What Lululemon's Downward Dog Position Means for Shareholders

Shares of lululemon athletica (NAS: LULU) fell more than 13% in intraday trading Thursday, despite the retailer beating expectations for its first quarter. Unfortunately, the company's weak forecast for the current quarter stole the spotlight and pushed the stock lower. Let's take a deeper look at what's causing the disparity, and whether shareholders should be concerned.

Solid growth

The luxury sports apparel company rang in its fiscal first quarter with a 40% increase in profit from the year-ago period, beating the Street's estimates on both the top and bottom lines. Earnings per share clocked in at $0.32 on net income of $46.6 million, which is up from $0.23 a share in 2011. Meanwhile, analysts were expecting earnings of just $0.30 a share. This marked the fourth straight quarter in which Lululemon rocked analyst estimates.

The retailer's e-commerce sales are even more impressive. Revenue from the company's direct-to-consumer channel soared 179% to $38.4 million, or 13.5% of total income in the period. That's a significant improvement from 7.4% of total revenue in the same quarter a year ago. Rival athletic apparel company Under Armour (NYS: UA) only wishes it could grow online sales at that rate. However, it has still put up big numbers and its net revenues from direct-to-consumer business grew 49% year-over-year.

Additionally, Lululemon continues to improve the online shopping experience for its customers by offering free shipping on any item, anytime. It's initiatives like this that will push the company's e-commerce sales higher in coming quarters.

Not only is Lululemon growing its online business, it's also expanding overseas. The company opened new stores in Australia and New Zealand, finishing the first quarter with 180 corporate-owned retail stores throughout North America, Australia, and New Zealand. International locations are crucial long-term growth drivers as only 4% of the company's net revenue was generated from sales outside of North America.

Lululemon plans to build the brand's presence in Hong Kong later this year, in addition to new showrooms in London. Yet even with management's global growth strategy now under way, the brand still has plenty of room to run.

Downward dog

There are plenty of positives in the company's latest earnings report, but it's management's less-than-record-shattering projections that are getting the attention. The company expects net revenue of between $273 million and $278 million for its second quarter, and EPS of $0.30. Analysts polled by Reuters are looking for revenue of $290 million and earnings of $0.33 a share.

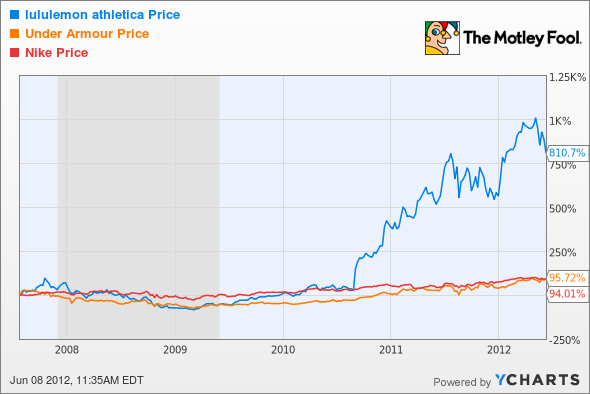

The stock took a hit on the news, but I think this is a short-lived setback in the stock price. Shares are still up more than 68% this year. Meanwhile, industry peers don't come close in terms of price performance.

Lulu's quarterly revenue growth of 51% is far more appealing than Nike's (NYS: NKE) 15% year-over-year growth. The yogi also trumps rivals on the cash flow front. Lululemon boasts a debt-free balance sheet with more than $400 million in cash. That's much healthier than Under Armour, which has nearly $76 million in debt on the books and negative free cash flow over the last 12 months.

Unlike Nike and Under Armour, Lululemon doesn't sell its merchandise in department stores like Dick's Sporting Goods. This vertical retail strategy is one reason why Lululemon's margins more than double those of Nike and Under Armour.

Thinking to the future

This is a company that's known for being cautious with its outlooks. Given the stock's performance to-date, I don't think Lululemon will have any problems beating management's conservative guidance this year. From increased sales in its direct-to-consumer business to new international store openings and fresh product categories like cycling and swim, I'm confident in the company's ability to grow profits.

True, the stock isn't cheap at 50 times earnings. But the niche retailer is doing too many things right to discount it on P/E alone. Lululemon remains focused on product innovation, and consumers are willing to pay a premium for its merchandise. The addition of men's clothing and a new girl's line of dance apparel, known as ivivva, has helped the company win the hearts of new customers. I'm in this stock for the long run and plan on adding to my position if shares continue to dip lower.

Lululemon is a quality business with a cult-like following and visionary leadership in CEO Christine Day. I have no doubt the stock will surge higher in the coming year. If you're not ready to buy the stock, I encourage you to instead add Lululemon to My Watchlist, The Motley Fool's free tool that lets you track and monitor your favorite companies.

Add Under Armour to My Watchlist.

Add Nike to My Watchlist.

At the time thisarticle was published Fool contributor Tamara Rutter owns shares of Lululemon. Follow her onTwitter, where she uses the handle:@TamaraRutter, for more Foolish insights and investing advice.The Motley Fool owns shares of lululemon athletica and Under Armour.Motley Fool newsletter serviceshave recommended buying shares of Nike, Under Armour, and lululemon athletica.Motley Fool newsletter serviceshave recommended creating a bear put spread position in Under Armour.Motley Fool newsletter serviceshave recommended creating a diagonal call position in Nike. The Motley Fool has adisclosure policy. We Fools may not all hold the same opinions, but we all believe thatconsidering a diverse range of insightsmakes us better investors. Try any of our Foolish newsletter servicesfree for 30 days.

Copyright © 1995 - 2012 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.