Facebook Won't Break the Law of Large Numbers

Want to know how valuable Facebook (NAS: FB) will be? First you'll need to know how many people with an Internet connection also have a Facebook account. Knowing the "Facebook ratio" won't be enough, though. There are many ways to evaluate Facebook's potential, beginning with its user base and ending with the profit it can generate from each user. The big picture might not be as bright as the Face-bulls claim -- but it may surprise Zucker-bears, too. Let's dig deep to uncover something interesting.

Warning: numbers ahead

Facebook is the second-most-visited site in the world, at 4.8 billion uniquely tracked visits per month. Google (NAS: GOOG) is the king of clicks, with 6.2 billion unique monthly views -- and that doesn't count its YouTube subsidiary (the world's third-most visited site in its own right). Google commands just more than two-thirds of all search engine use today. Yahoo! (NAS: YHOO) , the one-time search king, held a bit over half of the search market at the turn of the century.

That's a solid baseline for us to start from. Search has always been a free, ad-supported business model, which happens to be Facebook's preferred business model as well. Let's see how Facebook really stacks up, using monthly active users to find that "Facebook ratio" I mentioned earlier.

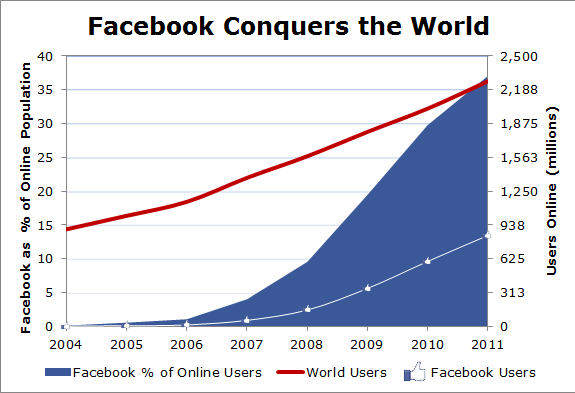

Sources: World Bank; Internet World Stats; Ben Foster; author's calculations.

As you can see, Facebook's growth quickly outpaced the growth of the global online user base. Keep in mind that this only tracks users to the end of 2011, and the ratio might now be a bit higher than the 37% it stood at last December. That's an impressive ratio, but Facebook isn't big everywhere. In fact, there's one country where it's nonexistent -- China. It's easy enough to fix our numbers to account for the Middle Kingdom's Face-block, so let's take a look at the new ratio:

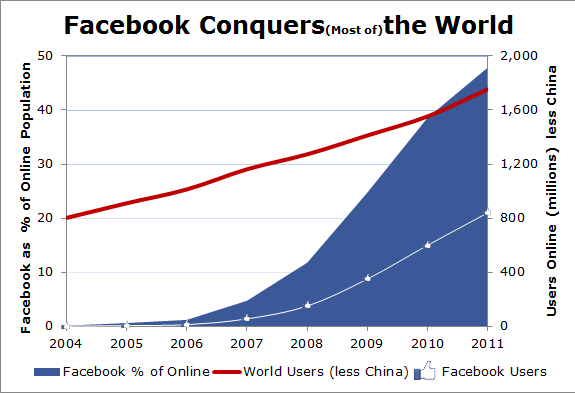

Sources: World Bank; Internet World Stats; Ben Foster; author's calculations.

That's pretty impressive, isn't it? Facebook's use in the world (minus China) is 48%, near Yahoo!'s previous percentage peak and most of the way to Google's dominant position. Now that we've gotten here, we can use these numbers to figure out how big Facebook could get -- and how quickly. It's safe to ignore China as a source of growth for now, as its control-obsessed government isn't likely to relax enough for Facebook to get a foothold.

Present possibilities and future potential

Understanding Facebook's growth potential requires some more numbers. Don't worry -- there's a quick refresher course at the end.

Facebook's user growth has obviously slowed down as it has gained in size. It's a lot easier to add users when you only have a million of them than it is when you have 900 million. Facebook still grew its user base by about 40% from 2010 to 2011, and it might gain at least 20% more users over the course of this year. That's a much faster clip than the typical annual increase in global connectivity:

Year | Global Online Year-Over-Year User Growth | Global (less China) Online Year-Over-Year User Growth | Facebook Year-Over-Year User Growth |

|---|---|---|---|

2005 | 13.9% | 13.5% | 450.0% |

2006 | 12.6% | 11.2% | 118.2% |

2007 | 19.3% | 14.7% | 358.3% |

2008 | 14.5% | 9.5% | 172.7% |

2009 | 14.3% | 11.0% | 133.3% |

2010 | 12.0% | 10.0% | 71.4% |

2011 | 12.6% | 12.9% | 40.0% |

Sources: World Bank; Internet World Stats; Ben Foster; author's calculations.

