Analysts Debate: Is IMAX a Top Stock?

The Motley Fool has been making successful stock picks for many years, but we don't always agree on what a great stock looks like. That's what makes us "motley," and it's one of our core values. We can disagree respectfully, as we often do. Investors do better when they share their knowledge.

In that spirit, we three Fools have banded together to find the market's best and worst stocks, which we'll rate on The Motley Fool's CAPS system as outperformers or underperformers. We'll be accountable for every pick based on the sum of our knowledge and the balance of our decisions. Today, we'll be discussing IMAX (NYS: IMAX) , the big-screen theater company.

IMAX by the numbers

Here's a quick snapshot of the company's most important numbers.

Statistic | Result (Most Recent Available) |

|---|---|

Revenue | $243 Million |

Net Income | $19.1 Million |

Number of Commercial Theaters | 510 |

Market Cap | $1.3 Billion |

Key 2012 Titles | The Avengers, The Amazing Spider-Man, The Dark Knight Rises |

Key Competitors | RealD (NYS: RLD) |

Sources: Yahoo! Finance and company press releases.

IMAX either sells its equipment to movie theater companies or enters into a joint venture, which involves lending equipment to the theater for a percentage of the box office, and sometimes a cut of popcorn sales. On the studio side, IMAX takes a cut from the box office of each film it converts into IMAX and shows on the big screen.

Travis' take

The evolution of IMAX from a small niche player in the theater market to a global brand has been fast and furious, and over the past five years, investors have been rewarded with a rising stock price.

After a miserable 2011 at the box office, companies such as IMAX and RealD have become forgotten commodities in the entertainment industry. But with IMAX's stock price down and a summer of blockbuster hits upon us, I think it's time to jump back in.

The heart of IMAX's performance is tied directly to blockbuster action films, something the company is starting to put into action. I'm talking about releases such as Mission: Impossible, Batman, Tron, and Avatar. It's these films that make IMAX what it is and drives the company's financial performance, because costs to convert a film into IMAX are relatively fixed, so a movie's performance is leveraged on the upside.

Also leveraged is IMAX's theater growth, particularly expansion internationally. Since 2008, the company has grown from 210 theaters to 510, and by the end of 2012, that figure could be as high as 594. The most exciting growth is in China, where theaters average 12.5 times the box office of other screens. In a country where there are more than 1 billion people and the middle class is growing, the opportunity is huge.

I'm not usually crazy about a company that has a $1.3 billion market cap and only $19.1 million in net income in the past 12 months, but in the case of IMAX I think profits will explode this summer. The pipeline of movies is strong, and if The Avengers' $21.4 million opening weekend in IMAX is any indication, the big screen is commanding a big audience.

I'm a longtime shareholder, and I'm more than willing to give an outperform call at the current share price. IMAX has too much upside to overlook, and with expansion moving along quickly in China and a strong slate of movies, I think the stock will quickly move higher.

Sean's take

Oh, how I loathe the majority of entertainment-based stocks -- and IMAX is no different. As Travis points out, IMAX has done wonders with expanding its global network of theaters, and it has taken advantage of a recent surge in strong movie debuts, but there are plenty of reasons I'd rather throw popcorn at a stock that gets a portion of ticket sales than go near it with my own money.

For starters, movie ticket sale trends are terrible!

Source: The-Numbers.com.

*Annualized estimate.

With the exception of 2006 and 2009, total ticket sales have been on a precipitous decline since 2002 and have been buoyed only by the rising price of movie admission. But even that figure that has been weak, with total ticket revenue rising from $9.19 billion in 2002 to an annualized estimate of just $10.17 billion in 2012 (a 1% annualized increase) according to movie data website The-Numbers.com. This could turn out to be bad news for movie theaters, given that wage growth is being outpaced by inflation, which, in turn, could mean a perpetuation of the trend of fewer moviegoers.

Also playing into this trend is the increasing demand for digital content at home. Cable companies and on-demand rental services are wising up to consumers' needs for movies at a reasonable price. We're seeing this translate into huge capital investments from Comcast (NAS: CMCSA) and Netflix (NAS: NFLX) in an attempt to draw consumers away from the theater and keep them in the comfort of their own home. This represents a viable threat, as it's both cheaper and more convenient than heading to the local theater.

