How Low Will Swift Energy Go?

Shares of Swift Energy (NYS: SFY) hit a 52-week low yesterday. Let's look at how it got here and whether clouds are ahead.

How it got here

Swift Energy began to tumble after reporting a disappointing first quarter and the perpetually low price of natural gas and the rapidly dropping cost of oil has resulted in the stock hitting new lows. Lower natural gas prices have already hit the company, resulting in weaker-than-expected revenue in the first quarter, and oil prices have only fallen since that time.

Management also said that capital spending would be at the top end of forecasts, flaming fears that costs are rising at the time energy prices are falling.

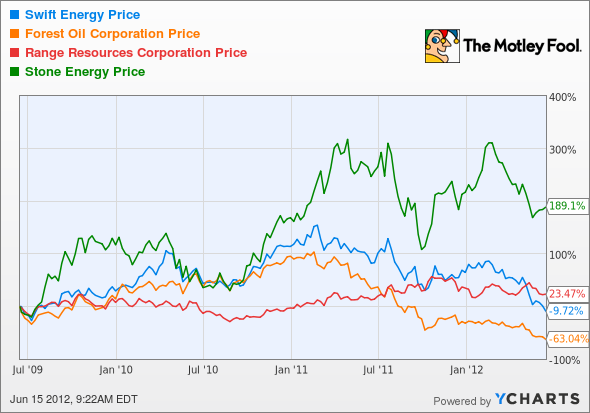

Swift Energy isn't the only one dealing with similar problems. Forest Oil (NYS: FST) , Range Resources (NYS: RRC) , and Stone Energy (NYS: SGY) have all struggled on the market recently. Just as energy producers begin to move production from low-margin natural gas wells to higher-margin liquid rich plays, prices fell out the bottom. As you can see in the chart below, the falling price of energy has affected these independent energy producers negatively this year.

From a fundamental perspective, these energy producers don't look too expensive. Swift's forward P/E is less than 10, price/book is less than 1, and profit margin is in the double digits -- all good signs for any stock.

Swift Energy | 0.7 | 13.8% | 4.7% | 8.3 |

Forest Oil | 0.7 | 15.6% | 6.4% | 8.2 |

Range Resources | 3.7 | 3.3% | 2.4% | 37.2 |

Stone Energy | 1.6 | 22.7% | 10% | 6.5 |

Source: Yahoo! Finance.

The worry is that lower prices will impact profitability, and I think that makes this a high-risk stock right now.

What's next?

Swift's stock has been hammered, but it could still go a lot further if energy prices continue to fall. The company has racked up $720 million of debt, and it needs to continue to generate cash to service that debt. Right now, operations are heading in the wrong direction, and net income per barrel of oil equivalent has fallen to $1.28 from $7.65 just three months ago. I'm afraid that may mean a loss per share next quarter.

The CAPS community has taken a tepid approach as well, giving the stock a middle-of-the-pack three-star rating (out of five).

The bottom line is that Swift Energy is largely at the whim of the price of oil and natural gas. If they keep falling, so will profitability, and there's no telling how low the stock can go. I would stay away from independent oil and gas stocks until the economy begins to pick up, which at this rate may be quite some time.

Interested in reading more about Swift Energy? Click here to add it to My Watchlist, which will find all of our Foolish analysis on this stock.

At the time thisarticle was published Fool contributor Travis Hoium does not have a position in any company mentioned. You can follow Travis on Twitter at @FlushDrawFool, check out his personal stock holdings or follow his CAPS picks at TMFFlushDraw.Motley Fool newsletter services have recommended buying shares of Range Resources Corporation Com. The Motley Fool has a disclosure policy. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. Try any of our Foolish newsletter services free for 30 days.

Copyright © 1995 - 2012 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.