Will iRobot Dream of Big Returns After Its 52-Week Low?

Shares of iRobot (NAS: IRBT) hit a 52-week low Friday. Let's take a look at how the company got there to find out whether cloudy skies remain on the horizon.

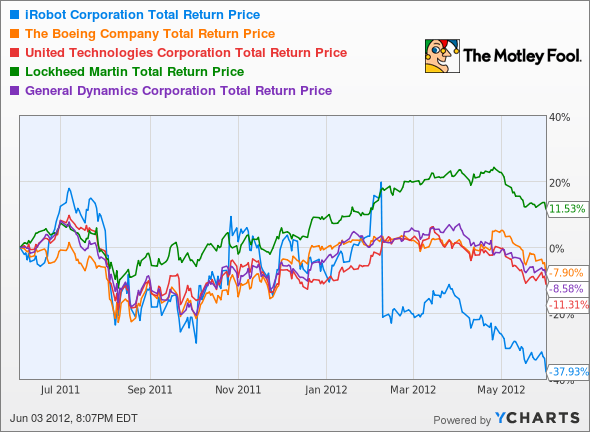

How it got here

One big dent in iRobot's armor came after it released disappointing forward guidance for 2012. Investors have been wary of the robot maker since then, although the trend over the past two months isn't much different than many of its defense peers:

IRBT Total Return Price data by YCharts

It's important to remember, though, that iRobot is a much smaller company than most defense-oriented manufacturers. It takes Boeing (NYS: BA) about two days to earn the revenue iRobot generates in a full year, and it (along with the other notable competitors) has a much more diversified military product lineup.

iRobot's defense backlog also dwindled in 2012, which was an ominous sign for shareholders. Anyone following America's ongoing conflicts shouldn't be surprised. The war effort is effectively over in Iraq and winding down in Afghanistan, and the military's favored patrol 'bots now seem to be of the aerial variety.

What you need to know

Despite the big drop, iRobot still commands a higher valuation than its peers, although its net margin is right in line with most of them:

Company | P/E Ratio | 3-Year Annualized Earnings Growth | Net Margin (TTM) |

|---|---|---|---|

iRobot | 16.7 | 123.9% | 7.3% |

Boeing | 11.6 | 28.1% | 6.0% |

Lockheed Martin (NYS: LMT) | 9.7 | (4.0%) | 5.9% |

General Dynamics (NYS: GD) | 9.2 | (0.1)% | 7.6% |

Northrop Grumman (NYS: NOC) | 7.5 | 5.5% | 8.1% |

Source: Yahoo! Finance, S&P Capital IQ.

The company's first-quarter earnings barely avoided going negative, and full-year numbers might still wind up splashed with red ink, as guidance projected in the fourth quarter. It may be iRobot's Roomba-led consumer segment keeping it afloat, since the broader defense sector has some valuations barely over half of the robot maker's.

Defense contracts were about a third of iRobot's revenue last year and will almost certainly be less this year. That's a lower percentage than its competitors:

Company | Percent of 2011 Revenue From Defense |

|---|---|

Boeing | 47% |

Lockheed Martin | 82%* |

General Dynamics | 69%* |

Northrop Grumman | 91% |

Sources: Corporate 10-K filings. *Does not include international military orders.

Considering the huge defense cuts set for 2013, a lower reliance on Uncle Sam may be the only thing keeping iRobot from shrinking further -- but that may very well happen anyway if a slowdown occurs in the company's key consumer markets. Things don't look very good for iRobot at the moment.

What's next?

Where does iRobot go from here? I wouldn't bet on a big military boost in the near future, so it may be up to the Roombas (and any other nifty robotic helpers the company comes up with) to carry the day. The Motley Fool's CAPS community is still bullish -- or is that bot-ish -- on iRobot. The company earned a four-star rating just after its big drop and has kept that high esteem since. Count me among those bot bulls. I placed an outperform call on iRobot last fall, and plan to keep it for the long term. I do mean long term, since it's hard to see the company making back its losses this year.

Interested in tracking this stock as it continues on its path? Add iRobot to your watchlist now for all the news we Fools can find, delivered to your inbox as it happens. If you're looking to invest in other companies transforming modern life, The Motley Fool has some great ideas in our latest free report. Find out more about the three stocks to own for the new industrial revolution -- click here to get your free information while it's still available.

At the time thisarticle was published Fool contributor Alex Planes holds no financial position in any company mentioned here. Add him on Google+ or follow him on Twitter @TMFBiggles for more news and insights. The Motley Fool owns shares of Lockheed Martin, Northrop Grumman, and General Dynamics. Motley Fool newsletter services have recommended buying shares of iRobot. The Motley Fool has a disclosure policy. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. Try any of our Foolish newsletter services free for 30 days.

Copyright © 1995 - 2012 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.