The Not-So-Private Equity Swindle

Over the past three years, the private equity industry has decided to eschew its handle and go public. Although their motives for doing so are questionable, one thing isn't: Investors who looked to these offerings as an opportunity to piggyback off the new kings of capital have been sorely disappointed. The shares in all but one have decreased in value markedly, and none have beaten the broader market.

Some things are best kept private

If we learned only one thing from the Facebook IPO debacle, it was this: If you're not entitled to an initial allocation -- the purchase of shares generally by institutional investors and typically on the evening prior to listing -- don't buy stock in a newly debuting company unless you're looking to offset a positive capital gain with a loss.

Investment bankers on Wall Street purportedly rigged the process to ensure that retail investors would lose out. And they did. To date, shares in the social media giant are down 36% after opening two weeks ago at $42.

Although I'm not aware of similar allegations concerning the IPO process of now-public private equity firms, the evidence certainly suggests a pattern.

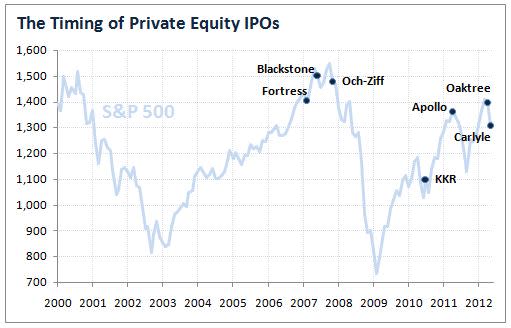

Of the seven largest buyout firms to go public since 2007, all but one, Kohlberg Kravis Roberts (NYS: KKR) , have seen the value of their shares decline markedly from their opening price.

Fortress Investment Group (NYS: FIG) leads the charge with a 91% loss, followed by Och-Ziff Capital Management (NYS: OZM) with a 78% decline, and rounding out the top three is The Blackstone Group (NYS: BX) , which has seen its shares decline by nearly 66% over the last five years.

To be fair, as you can see in the chart below, all three of these companies went public at the worst possible time, just as the housing bubble was about to burst. The three most recent filers -- Apollo Global Management (NYS: APO) , Oaktree Capital Group, and The Carlyle Group -- are only down by an average of 15%, largely weighed down by Apollo, which has declined by 36% since going public in April of last year.

Source: Yahoo! Finance.

The problem with this excuse, however, is that every single private equity company that's gone public in the past few years has underperformed the broader market.

Take the three companies just mentioned -- Fortress, Och-Ziff, and Blackstone -- they've lagged behind the S&P 500 by 85, 67, and 53 percentage points, respectively. And on average, the industry itself has lagged by nearly 35 percentage points.

Company | Total Aftermarket Return Since IPO* | Return for Initial Allocation | Relative to S&P 500 (percentage points) |

|---|---|---|---|

Fortress Investment Group | (91%) | 89% | (85) |

Och-Ziff Capital Management | (78%) | 2% | (67) |

The Blackstone Group | (66%) | 18% | (53) |

Average | (38%) | 16% | (35) |

Apollo Global Management | (36%) | (2%) | (32) |

Oaktree Capital Group | (8%) | (5%) | (2) |

The Carlyle Group | (3%) | 0% | (3) |

Kohlberg Kravis Roberts | 14% | 11% | (5) |

Source: Yahoo! Finance, author's calculations. *The total aftermarket return uses the opening share price on the first day of trading, as opposed to the IPO price.

Fool me once, shame on you

Now I know what you're probably thinking: Here John goes again with one of his crazy conspiracy theories.

Well, call it what you will, but the reality is that the average investor of an initial allocation in a private equity IPO would have reaped a nearly 16% gain on their investment by selling at the opening price. This beats the average aftermarket return by a whopping 53 percentage points.

In other words, just like the Facebook IPO, the only thing left over for investors like you and me is the proverbial slop.

If you're tired of moseying up to the trough to get your daily serving of slop, courtesy of our investment banking friends on Wall Street, then check out our recent free report about stocks only the smartest investors are buying. Among others, it profiles two companies that Warren Buffett either is, or would have been, interested in adding to his portfolio. To access this free report, and learn the identity of these two stocks, click here now.

At the time thisarticle was published Fool contributor John Maxfield does not have a financial position in any of the companies mentioned above. The Motley Fool owns shares of Facebook. The Motley Fool has a disclosure policy. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. Try any of our Foolish newsletter services free for 30 days.

Copyright © 1995 - 2012 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.