Dangerously Difficult to Fix the Deficit

In a 2009 NBC/Wall Street Journal poll, 8 in 10 Americans said they were concerned about the federal deficit and growing national debt.

Are you one of them? If so, this quote from a report by the Congressional Budget Office released last week contains the 39 most important words you need to know:

If current laws were to remain generally unchanged ... the budget deficit would drop markedly over the next few years and debt held by the public would decline gradually, reaching about 60 percent of GDP by 2022, in CBO's estimation.

The dirtiest and most underappreciated secret about national debt is that if Congress and the president do absolutely nothing and don't agree on a thing -- which they're pretty good at -- then poof ... deficits decline, debt stabilizes and eventually shrinks, and America becomes the poster child for sovereign skinflints.

What has to be done for this to happen? Three things:

All of the Bush tax cuts need to expire on Jan. 1, 2013, as they're currently set to.

A scheduled 27% cut in Medicare payments to doctors needs to occur on Jan. 1. This has been on the books since 1997 but is temporarily patched through the so-called doc-fix.

Spending cuts mandated by last year's debt-ceiling deal have to actually happen.

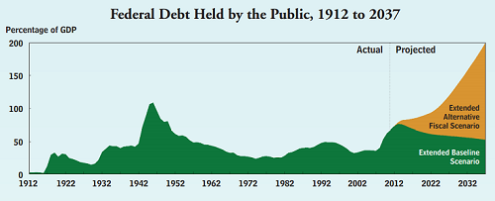

But as I've written before, almost no one wants to see all of this happen, especially right now. So rather than letting these three big policies play out as they're written on the books, a more likely outcome is what the CBO calls "alternative fiscal scenario," which includes tax cuts being extended, a continual patch on Medicare payments, and spending cuts being punted.

The difference between the two options is night and day:

Source: CBO.

The reason virtually no one wants to go down the low-debt path -- at least right now -- is clear and rational. If all tax hikes and spending cuts play out next year as they're currently on the books, the odds of falling back into a recession are high. People from nearly all political influences and economic backgrounds agree on that.

The scheduled cuts in Medicare payments are equally unrealistic, as a doctor who's closing his private practice recently described in a Colorado newspaper:

In the last 15 years, annual rates for primary care have been increased only once to match cost-of-living increases ... The prevailing wisdom is that no practice can survive with more than 20 percent of its patients being on Medicare. Summit Internal Medicine has a 40 percent Medicare population, and that is projected to only increase. Yet, the 20 percent benchmark would plummet if current Medicare rates are cut.

With the number of Americans relying on Medicare rising as baby boomers age, good luck getting those cuts past voters.

So, if one budget path leads to exploding deficits, and the other leads to a new recession and savage Medicare cuts, what's the answer (other than taking the fetal position)?

I think there are three things to keep in mind.

One, the most important assumption the CBO uses when forecasting a rise in long-term deficits is that health-care costs will surge, as they have in recent decades. Part of that is because of an aging population, but a lot is because of an assumed increase in the per-enrollee cost of programs like Medicare and Medicaid. Interestingly, though, it's becoming apparent that these assumptions could be way off. Growth in health-care spending has declined sharply and is now well below what was assumed just last year. Keeping that trend going could make a huge difference. As Annie Lowrey writes in the New York Times, "If the growth in Medicare were to come down to a rate of only 1 percentage point a year faster than the economy's growth, the projected long-term deficit would fall by more than one-third."

Second, and less optimistically, people like to point to the Bowles-Simpson budget proposal of 2010 as a sensible way forward. The abridged version of this means keeping stimulus (high spending and low taxes) today, while cutting the deficit back down the road when the economy is stronger and can handle it. This is an excellent idea in theory, but I doubt it could work in practice for a simple reason: An elected official will never make the argument that the economy is strong enough today to handle making current sacrifices, no matter how good things look. They're in the business of promising things will get better, not guilting you into feeling lucky today. And how do you know if the economy is strong enough to handle cutbacks? Today, we think of 2005 and 2006 as boom times, but people worried back then about how slow the economy was.

The final point might be the most important: It's unlikely that anything will be done to curtail the deficit until something bad -- like a big spike in interest rates -- occurs. As long as interest rates stay low, politicians will bloviate back and forth, but not much else. It takes a crisis to get people's attention. Until then...

At the time thisarticle was published Fool contributorMorgan Houseldoesn't own shares in any of the companies mentioned in this article. Follow him on Twitter @TMFHousel.The Motley Fool has a disclosure policy. We Fools may not all hold the same opinions, but we all believe thatconsidering a diverse range of insights makes us better investors. Try any of our Foolish newsletter services free for 30 days.

Copyright © 1995 - 2012 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.