Here We Go Again: The Dow Is Diving!

Today's upswing notwithstanding, it's ugly out there. Since early May, the S&P 500 (INDEX: ^GSPC) has fallen 9%, while the Dow Jones Industrial Average (INDEX: ^DJI) has fallen nearly as much.

On the one hand, it all seems so immediate and fresh -- Europe is in crisis, the U.S. is sluggish, and even Brazil, Russia, India, and China are slowing. No wonder investors are getting carpal tunnel from hitting the "sell" button.

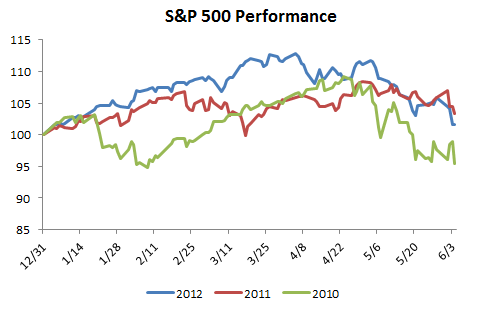

Yet, at the same time, this all feels so familiar. Take a look at the performance of the S&P from January through June in each of the past three years:

Sources: Yahoo! Finance and author's calculations.

I try my best to avoid seeing patterns where they don't exist, but that seems pretty hard to miss.

But it's not just that. Try this on for size:

Even if Greece and other troubled economies remain in the eurozone, the overall health of the zone could remain compromised for years. Greece could take a long time to scrape through its financial crisis and may need even more help.

Sound like current events? That's from June of 2010. Or how about this:

The European Central Bank is "looking increasingly vulnerable" and may face "hefty losses" as a result of propping up indebted eurozone countries, a leading think-tank has warned.

That's also from June, but this time 2011.

What I can't help but wonder is this: Is our three-year-running summertime freak-out over the eurozone the driver of falling stocks, or are falling stocks the driver of our increased concern about Europe?

My fellow Fool Alex Dumortier recently explained that for most investors it makes more sense to simply buy and hold rather than try to follow the Wall Street cliche of "sell in May and go away." But at the same time, the data Alex presented showed that between May and October, stocks tend to underperform the October-to-May stretch.

Signal or noise?

The danger here is that many pundits and so-called "market experts" see the stock market as a source of information. That is, they claim that if the stock market is falling, then we're getting a signal from the all-knowing markets that something is going wrong.

But as Nassim Taleb points out in his new book Antifragile (hat tip to Farnam Street blog for the excerpt), it's all too easy to take in a glut of data and assume that you're getting proportionately more signal, when what you're really getting is far more noise. Taleb writes:

The more frequently you look at data, the more noise you are disproportionally likely to get (rather than the valuable part called the signal); hence the higher the noise to signal ratio. ... Say you look at information on a yearly basis, for stock prices or the fertilizer sales of your father-in-law's factory, or inflation numbers in Vladivostock. Assume further that for what you are observing, at the yearly frequency the ratio of signal to noise is about one to one (say half noise, half signal) -- it means that about half of changes are real improvements or degradations, the other half comes from randomness. This ratio is what you get from yearly observations. But if you look at the very same data on a daily basis, the composition would change to 95% noise, 5% signal. And if you observe data on an hourly basis, as people immersed in the news and markets price variations do, the split becomes 99.5% noise to .5% signal. That is two hundred times more noise than signal -- which is why anyone who listens to news (except when very, very significant events take place) is one step below sucker.

Or, to put it in individual stock terms, Intel (NAS: INTC) is up 1.5% as I write this. There may be some bit of news somewhere that I could connect to that 1.5% rise and claim that today's move is meaningful. But dollars to donuts the change in Intel's stock price today is completely meaningless -- it's noise. On the other hand, if I look at the stock price today, and I look at it again a year from now, or five years from now, the change is likely to be much more meaningful and driven in large part by the company's chip-development efforts, the broad economy, etc.

Back to Europe

So what are we fretting about today? Are we worried that the eurozone problems are deepening and we're therefore selling stocks? Or are we selling stocks -- as is wont to happen in the summer -- and ascribing that seasonal phenomenon to Europe's woes?

Considering that the eurozone's problems have been going on for years and we've seen this June escalation in each of the past three years, I don't think it'd be nuts to think we've got some tail wagging the dog here.

So what do we do? It's tempting to look back to recent history to see if the post-June performance provides a guide. Unfortunately, it's not terribly helpful.

Sources: Yahoo! Finance and author's calculations.

The S&P whipped back in 2010, but performed poorly last year.

A better takeaway is a combination of Alex's breakdown of the "sell in May" saw and Taleb's caution about noise. We're fortunate to live in an era that puts a wealth of information and data at our fingertips, but we're also cursed to live in an era that puts a wealth of information and data at our fingertips. In a system as large and complex as the global economy, the overwhelming majority of what we're getting on a day-to-day or even month-to-month basis is noise.

For investors, it all comes back to the basics: Find good companies, buy at the right price, and be an owner over long periods of time.

Looking for ideas on which stocks to own? These nine dividend-payers are a great place to start.

At the time thisarticle was published Motley Fool newsletter services have recommended buying shares of Intel. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. Try any of our Foolish newsletter services free for 30 days.Fool contributor Matt Koppenheffer owns shares of Intel, but does not have a financial interest in any of the other companies mentioned. You can check out what Matt is keeping an eye on by visiting his CAPS portfolio, or you can follow Matt on Twitter @KoppTheFool or Facebook. The Fool's disclosure policy prefers dividends over a sharp stick in the eye.

Copyright © 1995 - 2012 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.