex likes to compare this situation with Intel, but we aren't talking about a business that will go from hundreds of devices to billions, which is what drove Intel's sales higher even as individual chip costs went lower. There are limits to the number of sequencing machines needed, and as speed increases, the number needed actually decreases.

Pacific Biosciences, Affymetrix, and Illumina are all driving costs lower, and the advantage in genome sequencing doesn't seem to stay with one for long. I would compare the genome sequencing business with what's happened to solar companies in the past few years more than I would to chipmakers in the '80s and '90s. Margins will eventually compress, and you find yourself in a commodity business with lots of competition instead of a high-margin business.

In general I stay far, far away from medical stocks because they're far too risky, especially in today's environment, where spending is under pressure from the individual level to the government. Life Tech isn't as risky as most speculative medical stocks, because it does have a solid revenue stream, it's profitable, and the stock trades at a reasonable price, but I'm still not buying it.

I've seen too many companies build up hope that their technology will be the best thing since sliced bread, and they rarely pan out the way you expect. I wouldn't make an underperform call here; I would just stay away from this stock altogether.

The final call

Despite Travis' valid concerns, we (Alex and Sean) are bullish enough on Life Technologies to grant the company an outperform call on our TMFYoungGuns CAPS portfolio. As of this writing, our nine total picks were outperforming the market by a cumulative 59 points, and we expect that there'll be nowhere to go but up over the long term. We will keep an eye on this stock to make sure the commoditization Travis mentioned doesn't undermine our investing thesis, so stay tuned!

If you have an idea for another stock to cover in our weekly series, send us an email with your suggestions, and we might just take a look in the near future.

If you're looking for other great opportunities in next-gen medical technologies, The Motley Fool has just the stock for you. Find out everything you need to know about "The Next Rule-Breaking Multibagger" that's changing the way hospitals work while offering investors big gains at the same time. Claim your copy of our popular free report to get the information you need for a great buy today.

At the time thisarticle was published Fool contributor Travis Hoium manages an account that owns shares of Intel. Fool contributors Alex Planes and Sean Williams have no positions in any companies mentioned. You can follow Travis on Twitter at@FlushDrawFool, Sean at@TMFUltraLong, and Alex at@TMFBiggles.The Motley Fool owns shares of Intel.Motley Fool newsletter serviceshave recommended buying shares of Illumina, Pacific Biosciences of California, and Intel. The Motley Fool has adisclosure policy. We Fools don't all hold the same opinions, but we all believe thatconsidering a diverse range of insightsmakes us better investors. Try any of our Foolish newsletter servicesfree for 30 days.

Copyright © 1995 - 2012 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.