China has helped drive global user growth, but that effect reversed in 2011. Still, both global growth and global-less-China growth have been relatively consistent over Facebook's lifetime.

If two of every three non-Chinese online users were on Facebook today, it could boast 1.2 billion monthly active users. But Facebook won't need 40% growth rates to get to the Google ratio. Increasing its user base by 20% a year will bring two-thirds of the non-Chinese connected global populace to Facebook by 2016, assuming global growth trends remain the same as they have over the past few years:

Year | Global (less China) Online Users | Total Facebook Users, Assuming Stable Growth Rate (remains at 48% of global total) | Total Facebook Users, Assuming 20% Annual Growth Rate / Percent of Total Global Users |

|---|---|---|---|

2012 | 1,958 million | 940 million | 1,008 million / 52% |

2013 | 2,185 million | 1,049 million | 1,210 million / 55% |

2014 | 2,438 million | 1,170 million | 1,452 million / 60% |

2015 | 2,721 million | 1,306 million | 1,741 million / 64% |

2016 | 3,037 million | 1,458 million | 2,090 million / 69% |

Source: Author's calculations. Hypothetical use only.

Facebook made about $1.19 in profit per monthly active user last year. Its annual revenue per user dropped in the most recent quarter, but as Evan Niu's graphs point out, revenue tends to drops slightly in the first quarter. Let's give Zuckerberg the benefit of the doubt. If earning potential stays as it was in 2011 and Facebook keeps growing, the company ought to generate between $1.74 billion and $2.49 billion in profit, depending on whether it grows in step with the Internet user base or at a faster rate.

I don't "like" this result

Many people have attempted to assess Facebook's future using a variety of numbers. Fellow Fool Anders Bylund went at it with a discounted cash flow analysis and found that only a very lofty growth rate -- even higher than my optimistic 20% annual user growth rate -- would justify its current price. Alex Dumortier, one of the Fool's biggest Facebook bears, has pointed out that Facebook's valuation offers it, at best, room to double if it is to reach a Google-sized market cap.

I won't try to convince you to trust these estimates. There's so much that could change between now and 2016. Facebook could effectively monetize its massive mobile user base and grow its profit per user, or mobile could be its downfall. Payments from Zynga's (NAS: ZNGA) millions of players could keep growing rapidly. Payments could also wither if the 2% of Zynga's user base that pays to play decides it has better things to buy than virtual cabbages. But here's what I know: If Facebook keeps growing and remains profitable, but doesn't find lucrative new avenues to explore, it won't be worth its current price.

Once again, here are the numbers you need, both present and future:

Percent of Internet-Connected World on Facebook (end of 2011) | 37% |

Percent of World (less China) on Facebook (end of 2011) | 48% |

Profit per Monthly Active User in 2011 | $1.19 |

Most Recent Quarterly Revenue per User | $1.21 |

88% | |

Annualized Profit Growth in 2011 | 65% |

Annualized Monthly User Growth in 2011 | 40% |

Projected Users at 69% of Non-Chinese Online Populace (2016) | 2,090 million |

Projected Annual Profit With 2,090 Million Users (2016) | $2,490 million |

Sources: Graphs, tables, and links in this article.

If nothing else happens between now and the fulfillment of this theory except the continued growth of users, revenue, and profit (stock prices would stay unchanged), Facebook would have a P/E of 24.

Foolish final thoughts

It seems clear that two things have to happen between now and then to justify pre-IPO hype and a long-term place for growth in your portfolio. Facebook must monetize its users far more effectively than it has to date, and it must maintain a consistent five-year growth rate that may be all but impossible at this stage of its life. Failing that, there's always the chance for Zuckerberg to pull a Steve Jobs and surprise us all with the wonder toy of tomorrow.

Let's face it: Right now, even if China were on board, Facebook wouldn't look like much of a multibagger. I've had my doubts for a while, and nothing I've uncovered here has convinced me that Facebook is worth it. I'd rather stick with companies that are both transformative and tiny -- the sort below many investors' radars. Find out more about three great companies that can deliver far better returns as they change the world in our latest free report. Click here to get the free information you need for a great investment today.

At the time thisarticle was published Fool contributorAlex Planesholds no financial position in any company mentioned here. Add him onGoogle+or follow him on Twitter@TMFBigglesfor more news and insights. The Motley Fool owns shares of Facebook and Google.Motley Fool newsletter services have recommended buying shares of Google. The Motley Fool has a disclosure policy. We Fools may not all hold the same opinions, but we all believe thatconsidering a diverse range of insights makes us better investors. Try any of our Foolish newsletter services free for 30 days.

Copyright © 1995 - 2012 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.