At a 52-Week High, Is AT&T Still a Great Buy?

Shares of AT&T (NYS: T) hit a 52-week high on Thursday. Let's take a look at how it got there and see if clear skies are still in the forecast.

How it got here

During turbulent economic times, stocks that maintain slow-but-steady growth and have high-demand, inelastic price point products are going to do well. The United States' two largest national carriers, AT&T and Verizon (NYS: VZ) , are perfect examples of this.

AT&T's latest quarterly report demonstrated weak contract growth of just 186,000 additional subscribers (thanks mainly to iPad sales), but did show marked growth in average revenue per user, a key metric for mobile providers that demonstrates customers are willing to pay more for the services they're signing up for. In the first-quarter, AT&T noted a 19.9% increase in wireless data revenue as more users gravitated toward higher-end data plans. As smartphones continue to gain in popularity and prices become more reasonable, it's quite reasonable to expect AT&T's ARPU figures will rise as subscribers opt for high-tiered data plans.

As you might expect, AT&T won't have a cakewalk because of increased competition, despite being the nation's No. 2 carrier. Verizon currently has next-generation 4G LTE coverage in 230 markets, compared to AT&T's 35, and hopes it can lure customers into higher-margin data plans with its infrastructure build-out.

Also, the dominance of Apple's (NAS: AAPL) iPhone has been a key component to the mobile sectors growth. Although most vendors take a margin hit by bringing the iPhone into their network, the sheer volume of customers it brings in, and the data plans they buy, makes up for the smaller margin. This is exactly why No. 3 carrier Sprint Nextel (NYS: S) pushed for so long to get the iPhone into its network and why pre-paid, no-contract service provider Leap Wireless (NAS: LEAP) is excited to offer the iPhone through its Cricket service.

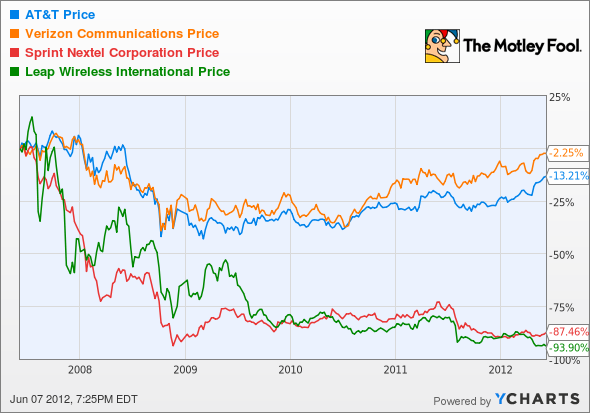

How it stacks up

Let's see how AT&T stacks up next to its peers:

Now that's what I call a sector bifurcation! Continuing losses and slow subscriber growth has both Sprint and Leap Wireless on the ropes with investors.

Company | Price/Book | Price/Cash Flow | Forward P/E | Dividend Yield |

|---|---|---|---|---|

AT&T | 1.9 | 5.9 | 13.4 | 5.1% |

Verizon | 3.2 | 3.9 | 14.9 | 4.8% |

Sprint Nextel | 0.8 | 2.2 | N/M | 0% |

Leap Wireless | 0.8 | 1.1 | N/M | 0% |

Source: Morningstar. Yields are projected. N/M = not meaningful.

As the chart indicates, this is essentially a two-horse race between AT&T and Verizon. Sprint Nextel has been crushed by its parasitic partnership with Clearwire, which could wind up costing it in excess of $2 billion. Leap, on the other hand, may actually be in worse shape than Sprint since it's been burning cash on a free cash flow basis for six straight years. It simply can't compete with the infrastructure and marketing budget of AT&T or Verizon.

The differences between AT&T and Verizon are very subtle. Verizon's 4G LTE rollout should offer greater high-speed mobile coverage and will probably lead to a marginally faster growth rate than AT&T. However, AT&T's dividend is slightly higher than Verizon's and, in its latest quarter, it sold a clean one million more iPhones than its counterpart, Verizon. Those iPhones are the key to driving long-term customer loyalty, yet both appear to be solid buys with strong cash flow generation.

What's next

Now for the $64,000 question: What's next for AT&T? That question is going to depend on whether it can continue to increase its ARPU in light of Verizon's advanced 4G LTE network and if it can continue to outpace Verizon in iPhone sales which are crucial to driving higher-margin data plans in the long run.

Our very own CAPS community gives the company a three-star rating (out of five), with 92.3% of the 5,810 members expecting it to outperform. Count me among the vast majority who have made a CAPScall of outperform on AT&T. I find myself currently up 15 points on that call and with no reason to close it.

AT&T is a dominant player in mobile that isn't going to gain or cede much market share from any of its competitors and remains the vendor of choice for users who want the Apple iPhone. It still has plenty of opportunities to convert lower-cost plans into higher-paying customers as smartphones grow even cheaper, which should ultimately increase its ARPU. There's little reason to believe AT&T's dividend is at risk of falling given its strong cash flow generation and I feel it remains one of the best quality "safe investments" you can buy.

Unlike the carriers, who have a love-hate relationship with Apple given the massive subsidies they pay, investors absolutely love the company. It's easy to understand given the stock's incredible past performance. Whether you own Apple or not, our senior technology analyst doesn't think it's too late to participate in more gains, and he explains his stance in this premium research report on Apple. While the report costs less than a single stock trade, its insight might lead to one of your best trades ever.

If you'd rather get the inside scoop on three more companies set to take advantage of the next technological revolution, click here to read our feature report on the mobile revolution - absolutely free of charge.

Craving more input on AT&T? Start by adding it to your free and personalized watchlist. It's a free service from The Motley Fool to keep you up to date on the stocks you care about most.

At the time thisarticle was published Fool contributor Sean Williams has no material interest in any companies mentioned in this article. You can follow him on CAPS under the screen name TMFUltraLong, track every pick he makes under the screen name TrackUltraLong, and check him out on Twitter, where he goes by the handle @TMFUltraLong.The Motley Fool owns shares of Apple. Motley Fool newsletter services have recommended buying shares of, and creating a bull call spread position in, Apple. Try any of our Foolish newsletter services free for 30 days. We Fools don't all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.

Copyright © 1995 - 2012 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.