For IMAX in particular, I have to wonder what it's going to take for the company to turn a reasonable profit, especially with movie trends not in their favor despite the network expansion. If you're thinking to yourself, "The Avengers and Hunger Games are enough to turn IMAX's fortunes around," then you've essentially proved my next point that movie blockbusters are few and far between. A movie production company like Disney (NYS: DIS) can produce an epic flop like John Carter and still redeem itself (and then some) with game-changers like Marvel's The Avengers. Movie theaters don't have that luxury and are practically obligated to share screen space among all types of movies, both blockbusters and flops.

The movie industry is far too hit-and-miss, and movie ticket sale trends way too bearish, to consider IMAX a buy at these levels.

Alex's take

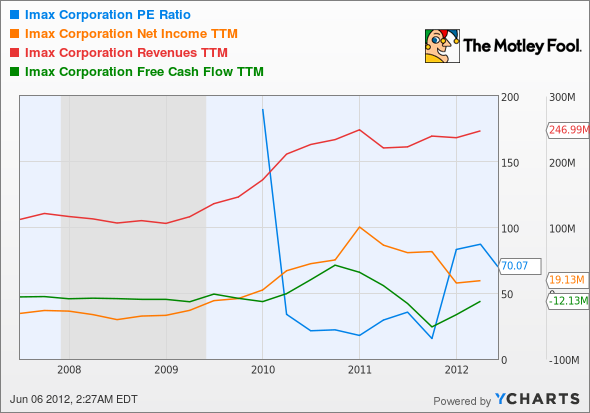

Before I get buried in analysis, I'd like to open with a nice, quick chart of IMAX's recent history:

IMAX P/E Ratio data by YCharts

Here's how to read this chart: IMAX has seen fairly steady revenue growth over the past five years, but net income and free cash flow growth stalled out at the end of 2011. The trend seems to finally be reversing, but lower net income combined with a stronger bottom line pushed IMAX's valuation to some of its highest levels since becoming profitable.

That valuation element is important, but it may not be as critical as you think -- the rest of the year will see some hotly anticipated blockbusters show up on IMAX's bottom line. The Avengersdrew $15 million domestically on IMAX screens during its opening weekend. That superhero extravaganza is followed this summer by The Amazing Spider-Man, Men in Black III, The Dark Knight Rises, and Prometheus, with Skyfall and The Hobbit landing in the winter. That's a list to make action fans geek out.

If, as Travis says, IMAX is keyed into the need to push tentpole pictures for longer periods, 2012 could be a big turnaround year. But, as Sean also mentions, blockbusters can be few and far between. That's a longer-term worry, but 2012 has that problem handled.

I'm not as concerned as Sean over a slow decline in ticket sales. As I've shown before, total box office revenues have stayed stable for years, and value-added experiences like IMAX screens and RealD 3-D has helped drive that. In fact, 2012 and 2013 could be big for IMAX because of mounting economic fears. You'll note that Sean's graph shows an uptick in ticket sales in 2009. The difference between an IMAX ticket and a standard one is very small, and people need escapes during tough times. There's no substitute for the big-screen experience, despite the wealth of options Netflix might offer at home.

I think 2012 will be a strong year for IMAX and will reverse its 2011 trend, thanks to a better slate and a larger international presence. Movies are recession-proof, which makes this one stock I like for these strange times. I'd like to revisit my call at the end of the year, but for the time being I have no qualms about calling this an outperformer for 2012.

The final call

Despite Sean's objections, we'll give IMAX an outperform rating on our TMFYoungGuns CAPS portfolio, where we've tracked the picks we've made in this series.

Speaking of our picks, overall our eight picks have outperformed by 63 points, and we've decided to cash in some chips by closing out our underperform call on Zynga after beating the market by more than 44 points. An underperform call has only so much upside, and we think the juice has been squeezed from this pick.

At the time thisarticle was published Fool contributor Travis Hoium owns shares of IMAX and Disney. Alex Planes, and Sean Williams have no positions in any companies mentioned. You can follow Travis on Twitter at@FlushDrawFool, Sean at@TMFUltraLong, and Alex at@TMFBiggles.The Motley Fool owns shares of Walt Disney and Netflix.Motley Fool newsletter serviceshave recommended buying shares of IMAX, Walt Disney, and Netflix. The Motley Fool has adisclosure policy. We Fools don't all hold the same opinions, but we all believe thatconsidering a diverse range of insightsmakes us better investors. Try any of our Foolish newsletter servicesfree for 30 days.

Copyright © 1995 - 2012 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.