How Low Can J.C. Penney Go?

Shares of J.C. Penney (NYS: JCP) hit a 52-week low on Tuesday. Let's take a look at how it got there and see whether cloudy skies are still in the forecast.

How it got here

If I didn't know any better, I'd almost guarantee you that if you looked up the definition of Murphy's Law in a dictionary, J.C. Penney's logo would be right next to it.

J.C. Penney has been losing market share to Macy's (NYS: M) and Nordstrom (NYS: JWN) for years. The company had been relying on steeper discounts to drive customer traffic, which ate into margins and gave it little room to grow and compete with the aforementioned mall anchors.

Rather than go down the same path, Penney's management went outside of the box and hired the mastermind behind the Apple retail store concept, Ron Johnson. When Mr. Johnson was an executive at Target (NYS: TGT) in the mid-1990s, he reinvigorated its previously stagnant growth by introducing brand-name apparel at a discount and turned it into a viable competitor to Wal-Mart (NYS: WMT) . At Apple, he transformed the computer company into arguably one of the most impressive retail forces in the world.

However, the actual results from Penney's recent quarter were absolutely dismal. Same-store sales figures plunged 18.9%, it suspended its dividend indefinitely, and it reported an adjusted-loss of $55 million. Most of this weakness can be traced to Penney's new pricing strategy which involves abandoning heavy discounts in favor of everyday low pricing with clearance events on the first and third Fridays of each month. After decades of offering discounts, many consumers are simply avoiding J.C. Penney or misunderstanding its new pricing practices.

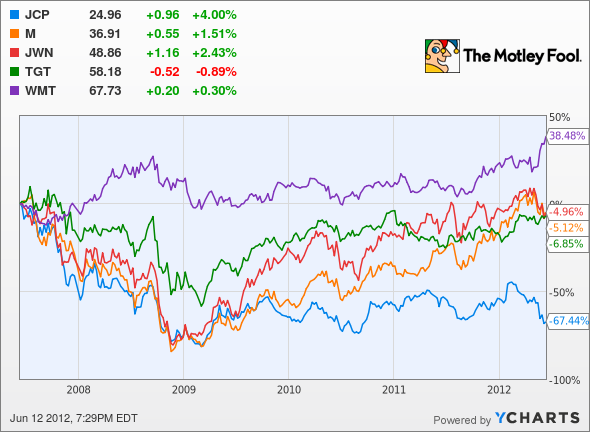

How it stacks up

Let's see how J.C. Penney compares to its peers.

I bet you never expected Wal-Mart to be that much of an outperformer in this group over the past five years. You can also see just how poorly Penney has performed relative to the group.

Company | Price/Book | Price/Cash Flow | Forward P/E | 5-Year Revenue CAGR |

|---|---|---|---|---|

J.C. Penney | 1.4 | 27.4 | 10.0 | (2.8%) |

Macy's | 2.6 | 6.9 | 9.8 | (0.4%) |

Nordstrom | 5.0 | 9.5 | 12.8 | 4.9% |

Target | 2.4 | 6.9 | 11.8 | 3.3% |

Wal-Mart | 3.3 | 8.5 | 12.7 | 5.1% |

Sources: Morningstar and author's calculations. CAGR = compound annual growth rate.

So how many of you predicted Wal-Mart would be the fastest-growing stock of this grouping over the past five years? My guess is fewer than 5% of you. It's not hard to see why Wal-Mart -- which in the other retailers' defense carries a wide variety of products in addition to apparel -- is able to attract shoppers of all tastes and grow its business in any economic environment. Target is doing what it can to catch Wal-Mart, but concerns regarding the credit quality of its customers have tempered its recent growth.

Nordstrom shows that while growth in the retail sector doesn't come cheap (with price-to-book ratio of 5), luxury buyers are willing to step up and spend even in the face of economic weakness. Even Macy's, which does show a dip in total sales over the five-year period, has consistently grown same-store sales in recent months and has cornered the mall-based mid-tier price point between J.C. Penney and Nordstrom.

J.C. Penney might be the cheapest on a book value basis, but its sales have been trending almost constantly lower since 2007 and its cash flow has shrunk dramatically. Cutting its dividend out of the equation saves the company $175 million annually, but comparatively, it's no better value than any of its peers based on these metrics.

What's next

Now for the $64,000 question: What's next for J.C. Penney? The answer is going to depend on whether Ron Johnson's actions can get consumers back into the stores again, if its new pricing strategy can be conveyed in an easy-to-understand manner, and if it can ultimately control its expenses as sales continue to fall while the new plans are implemented.

Our very own CAPS community gives the company a dreaded one-star rating (out of five), with 30.1% of members expecting it to underperform. Although I've yet to make a CAPScall on J.C. Penney in either direction, I've mentioned on a few occasions that I'd lean more toward an outperform call than an underperform call merely because of Ron Johnson's presence.

The key thing to remember here is that turnarounds take time and they are often unpredictable. We saw that last quarter with sales crashing through the floor. Ultimately sales will find a floor and customers will acclimate to Penney's new pricing strategy which should produce steadier and healthier margins. I'm not saying J.C. Penney may not head lower from its current levels, as there's little in the way of good news to support the stock, but I've also learned that Ron Johnson is an innovator I dare not bet against over the long run.

Even if J.C. Penney isn't the right investment for you, you might be interested in reading about three companies our analysts at Stock Advisor feel will outperform in the emerging markets. Get your copy of this latest free special report by clicking here.

Craving more input on J.C. Penney? Start by adding it to your free and personalized watchlist. It's a free service from The Motley Fool to keep you up to date on the stocks you care about most.

At the time thisarticle was published Fool contributor Sean Williams has no material interest in any companies mentioned in this article. You can follow him on CAPS under the screen name TMFUltraLong, track every pick he makes under the screen name TrackUltraLong, and check him out on Twitter, where he goes by the handle @TMFUltraLong.The Motley Fool owns shares of Apple. Motley Fool newsletter services have recommended buying shares of Apple, as well as creating a bull call spread position in Apple and a diagonal call position in Wal-Mart. Try any of our Foolish newsletter services free for 30 days. We Fools don't all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.

Copyright © 1995 - 2012 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.